Is a Business Liable If an Employee Crashes a Personal Car for Work?

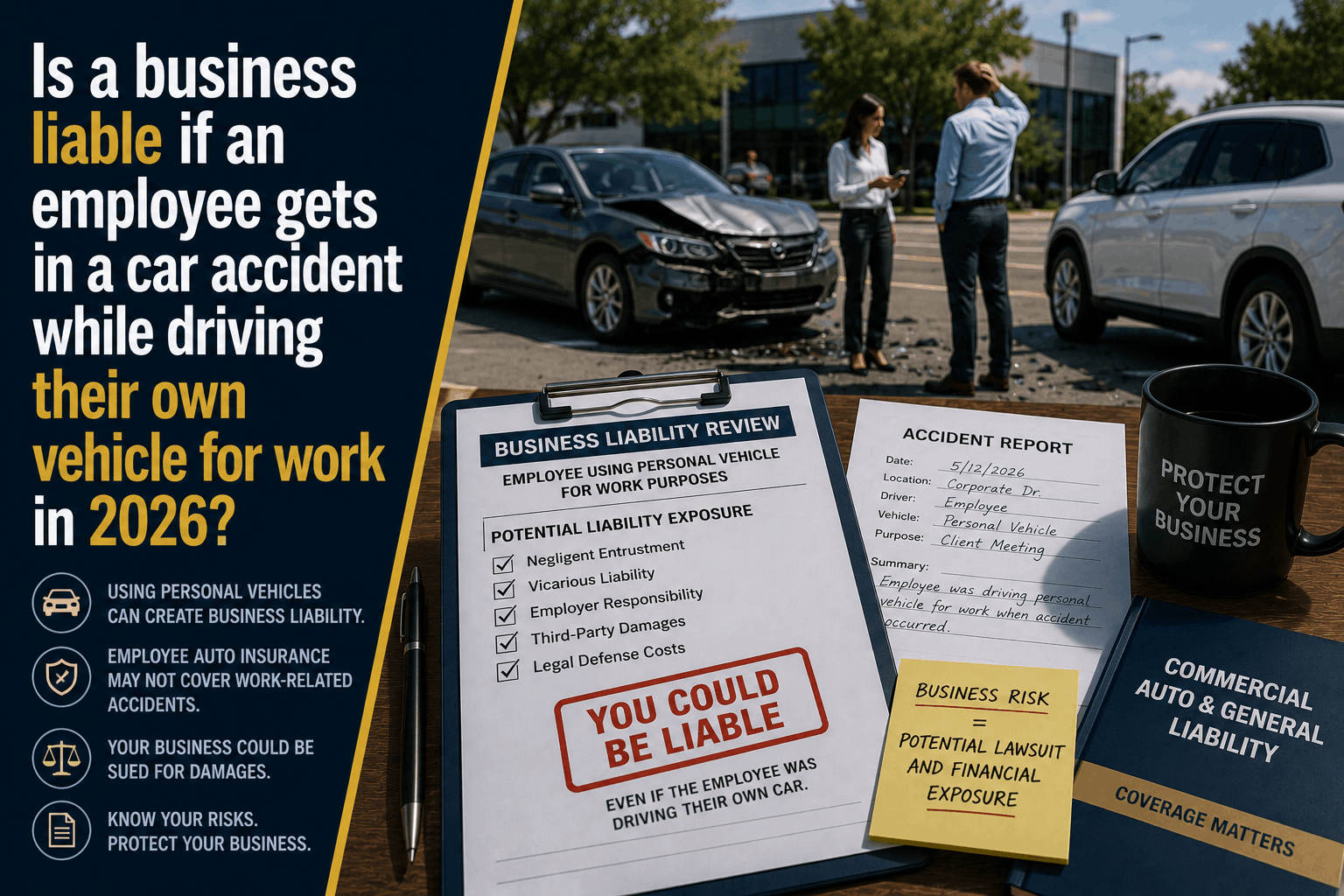

Is a Business Liable If an Employee Gets in a Car Accident While Driving Their Own Vehicle for Work in 2026?

The Direct Answer: Yes, a business is 100% legally liable if an employee causes a car accident while driving their personal vehicle for work-related purposes. Under the long-standing legal doctrine of respondeat superior (vicarious liability), an employer is held financially responsible for the negligent actions of their staff if those actions occur within the course and scope of their employment.

In 2026, this liability is catching thousands of small and mid-sized business owners completely off guard. There is a dangerous, widespread myth that because the vehicle belongs to the employee, the employee's private auto insurance will absorb the entire loss.

To achieve total visibility over your corporate balance sheet, you must realize that standard personal auto policies explicitly exclude commercial use. If a worker causes a crash while executing a business errand, the injured third party will bypass the employee's low personal limits and sue your business directly. Without a specialized add-on insurance line known as Hired and Non-Owned Auto (HNOA) coverage, your standard business general liability policy will pay exactly $0 toward your defense.

1. The Real-World Triggers of Employer Auto Liability

Many business owners believe they only face auto liability if they manage a dedicated fleet of commercial delivery vans. However, in the modern corporate landscape, everyday office routines trigger severe vicarious liability exposures.

Your business is legally on the hook if an employee causes a collision during any of the following activities:

- Routine Office Errands: Sending an administrative assistant to drop off mail at the post office, pick up office supplies, or grab lunch/coffee for a client meeting.

- Off-Site Business Travel: A sales representative driving their personal sedan to visit a prospect, or a manager traveling between multiple company office locations.

- Banking and Administrative Tasks: Directing a worker to take cash or checks to the local bank to make a corporate deposit.

The "Coming and Going" Rule: Generally, your business is not liable for accidents that occur during an employee's standard daily commute from home to their fixed workplace. Commuting is legally defined as a personal activity. However, the exact second you instruct that employee to stop by a client's office on their way to work, the entire commute converts into a business errand, instantly shifting the legal liability onto your corporate entity.

2. The 2026 Financial Reality: The Severity of the Threat

Operating an enterprise with a payroll roster without verifying your commercial auto endorsements exposes your corporate capital to immense modern litigation inflation. If an employee triggers a corporate auto lawsuit this year, the out-of-pocket costs build rapidly across multiple fronts:

- The Uninsured Litigation Defense Burn Rate: Managing an injury lawsuit through a private corporate defense counsel costs between $250 and $500 per hour. Filing responsive pleadings, managing digital data discovery, and attending depositions averages $20,000 to $45,000 before the case ever reaches a trial date.

- Third-Party Bodily Injury Settlements: Modern medical inflation has driven basic emergency room bills, structural evaluations, and surgical rehabilitation costs higher than ever. A moderate collision involving soft-tissue or structural injuries routinely results in corporate settlements crossing $50,000 to $150,000.

3. How to Erect a Secure Non-Owned Auto Shield

If your enterprise frequently utilizes workers to execute minor errands or travel between client offices using their personal vehicles, your corporate balance sheet is completely vulnerable.

To safely insulate your business, you must transition your protection framework to a precise, dual-layer risk management layout:

Step 1: Implement an Active Employee Driving Record (MVR) Pre-Screening Protocol

Step 2: Formally Bind a Hired & Non-Owned Auto (HNOA) Endorsement Policy Rider

===================================================================================

= 100% Comprehensive Corporate Liability Safety for All Non-Owned Vehicle Errands

- The Contractual Shield: Contact your independent insurance agent and ask to formally add a Hired and Non-Owned Auto (HNOA) Endorsement to your Business Owner’s Policy (BOP) or General Liability framework. For a remarkably low annual premium addition—typically ranging between $100 and $300 per year—this rider deletes the non-owned vehicle loophole. It forces the carrier to step in, provide corporate defense attorneys, and fund third-party liability settlements if an employee crashes while driving a rented or personal vehicle on company business.

- The Operational Shield: HNOA coverage only handles liability for your business. It does not pay to fix the employee's personal vehicle. To protect your risk profile, your operational handbook must mandate that any worker driving for company errands must maintain valid personal auto limits of at least $100,000/$300,000. Management must collect and review copies of these insurance declaration pages annually.

Why Working with an Independent Agency is Vital

Attempting to manage complex commercial auto liabilities through a generic, automated online application ensures you will miss the critical regional riders needed to survive a vicarious liability claim. At Walker Insurance Agency, we provide the data-driven visibility you need to defend your business assets.

The Walker Advantage:

- Exposure Scope Audits: We analyze your industry operations—whether you handle basic office errands, restaurant deliveries, or sales travel—to scale your HNOA liability thresholds to match actual 2026 litigation trends.

- Umbrella Extension Management: We audit your commercial umbrella layers to guarantee that your non-owned auto liability protections extend cleanly into higher excess coverage limits.

- Strategic Carrier Matching: We cross-reference your business profile against the underwriting models of leading commercial insurers to capture the highest liability limits at the lowest available premium floors in Stuart.

FAQ

1. Does a Hired and Non-Owned Auto rider pay to fix the employee's personal car after an accident? No. An HNOA policy provides liability protection strictly for your business entity when a third party sues your company for damages. It features $0 for physical damage (comprehensive and collision) to the employee's personal vehicle. The employee must look to their own personal auto insurance policy's collision coverage to repair or replace their car.

2. Can an employee's personal insurance company sue my business after an accident? Yes. This process is known as subrogation. If an employee's personal insurance company pays out a claim for an accident that occurred while the worker was operating within the scope of employment, that carrier has the legal right to pursue your business to recover the funds they paid out, alleging that the commercial operation was the true entity responsible for the risk.

3. What should management do immediately if an employee calls to report a crash during a business errand? Instruct the employee to call emergency services and cooperate fully with local law enforcement to secure a formal police report. Advise them to take clear, high-resolution photographs of the scene, vehicle positions, and property damage. Gather the contact information of all involved parties and immediately notify your independent commercial agent. Do not let any manager admit company liability or promise out-of-pocket payments to the other driver at the scene.

Insulate Your Commercial Capital Before the Next Corporate Errand

Sending a worker out for a quick office supply pick-up or a routine coffee run is a standard piece of corporate life, but leaving that routine task exposed to a baseline general liability exclusion is a high-risk gamble that can instantly compromise your company’s financial survival.

Expose your true policy protections today. Contact Walker Insurance Agency for a comprehensive commercial policy evaluation. We provide the visibility you need to erase hidden non-owned auto loops, deploy high-limit HNOA riders, and protect your company's hard-earned wealth safely in Stuart.

[GET A FREE COMMERCIAL QUOTE TODAY]

Call our commercial lines division at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your corporate boundaries today.

Related Articles

Does Florida Full Coverage Pay Medical Bills in a Hit-and-Run?

Relying on Florida "full coverage" auto insurance to pay your medical bills after a hit-and-run in 2026? Discover why it fails and leaves you broke.

Read More →

Why Florida Full Coverage Auto Insurance Fails in Hit-and-Runs

Think you're safe with Florida "full coverage" auto insurance? Discover the hidden blind spot that leaves hit-and-run victims broke and unprotected in 2026.

Read More →

The Coffee Run Catastrophe: Hired & Non-Owned Auto Policy Gaps

If an employee crashes their personal vehicle while running a business errand, your standard insurance pays $0. Discover the Hired & Non-Owned Auto loophole.

Read More →