Roof Damage Insurance Claims in Florida: What Stuart Homeowners Must

Roof Damage Insurance Claims in Florida: What Stuart Homeowners Must Know!

![https://donan-twill.imgix.net/3a140a63-1656-455a-a6c0-819250ffa08e/MissingShingles.PNG?auto=compress%2Cformat&fit=min&fm=jpg&q=80&rect=0%2C0%2C600%2C452&s=28b7e844d3a8ccbb09c7312357826f70&w=1200][image2]

![https://cmsplatform.blob.core.windows.net/wwwromanroofingcom/blog-images/1ca288ea-ed63-4f92-834c-575e8c4f8ed8.jpg][image3]

![https://donan-twill.imgix.net/3a140a63-1656-455a-a6c0-819250ffa08e/MissingShingles.PNG?auto=compress%2Cformat&fit=min&fm=jpg&q=80&rect=0%2C0%2C600%2C452&s=28b7e844d3a8ccbb09c7312357826f70&w=1200][image2](https://donan-twill.imgix.net/3a140a63-1656-455a-a6c0-819250ffa08e/MissingShingles.PNG?auto=compress%2Cformat&fit=min&fm=jpg&q=80&rect=0%2C0%2C600%2C452&s=28b7e844d3a8ccbb09c7312357826f70&w=1200%5D%5Bimage2){kind=link}

![https://cmsplatform.blob.core.windows.net/wwwromanroofingcom/blog-images/1ca288ea-ed63-4f92-834c-575e8c4f8ed8.jpg][image3](https://cmsplatform.blob.core.windows.net/wwwromanroofingcom/blog-images/1ca288ea-ed63-4f92-834c-575e8c4f8ed8.jpg%5D%5Bimage3){kind=link}

In Florida, roof claims are among the most common — and expensive — insurance claims filed after hurricanes.

If you live in Stuart or anywhere in Martin County, your roof is your home’s first line of defense against wind, rain, and storm debris.

Understanding how hurricane roof damage works — and how insurance responds — can save you thousands of dollars and major stress.

How Hurricanes Damage Roofs

Strong winds during a hurricane can:

- Lift shingles

- Crack tiles

- Break waterproof seals

- Tear off flashing

- Allow water intrusion beneath underlayment

And here’s the critical part:

Sometimes roof damage isn’t immediately visible.

A storm passes. The roof “looks fine.”

Weeks later, stains appear on the ceiling.

By then, identifying the original cause can be more complicated.

That’s why early inspection after a major storm is essential in Stuart and coastal Florida communities.

Understanding Florida’s Hurricane Deductible

Florida homeowners insurance policies typically include a separate hurricane deductible.

Unlike standard deductibles (often a flat dollar amount), hurricane deductibles are usually calculated as:

2%–5% of your home’s insured value.

Example:

If your home is insured for $400,000 and you have a 2% deductible:

- You pay $8,000 out-of-pocket before coverage applies.

At 5%:

- You could owe $20,000 before insurance contributes.

Many homeowners only discover this when filing a roof claim Florida policyholders didn’t fully review beforehand.

Knowing your wind deductible Florida percentage is critical before hurricane season begins.

Roof Age and Insurance in Florida

Insurance carriers in Florida closely evaluate roof age — especially in hurricane-prone regions like Martin County.

Older roofs may:

- Require inspections

- Be insured at Actual Cash Value (ACV) instead of Replacement Cost

- Be excluded from full wind coverage

- Trigger non-renewal notices

If your roof is approaching 10–15 years (depending on material), underwriting scrutiny increases.

Annual inspections and maintenance documentation can make a significant difference in maintaining coverage eligibility.

Preventative Steps Before Hurricane Season

Preparation reduces claim disputes — and can protect both your home and your premium.

Before hurricane season in Stuart, consider:

- Scheduling a professional roof inspection

- Securing or replacing loose shingles or tiles

- Cleaning gutters and drainage systems

- Trimming nearby trees and overhanging branches

- Photographing and documenting your roof’s condition

If a claim is necessary later, having “before” photos strengthens your position.

Hurricane roof damage Stuart homeowners experience often leads to complex claim reviews — preparation gives you leverage.

Why Roof Claims Are So Common in Florida

Florida’s combination of:

- High winds

- Heavy rainfall

- Wind-driven debris

- Salt air corrosion

Creates ongoing stress on roofing systems.

That’s why Martin County roof insurance underwriting has become stricter in recent years.

Carriers know roof exposure is one of the largest financial risks in hurricane insurance Florida policies.

Final Thought: Your Roof Is Your Financial Shield

When hurricanes approach the Treasure Coast, your roof absorbs the first impact.

Understanding:

- Your deductible

- Your coverage type (ACV vs Replacement Cost)

- Your roof’s age and condition

- Your documentation

Can be the difference between a smooth claim and a financial shock.

Preparation today prevents surprises tomorrow.

FAQ – Roof Claims & Hurricane Insurance in Florida

Q1: Is roof damage from hurricanes covered in Florida?

Generally yes, but coverage depends on your policy terms, roof age, and whether the damage is caused by a named storm.

Q2: What is a wind deductible in Florida?

It is typically a percentage (2%–5%) of your insured dwelling value and applies to hurricane-related claims.

Q3: Can an old roof affect my insurance claim?

Yes. Older roofs may be covered at Actual Cash Value or face coverage limitations.

Q4: Should I inspect my roof before hurricane season?

Absolutely. Preventative inspections help identify vulnerabilities and reduce disputes during claims.

Related Articles

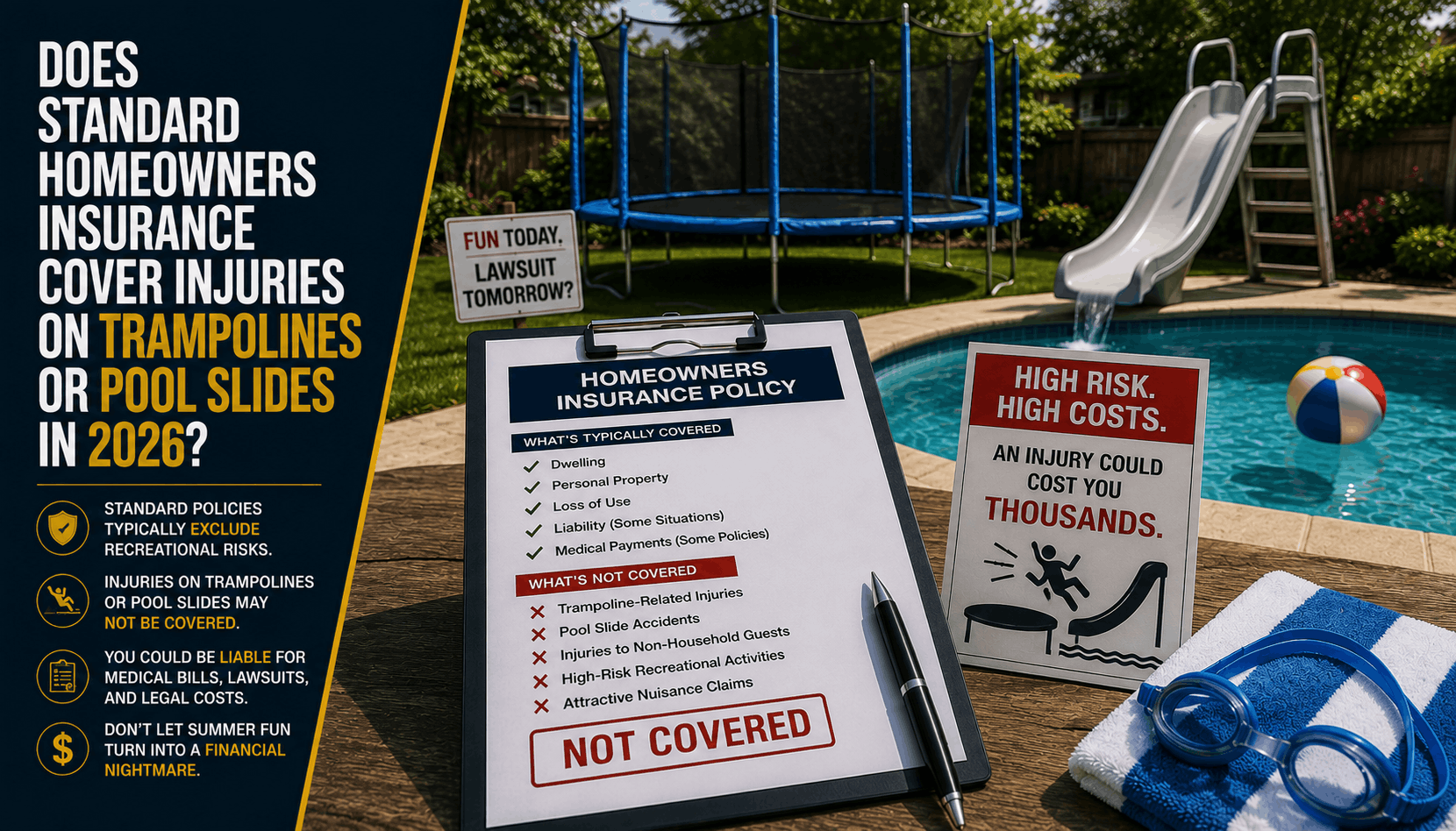

Does Homeowners Insurance Cover Trampolines or Pool Slides? (2026)

Planning summer fun in Stuart, FL? Discover why trampolines and pool slides are major homeowners insurance liability traps that can lead to dropped coverage.

Read More →

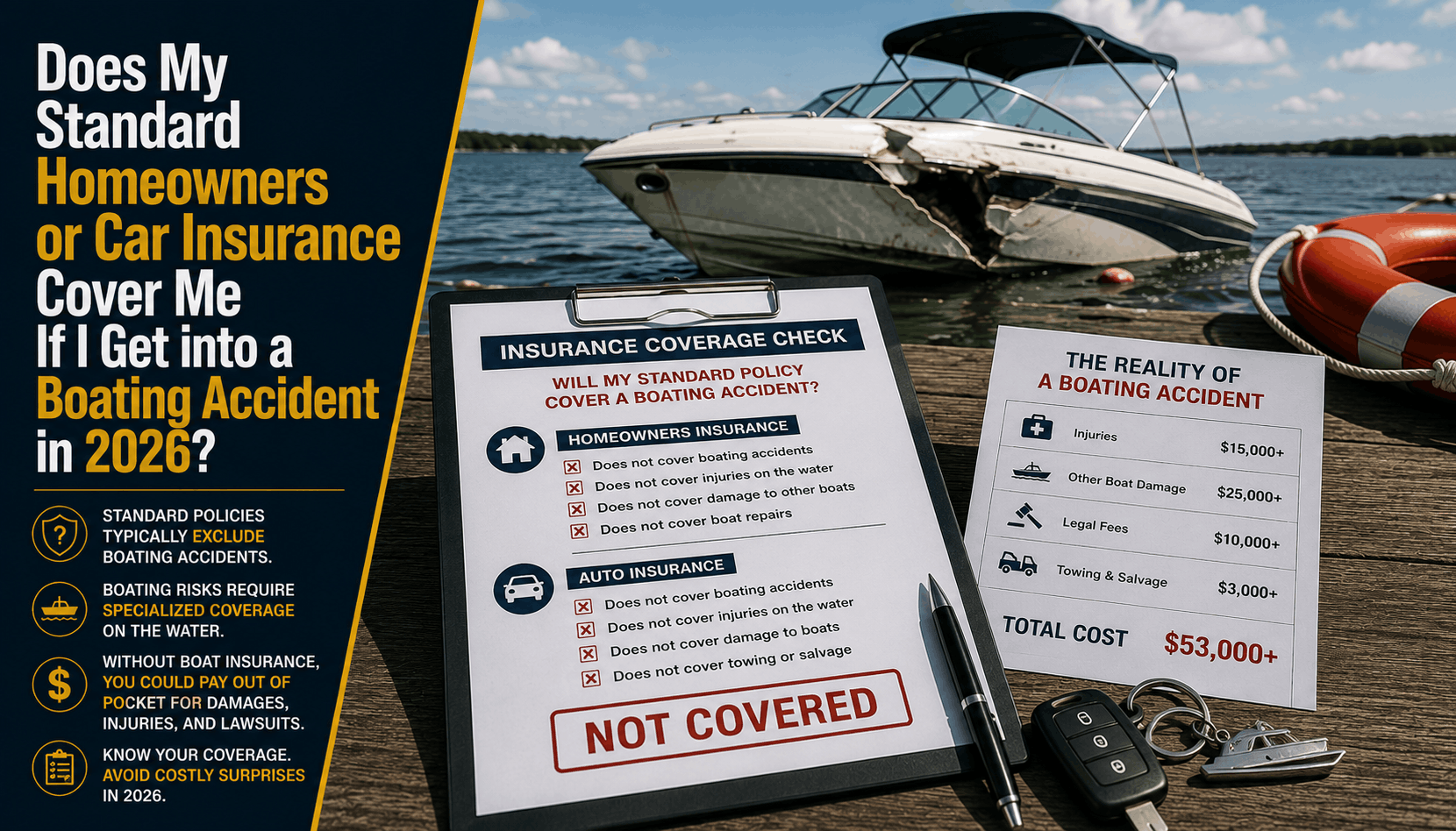

Does Home or Auto Insurance Cover Boating Accidents? (2026)

Planning a boat day in Stuart? Learn why relying on your home or auto insurance policies for watercraft liability is a dangerous financial gap.

Read More →

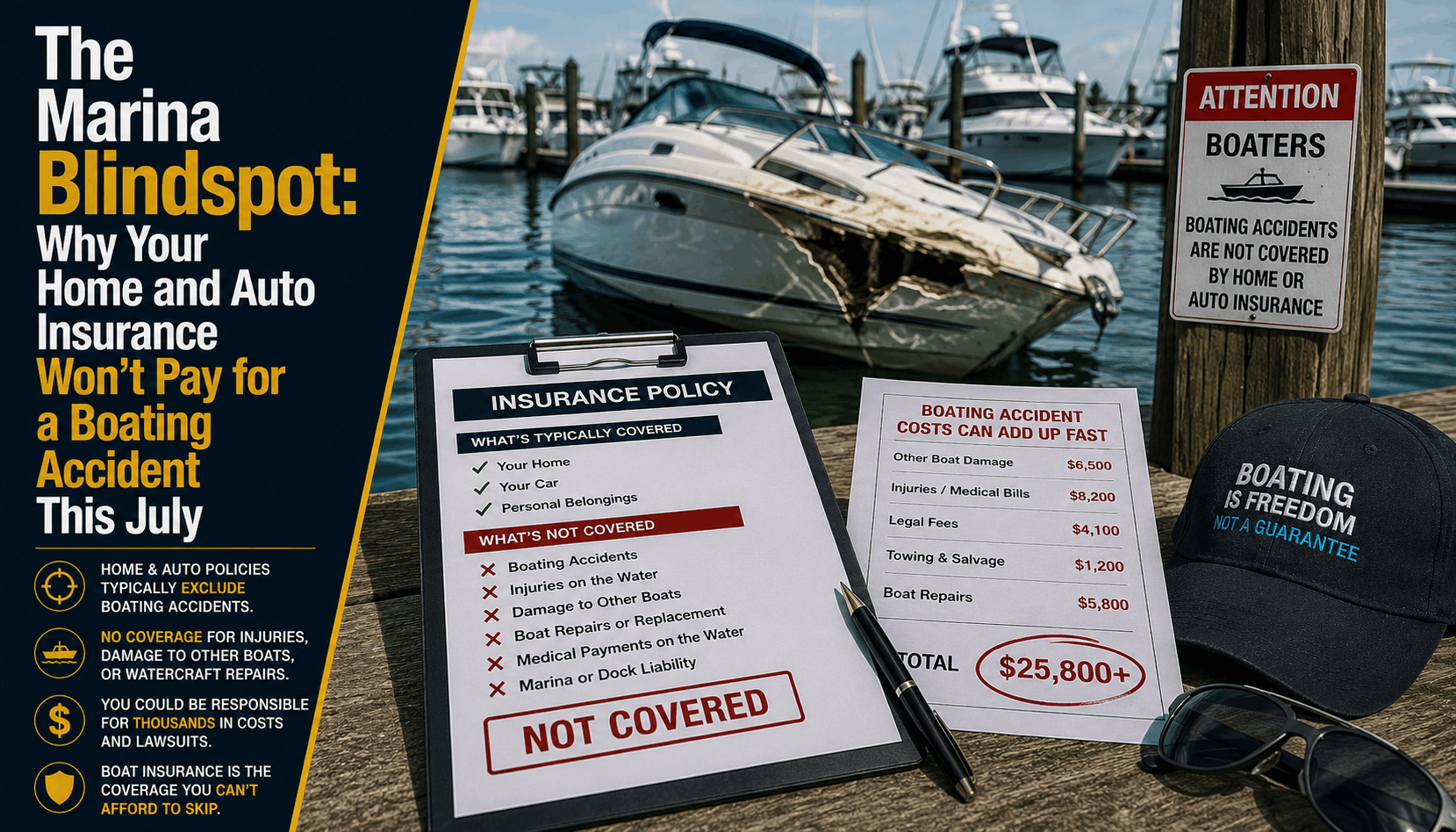

Why Home and Auto Insurance Won't Cover Boat Accidents (2026)

Planning a July boat day in Stuart, FL? Discover why relying on your home or auto insurance policies for watercraft liability is a dangerous financial blindspot.

Read More →