Insurance Gap for Uber & DoorDash Drivers in Florida (2026)

The Insurance Gap: What Every Uber and DoorDash Driver Must Know in Florida

The Quick Answer: The "Insurance Gap" is the period when a gig driver is logged into an app (like Uber or DoorDash) but has not yet accepted a trip or delivery. During this time, your personal auto insurance will deny any claim because you are using the vehicle for business, and the app’s commercial insurance provides only minimal liability coverage—leaving your own car with zero protection. To achieve total visibility and protection in 2026, Florida drivers must add a Rideshare Endorsement to their personal policy.

In 2026, Florida remains one of the most litigious states for gig work. Without the proper "hybrid" coverage, a single fender-bender while waiting for an order could result in a canceled policy, thousands in out-of-pocket repairs, and the suspension of your driving privileges.

Understanding the Three Periods of Gig Work

Insurance coverage in Florida shifts automatically based on your app status. Understanding these phases is vital for your financial safety:

- Period 1 (The Gap): App is ON, but no request is accepted. Your personal insurance is OFF, and app coverage is at its lowest (usually liability only). Your car is not covered for collision.

- Period 2: Request accepted, and you are en route to the passenger or restaurant. The app’s commercial policy (usually $1M liability) kicks in.

- Period 3: Passenger is in the car or food is being delivered. Full app coverage is active.

Why Your Personal Policy Won't Save You

A common mistake among Florida drivers is assuming their standard "Full Coverage" policy protects them while working.

The Reality in 2026:

Standard personal auto policies in Florida have a strict "Business Use Exclusion." If you are in an accident and the adjuster finds out you were "online" with DoorDash or Uber, they will deny the claim for breach of contract. In many cases, the insurer will also non-renew or cancel your policy entirely for failing to disclose your commercial activity.

Florida Requirements for Rideshare & Delivery (2026)

Florida Statute 627.748 sets the specific insurance requirements for Transportation Network Companies (TNCs):

- While Logged In (Period 1): You must have at least $50,000 for bodily injury per person, $100,000 per accident, and $25,000 for property damage.

- While Engaged (Periods 2 & 3): A minimum of $1 million in primary third-party liability coverage is required.

The Catch: While Uber and DoorDash provide the liability to meet these laws, they rarely provide Collision or Comprehensive coverage during Period 1. If you hit a pole while waiting for a Dash, you are on your own.

The Solution: Rideshare Endorsements vs. Hybrid Policies

To close the gap, you don't necessarily need a full (and expensive) commercial policy.

- Rideshare Endorsement: An add-on to your personal policy that specifically "buys back" coverage for Period 1. In 2026, this typically adds $15 to $30 per month to your premium.

- Hybrid Policy: A single policy designed for people who use one vehicle for both personal and business use 50/50.

- Full Commercial: Necessary if you have a dedicated vehicle used only for deliveries or rideshare.

2026 Costs: What Will You Pay in Florida?

Insurance rates for gig workers in Florida have seen a slight stabilization in 2026, but remain higher than the national average.

| Provider | Estimated Monthly Add-on | Best For |

|---|---|---|

| State Farm | +15-20% of premium | Widest availability in FL |

| Progressive | Varies | Drivers who also do food delivery |

| Mercury | As low as $0.90/day | Part-time Period 1 specialists |

| USAA | $6 - $15 | Military members and families |

Why Working with an Independent Agency is the Best Move

At Walker Insurance Agency, we provide the visibility needed to ensure you aren't paying for "double coverage" while eliminating the dangerous gaps in your protection.

The Walker Advantage:

- Carrier Matching: We shop multiple 2026 Florida carriers to find those that are "gig-worker friendly" and offer the lowest endorsement rates.

- Claim Protection: We ensure your personal insurer knows about your side hustle properly, so your claims are never denied for "misrepresentation."

- Local Stuart Expertise: We understand the high-traffic risks of the Treasure Coast and how to protect your income and your vehicle.

FAQ

1. Does DoorDash insurance cover my car if I get into an accident?

Only if you have an active delivery in the car (Period 3) and even then, they only provide "excess" liability. They almost never cover your own vehicle's repairs unless you have a specific commercial add-on.

2. Can I just not tell my insurance company I drive for Uber?

That is insurance fraud and a recipe for disaster. If you have an accident, adjusters will check app logs. A denial will leave you with a totaled car and a potential 3-year license suspension in Florida.

3. Is rideshare insurance the same as delivery insurance?

Technically no, but in 2026, most major Florida insurers bundle them into a single "Gig Economy" or "Rideshare" endorsement that covers both passengers and food delivery.

4. How much does a rideshare endorsement cost in Florida?

For most safe drivers in Florida, adding a rideshare endorsement costs between $180 and $350 per year—a small price to pay to avoid a $20,000 uncovered loss.

Local Business Schema

Don’t Let Your Side Hustle Become a Liability

Driving for the gig economy is a great way to earn extra income, but it shouldn't put your primary vehicle at risk. In Florida, the "Insurance Gap" is real, and it is expensive.

Close the gap today. Contact Walker Insurance Agency for a complimentary gig-worker policy review. We provide the visibility you need to ensure your app work is fully protected without breaking the bank.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us help you protect your car and your hustle.

Related Articles

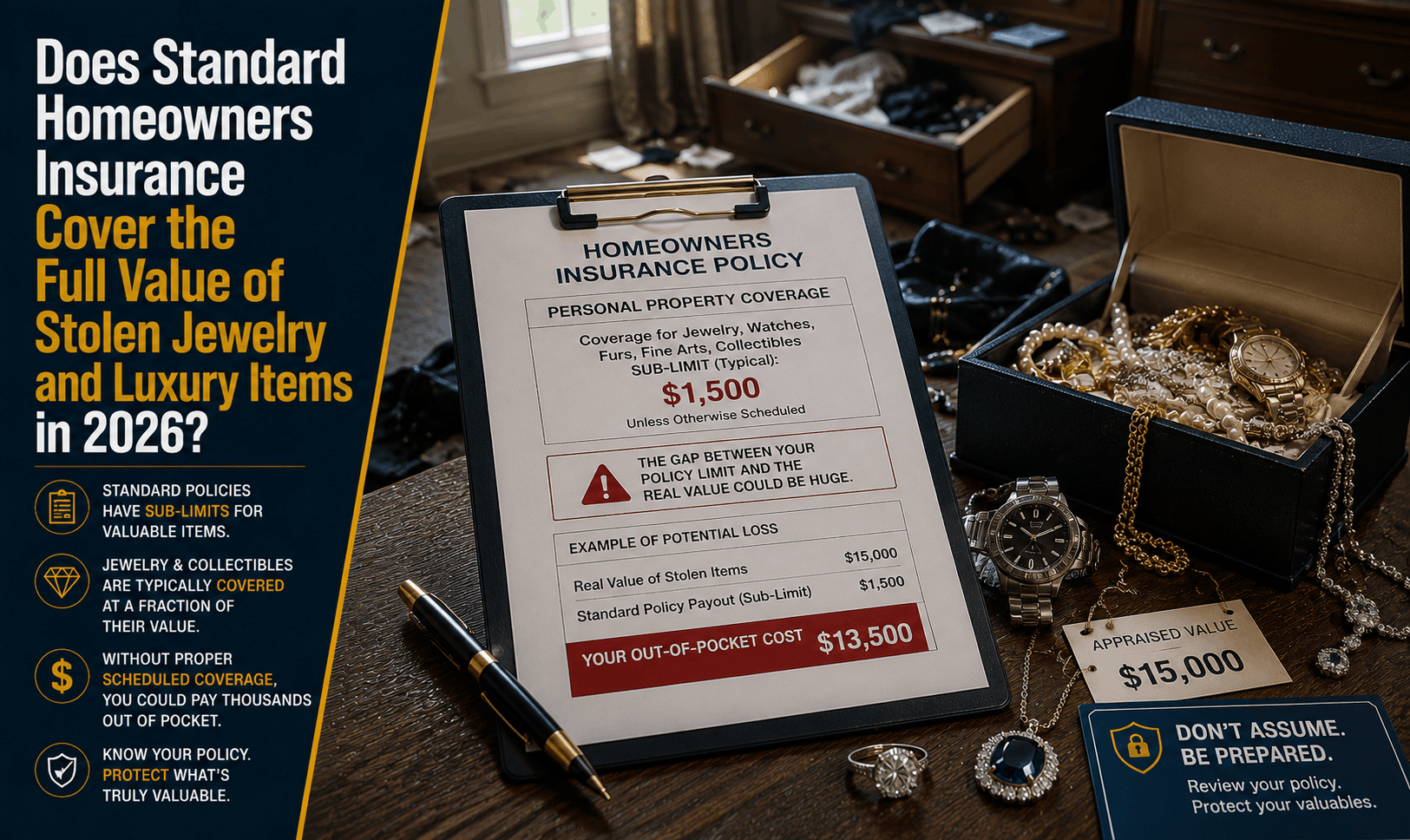

Does Homeowners Insurance Cover Stolen Jewelry & Luxury Goods? (2026)

Had luxury watches or jewelry stolen? Learn why standard homeowners insurance caps theft payouts at $1,500 and how to fully insure your high-value items.

Read More →

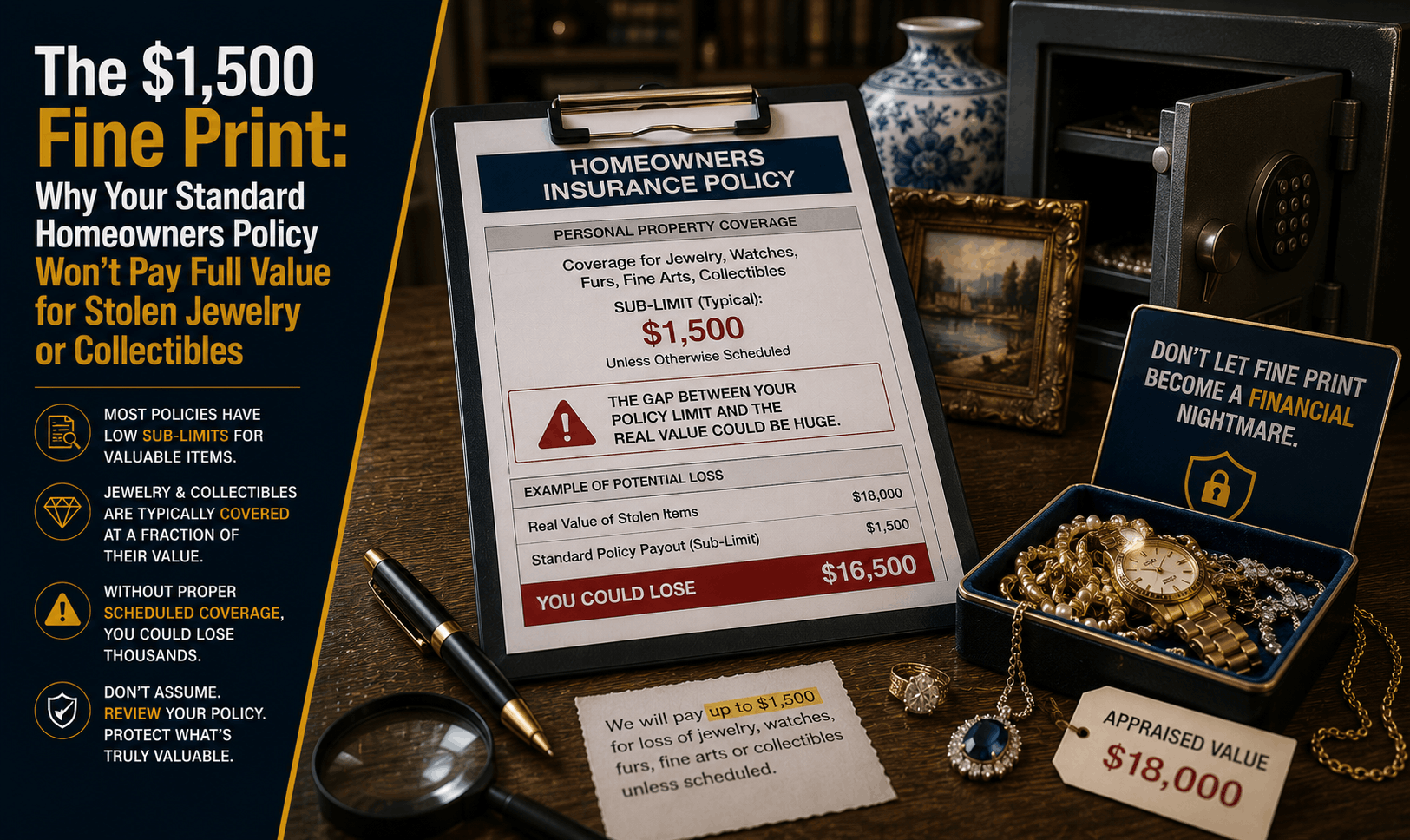

Does Home Insurance Cover Stolen Jewelry & Collectibles? (2026)

Had jewelry or valuables stolen? Discover why standard homeowners insurance limits theft payouts to $1,500 and how to fully insure your high-value items.

Read More →

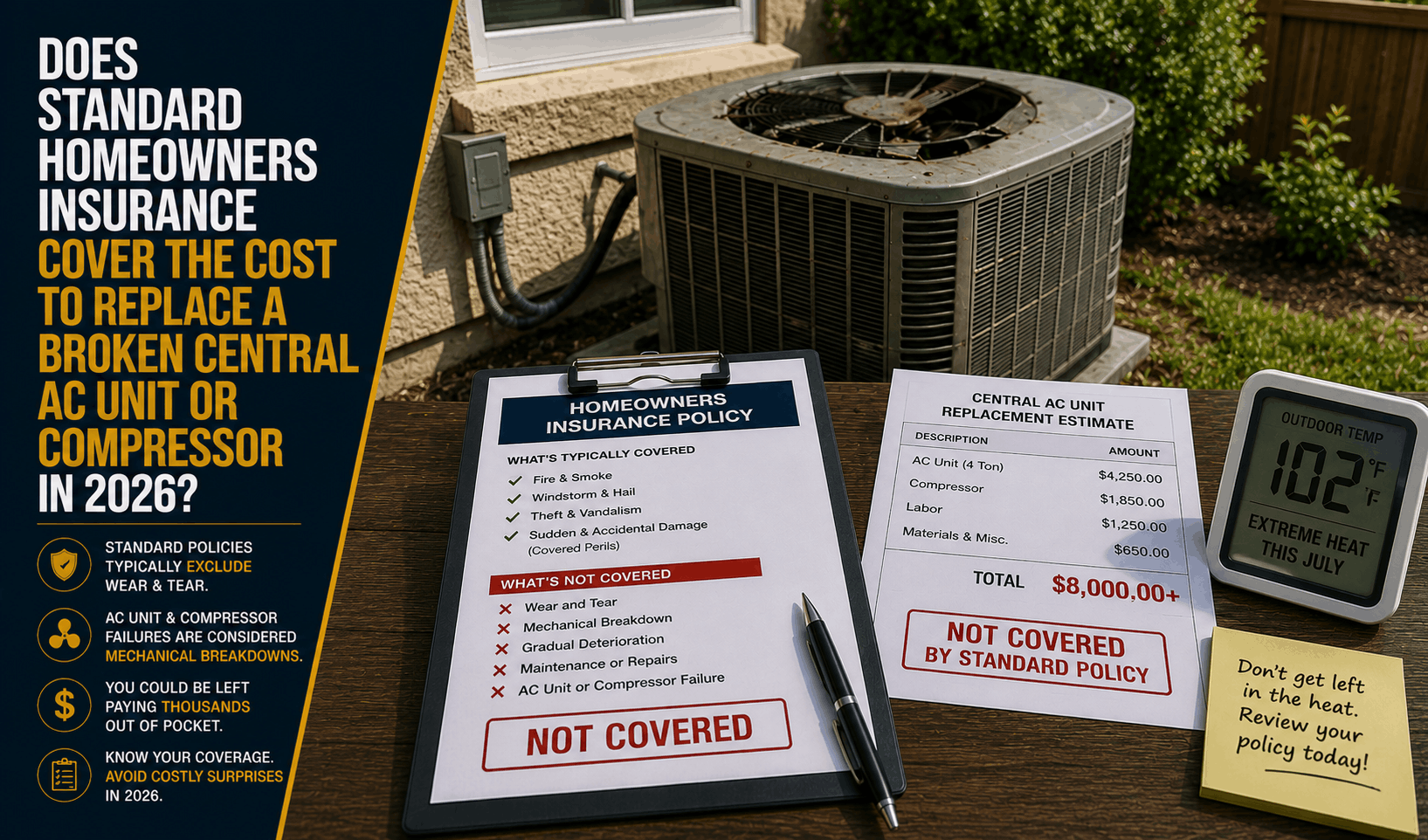

Does Homeowners Insurance Cover Broken AC Units? (2026)

AC broken in the summer heat? Learn why standard homeowners insurance won't pay to replace a broken central AC unit or compressor due to mechanical wear.

Read More →