Does Florida Home Insurance Cover HOA Storm Special Assessments? (2026)

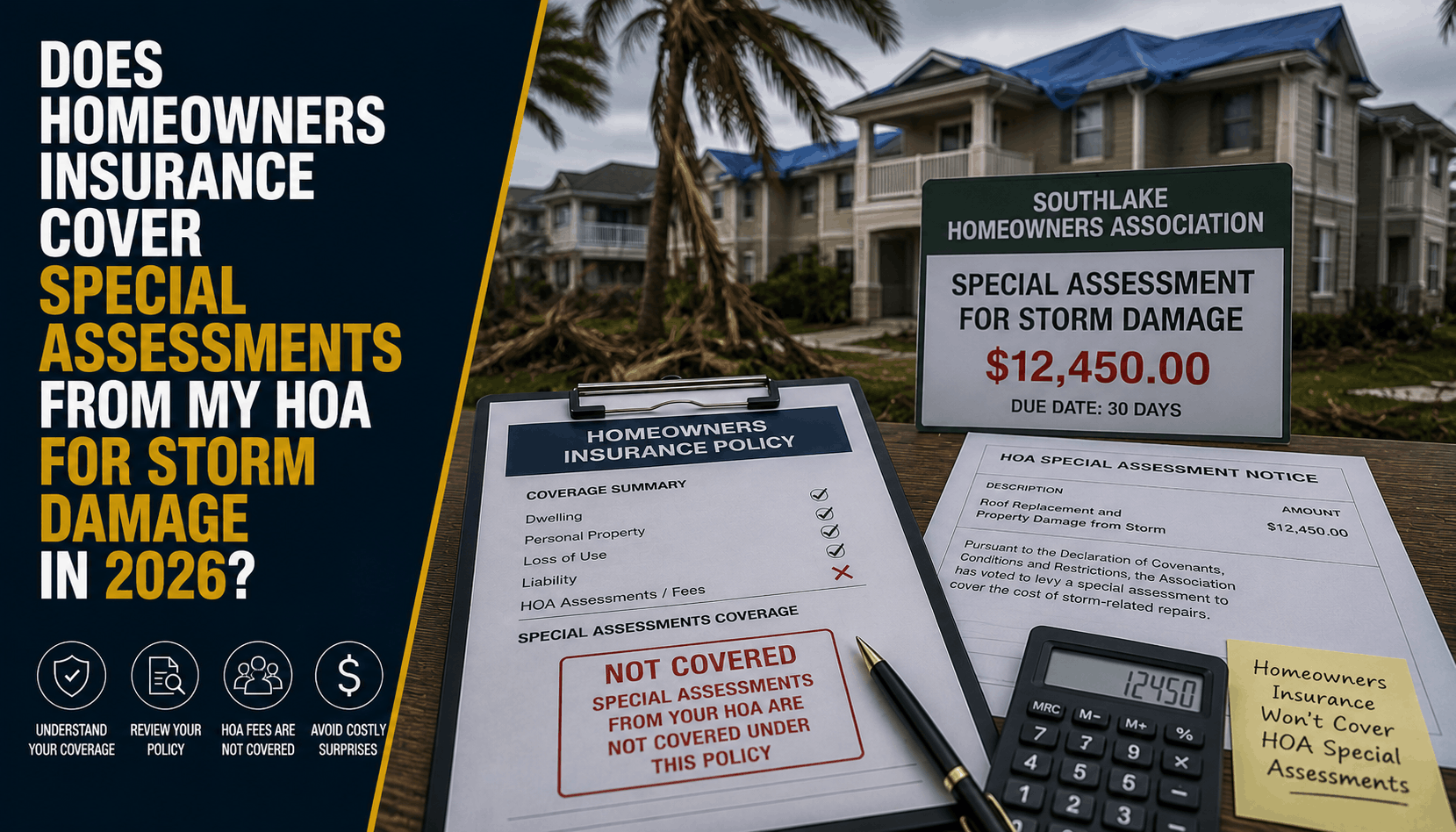

Does Homeowners Insurance Cover Special Assessments from My HOA for Storm Damage in 2026?

The Direct Answer

The short answer is yes, but only if you have a specific, frequently underinsured add-on called Loss Assessment Coverage. In 2026, if a severe hurricane, tornado, or lightning storm tears through your Stuart neighborhood and causes catastrophic damage to common HOA properties—like the clubhouse, community pool, or main condo roofs—the HOA board will issue a massive special assessment to split the remaining repair bills among all unit owners. A standard homeowners (HO-3) or condo (HO-6) insurance policy will not automatically step in to pay your share of that assessment. Unless you have explicitly updated your policy with a dedicated Loss Assessment Endorsement, your baseline insurer will deny the claim, leaving you legally obligated to pay thousands of dollars in emergency assessments entirely out of your own pocket.

For property owners across Stuart and the Treasure Coast, this coverage gap has become a major financial risk in 2026. As local HOA master deductibles climb to unprecedented heights and Florida's updated Structural Integrity Reserve Study (SIRS) mandates push associations to aggressively collect funding for structural elements, unexpected storm assessments are catching completely unprepared homeowners completely off guard.

1. The Anatomy of the Assessment: Why Your Baseline Policy Falls Short

When a severe storm damages a master community, the HOA's primary commercial insurance policy is designed to step in. However, standard master policies feature massive hurricane deductibles—often calculated as a flat 2% to 5% of the total property value. If a luxury condo complex or neighborhood clubhouse suffers a major wind loss, the master policy deductible can easily reach $250,000 to $1,000,000.

Because the HOA cannot pay this structural deductible out of regular reserve funds, they must divide that entire multi-million-dollar gap among the individual owners as a special assessment.

- The Baseline Trap: While Florida law requires residential condo policies issued after mid-2024 to carry a minimum of $5,000 in property loss assessment coverage, this limit is a mere drop in the bucket in 2026.

- The Exposure Shortfall: If your local association hits you with a $15,000 to $25,000 special assessment to replace a shared clubhouse roof after a summer storm, your built-in $5,000 minimum leaves you holding a devastating deficit.

- The Liens and Foreclosures: In Florida, if you fail to pay your share of an HOA special assessment, the association retains the full legal right to place a lien on your home and initiate foreclosure proceedings, regardless of whether your primary mortgage is paid in full.

2. Covered Perils vs. Capital Upgrades: Where Insurers Draw the Line

Your personal loss assessment coverage is highly valuable, but it is not a blank check for any bill your HOA board decides to send your way. To trigger insurance coverage, the special assessment must meet strict, legal underwriting parameters:

- When Insurance WILL Pay (The Covered Peril): Your loss assessment policy will pay your share of the bill if the structural damage was caused by an active peril explicitly listed in your personal policy—such as hurricane-force winds, hail, tornado strikes, or lightning. If a windstorm rips off the community pool pavilion, the assessment is covered up to your endorsement limit.

- When Insurance WILL NOT Pay (SIRS and Wear-and-Tear): Your insurer will immediately deny any assessment claims relating to standard wear and tear, aging buildings, or deferred maintenance. In 2026, under Florida's strict SIRS compliance guidelines, many communities are issuing assessments to fund structural reserves for load-bearing walls, fireproofing, or plumbing systems. These are classified as capital maintenance reserves, not sudden storm losses, and are completely excluded from insurance payouts.

- The Flood Exclusion: Standard home policies exclude flood and rising storm surge. If a hurricane pushes rising waters from the St. Lucie River into your community, damaging the first-floor common structures, your regular loss assessment coverage will pay $0 unless you also carry a personal flood insurance policy with a specialized flood loss assessment rider.

3. How to Protect Your Home and Erase the Assessment Loophole

You do not have to live in fear of a surprise assessment letter, but you must actively adjust your policy framework before the peak of the Florida hurricane season. At Walker Insurance Agency, we advise Stuart homeowners to secure their equity using three clear steps:

- Step 1: Request Your HOA's Master Insurance Declarations. Contact your HOA board or property manager to request a copy of the community’s master insurance summary page. Look specifically for the "Hurricane Deductible" percentage and calculate the potential assessment exposure per unit.

- Step 2: Bind an HO 04 35 Loss Assessment Endorsement. Contact your independent insurance broker to manually increase your Loss Assessment limit. Boosting your protection from the basic $5,000 minimum up to $20,000, $50,000, or $100,000 is incredibly inexpensive—often adding only $15 to $35 a year to your primary premium.

- Step 3: Audit Your Personal Deductible Alignment. Ensure your loss assessment coverage does not carry a separate, high deductible that eats away at your payout. Aligning your personal limits with your community's master deductible ensures your out-of-pocket costs remain flat and manageable.

Why Working with an Independent Agency is Vital

Attempting to evaluate complex condo master contracts and HOA property divisions through an automated direct-to-consumer website is a recipe for an expensive coverage gap. At Walker Insurance Agency, we provide the localized, expert advocacy required to secure your home.

The Walker Advantage:

- Master Policy Cross-Examination: We thoroughly review your HOA’s master insurance structures to calculate your exact personal assessment vulnerability windows.

- Targeted Endorsement Matching: We shop Florida's leading independent insurance market to integrate high-limit loss assessment riders without inflating your base rates.

- Treasure Coast Inflation Balancing: We scale your policy limits to match the actual reality of local Stuart construction costs, ensuring your hard-earned wealth remains completely insulated.

FAQ

1. Can I buy Loss Assessment Coverage after a storm is forecasted or after my HOA announces an upcoming special assessment?

No. Insurance carriers will place a temporary binding freeze on all policy changes and new endorsements the moment a tropical storm or hurricane watch is active in Florida. Furthermore, you cannot add coverage to pay for an assessment that is already planned, voted on, or announced by your HOA board. You must have the active endorsement on your policy before the storm event occurs.

2. If my HOA assesses me for damage to another unit owner's private property, will my insurance cover it?

Typically, no. Personal loss assessment coverage is designed to cover your shared liability for common elements owned collectively by the association (such as roofs, lobbies, siding, and community centers). It does not pay for assessments issued to repair private elements belonging solely to a neighboring individual unit owner.

3. Does loss assessment coverage pay my regular monthly HOA maintenance dues if they increase after a storm?

No. Loss Assessment coverage only applies to one-time, unexpected special assessments triggered by a sudden physical loss to shared property from a covered peril. It does not cover gradual, permanent increases to your regular monthly or quarterly HOA maintenance dues, even if those increases are designed to offset rising commercial insurance premiums for the association.

Insulate Your Homeowner Equity Before the Next Storm

Your home or condo is a vital personal investment, but assuming your standard policy automatically covers the massive financial gaps left by an HOA master policy is an administrative gamble that can instantly drain your bank account. True peace of mind requires looking closely at your underlying contract boundaries and ensuring your written coverage matches the physical reality of your neighborhood.

Take control of your home protection today. Contact Walker Insurance Agency for a comprehensive portfolio evaluation. We provide the visibility you need to eliminate hidden HOA assessment loopholes, deploy high-limit loss assessment riders, and protect your family's hard-earned wealth safely in Stuart.

[GET A FREE QUOTE TODAY]

Call our personal lines division at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your property boundaries today.

Related Articles

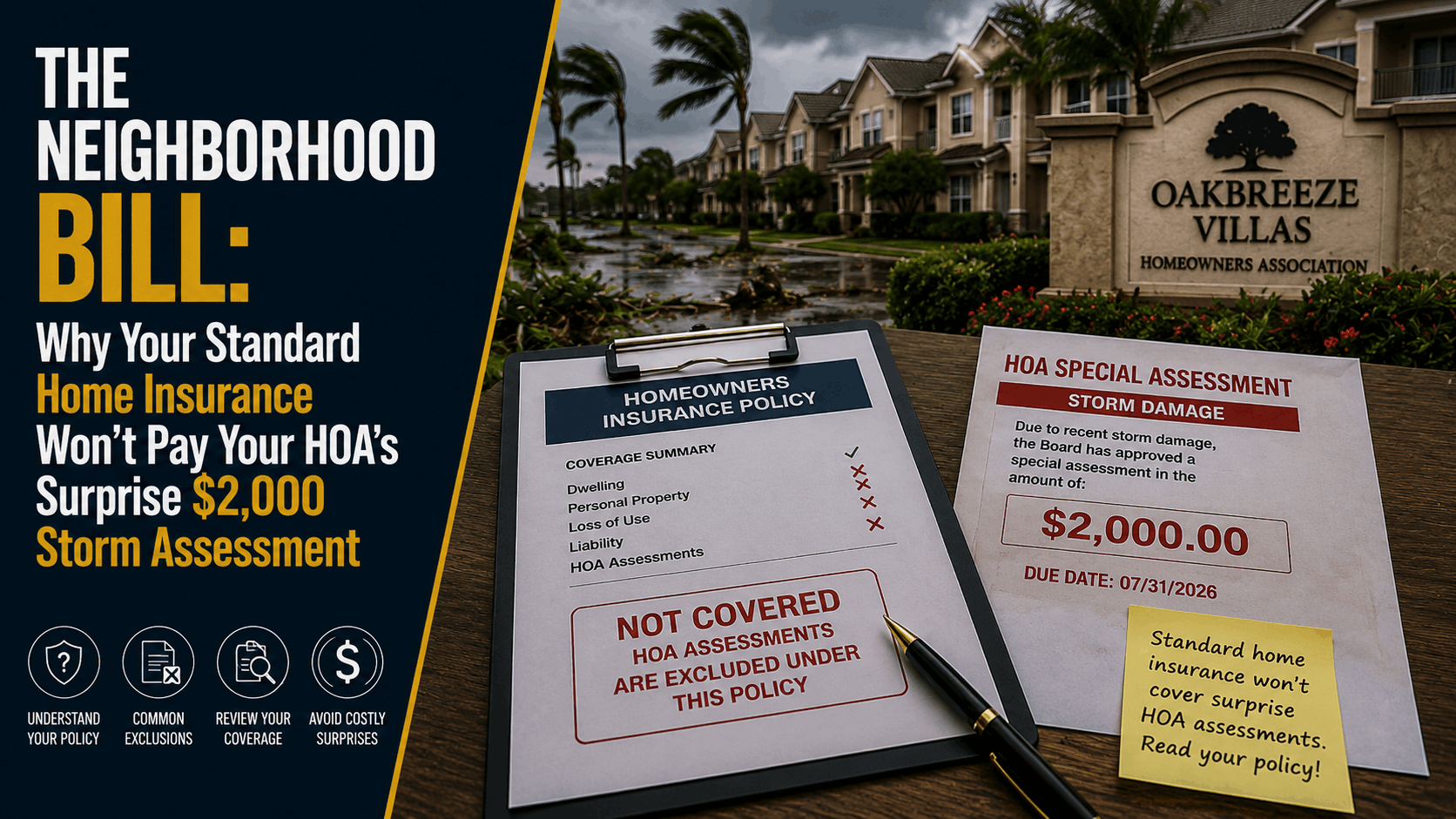

Why Home Insurance Won't Pay Your HOA Storm Assessment (2026)

Received a surprise HOA special assessment after a storm? Discover the critical loss assessment loopholes leaving Stuart homeowners completely exposed in 2026.

Read More →

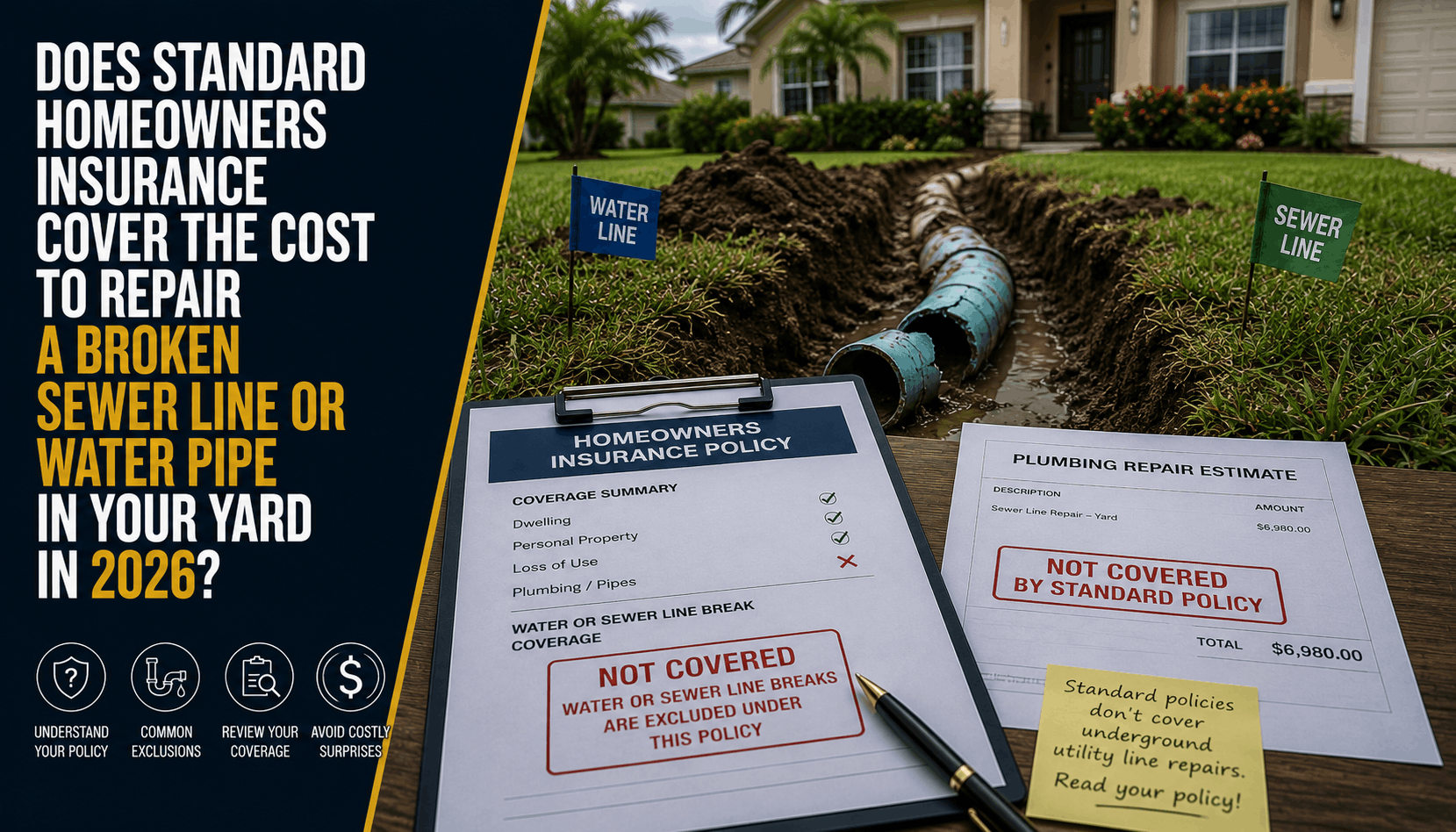

Does Home Insurance Cover Broken Pipes in the Yard? (2026)

Discover why standard homeowners insurance completely denies the cost to repair a broken sewer line or water main in your yard, and how Stuart homeowners can fix this gap.

Read More →

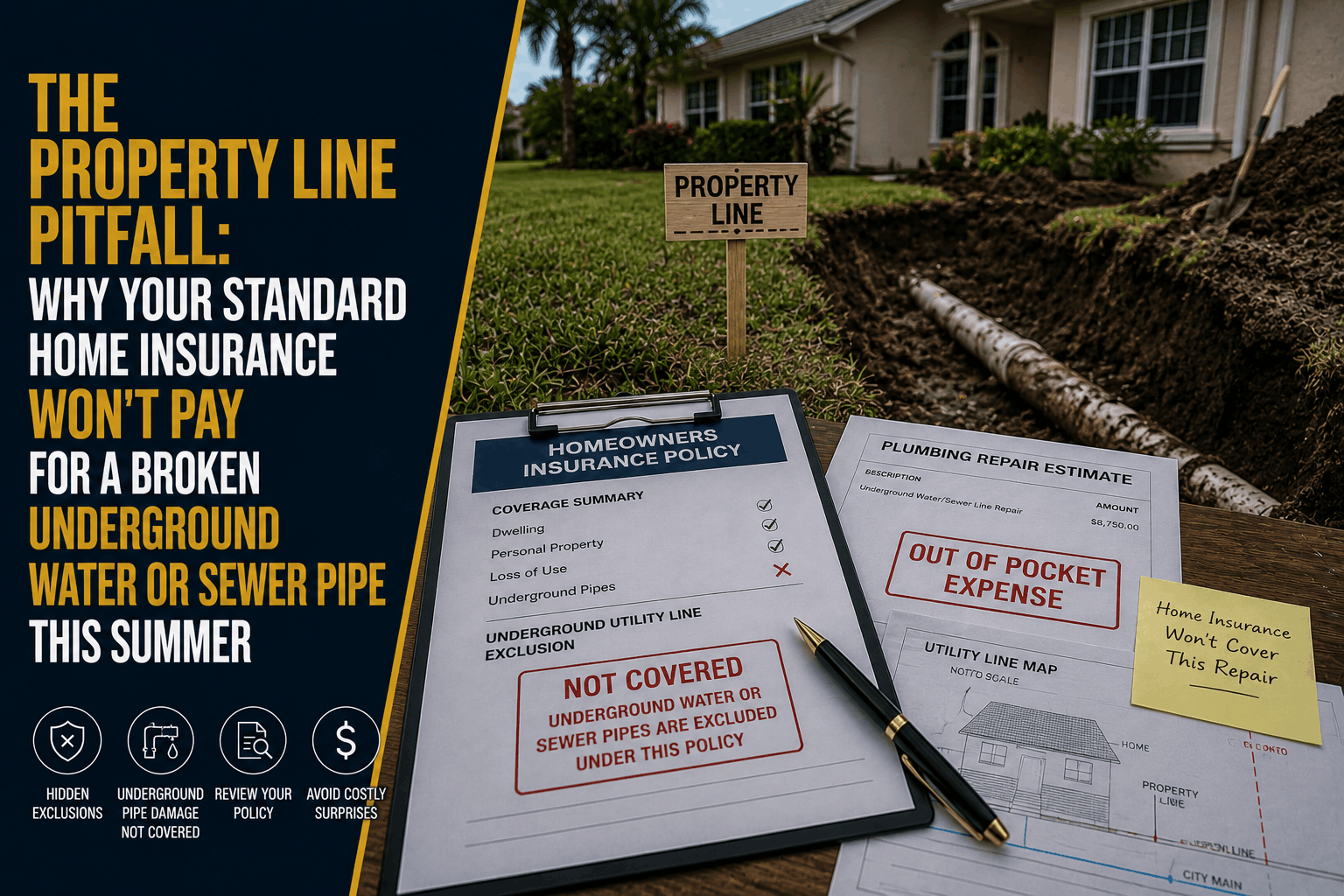

Does Home Insurance Cover Broken Underground Utility Lines? (2026)

Think your standard Florida homeowners insurance pays to fix a cracked water main or collapsed sewer line in your yard? Discover the property line pitfall leaving Stuart homes exposed.

Read More →