The Florida Sinkhole Loophole: Why Home Insurance Fails in July 2026

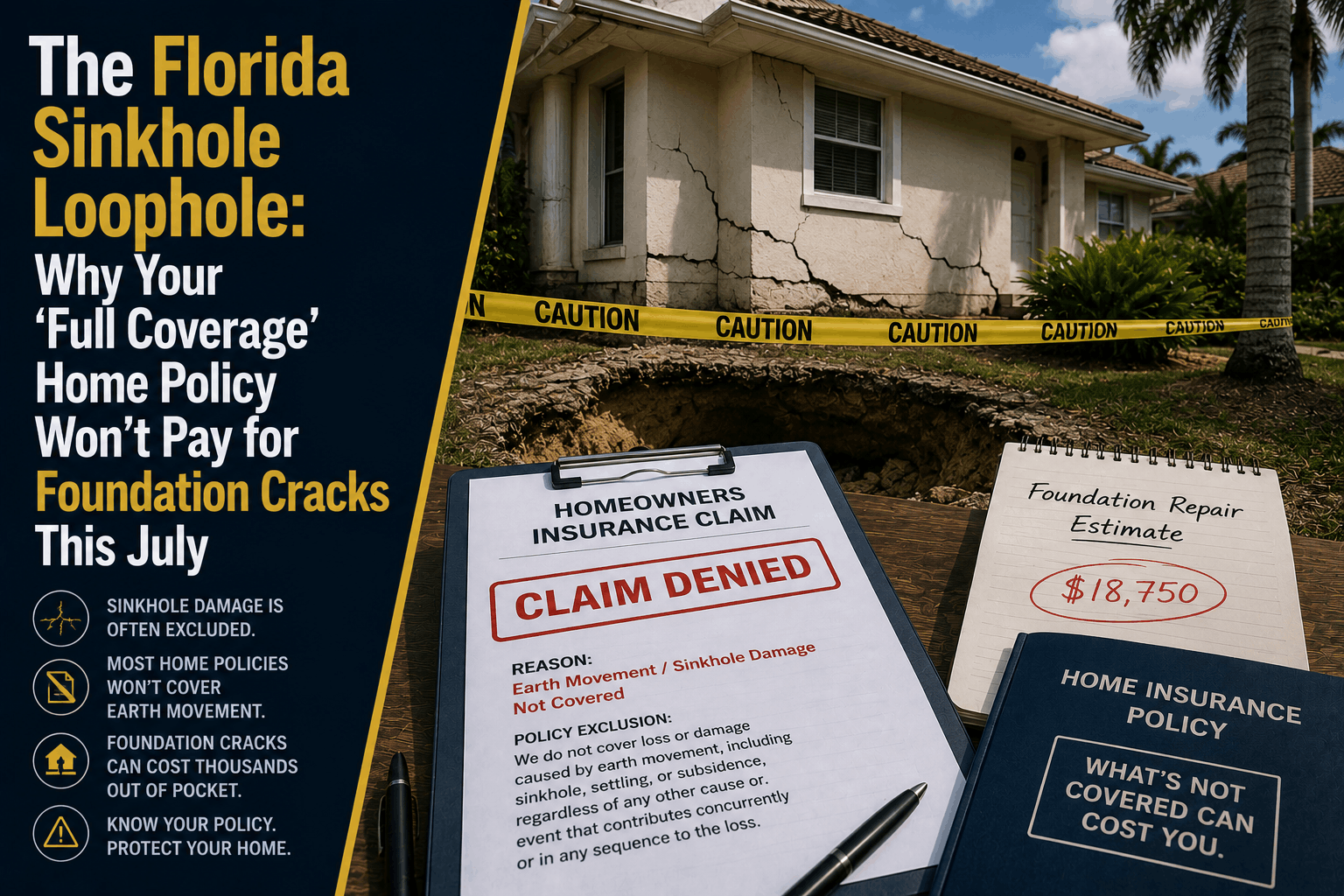

The Florida Sinkhole Loophole: Why Your "Full Coverage" Home Policy Won't Pay for Foundation Cracks This July

The Direct Answer

If you notice fresh staircase cracks in your exterior stucco, sloping interior floors, or windows that suddenly stick in their frames this July, your standard Florida "full coverage" homeowners policy will pay exactly $0 to fix them. Homeowners routinely assume their policy protects against subterranean land shifts, but standard Florida forms legally exclude sinkhole damage. Instead, state law only forces carriers to include a highly restrictive alternative called Catastrophic Ground Cover Collapse (CGCC). Under this strict legal definition, your insurer will completely deny your claim unless your home suffers an immediate, catastrophic event where the ground collapses abruptly, a hole is visible to the naked eye, the foundation is structurally ruined, and a government agency officially condemns and orders your home vacated. If your house is still standing and habitable despite severe foundation cracking, you fall completely into the loophole.

As the summer rain patterns saturate the porous limestone bedrock across the Treasure Coast this July, underground voids are shifting. Yet, thousands of property owners remain completely unprotected. Private insurance carriers aggressively lean on this statutory division to reject expensive foundation stabilization claims, shifting the massive cost of deep-grouting and underpinning entirely onto unprepared homeowners.

1. The Impossibly High Four-Part Legal Threshold

When underground erosion occurs beneath a property, it rarely looks like a dramatic Hollywood movie scene. Most sinkhole activity manifests slowly. The soils slowly ravel downward into limestone caverns, causing the home above to settle unevenly.

If you file a claim for these settling issues under your standard policy, a claims adjuster will immediately judge the damage against Florida Statute Section 627.706. To trigger a payout, your home must meet all four of these requirements simultaneously:

[Ground Collapses Abruptly]

\+ \[Visible Surface Hole\]

\+ \[Severe Foundation Damage\]

\+ \[Government Condemnation Order\] ──\> 100% PAID via Mandatory CGCC

──\> If ANY step is missing: $0 Payout

The Settlement Exclusion Squeeze

Because a house experiencing slow structural shifting does not feature a gaping, visible hole and has not been condemned by local Stuart building inspectors, it fails the statutory test. The carrier will legally categorize your multi-thousand-dollar foundation issue as basic "settling, cracking, or shrinking," which is explicitly excluded from standard property forms.

The structural and financial reality of navigating this loophole out of pocket is devastating:

- Minor Concrete Foundation Cracking: Even simple cracks that cause minor interior tile displacement require specialized deep-injection polyurethane foam or cosmetic stabilization. Local structural technicians command $5,000 to $12,000 for localized remediation, a cost completely rejected by standard policies.

- Systemic Subsurface Settlement: If a corner of your home begins sloping because of verified underground raveling, you must install heavy steel underpinning piers driven deep into the stable bedrock. Remediating a single compromised zone routinely costs $25,000 to $55,000 in pure engineering and contractor fees.

- Comprehensive Under-Home Stabilization: For severe structural shifting where the soil underneath the entire home footprint must be stabilized via low-mobility chemical grouting, homeowners face massive bills averaging $80,000 to $140,000. Without specific coverage, your entire household savings can be wiped out by a single subterranean shift.

The Testing Cost Trap: If you contest a denial and demand advanced geological testing, and the insurer's professional engineer rules that the foundation cracks were caused by clay shrinkage rather than true sinkhole activity, you can be held legally responsible to reimburse the carrier for up to 50% of the engineering testing costs, capped at $2,500 under state guidelines.

2. The July 2026 Environmental Squeeze: Why Now?

Allowing this gap to remain in your home insurance portfolio this summer leaves your personal wealth entirely exposed to seasonal climate risks. July represents a peak danger period for Florida foundations due to two specific forces:

- The Heavy Rain Hydrostatic Pressure Squeeze: As heavy summer downpours dump inches of water onto the local landscape, the weight of the water-logged topsoil increases exponentially. This sudden downward pressure forces weak upper soil layers to collapse into hidden underground limestone pockets that remained stable during the dry spring months.

- The Post-Drought Water Table Shift: When the local water table fluctuates rapidly between dry spells and sudden tropical weather systems, the internal buoyant pressure that supports the underground cavities is stripped away, causing immediate settling directly beneath heavy concrete home slabs.

3. How to Secure Your Property Lines Against Land Shifts

If your home asset is currently sitting on a standard, un-audited property contract, your financial stability is entirely at the mercy of the soil beneath your feet. At Walker Insurance Agency, we advise property owners to protect their foundations using a precise, three-step defensive layout:

- Step 1: Check Your Declarations Page for a "Sinkhole Loss Endorsement." Pull your complete multi-page policy document. If you only see "Catastrophic Ground Cover Collapse," you have zero protection for foundation cracks. Look specifically for an optional rider labeled "Sinkhole Loss Coverage."

- Step 2: Document Baseline Cracks Prior to Major Storm Systems. Take high-resolution photos of your garage floor, exterior perimeter walls, and interior doorways this July. Having a dated visual baseline makes it significantly harder for an adjuster to claim your foundation damage is ancient, pre-existing wear and tear.

- Step 3: Undergo a Pre-Binding Visual Home Inspection. Because Florida private carriers are legally permitted to deny optional sinkhole riders if a home already shows structural distress, work with an independent broker to secure a clean visual inspection report while your home is stable, allowing you to bind the necessary endorsement safely.

Why Working with an Independent Agency is Vital

Attempting to manage complex coastal property risks through a generic smartphone app or a standard corporate online form ensures you will miss the statutory distinctions that dictate whether your foundation repair bill is paid or denied. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to protect your home.

The Walker Advantage:

- Statutory Text Dissection: We meticulously review your underlying policy language to confirm whether you are limited to the narrow, mandatory collapse definition or fully protected against standard sinkhole loss.

- Localized Geotechnical Alignment: We understand the unique soil compositions across Stuart and Martin County, ensuring your policy limits align with actual structural engineering costs in our region.

- Carrier Market Access: As the stabilizing Florida market introduces 20 brand-new private insurance companies to the state, we continuously shop your profile to locate providers that still offer comprehensive, optional sinkhole endorsements at realistic premium floors.

FAQ

1. Does a standard "All-Perils" policy cover sinkhole damage automatically?

No. An "All-Perils" or "Open-Perils" policy covers your home against unexpected losses unless the cause of loss is explicitly excluded. Earth movement, settling, shifting, and sinkholes are universal exclusions on standard Florida home insurance forms. You must purchase a separate Sinkhole Loss Endorsement for your foundation cracks to be covered.

2. If a sinkhole damages my driveway or pool deck, will optional sinkhole insurance fix it?

No. Under Florida Statute Section 627.706, neither mandatory catastrophic ground cover collapse coverage nor optional sinkhole loss endorsements cover detached structures, driveways, sidewalks, swimming pools, patio decks, or open land. The insurance coverage applies strictly to the primary, insured residential structure and its direct foundation footprint.

3. How large are the deductibles for a verified sinkhole loss claim?

They are substantial. Florida law allows insurance providers to apply separate, specific deductibles for sinkhole claims, usually structured as a percentage of your dwelling coverage limit (1%, 2%, 5%, or 10%). For a home insured for $400,000 with a 10% sinkhole deductible, you are responsible for the first $40,000 of foundation repair costs out of pocket before the carrier pays the remainder.

Insulate Your Property Boundaries Before the Ground Shifts

Your foundation is the anchor of your entire life, but leaving its underground protection to a basic, un-vetted property insurance policy is an administrative gamble that can instantly ruin your household budget. True peace of mind requires pulling back the curtain on your policy’s statutory exclusions and ensuring your written contract matches the geological reality of your lot.

Take control of your structural protection today. Contact Walker Insurance Agency for a comprehensive portfolio evaluation. We provide the visibility you need to eliminate hidden sinkhole loopholes, deploy high-limit comprehensive foundation riders, and protect your family's hard-earned wealth safely in Stuart.

[GET A FREE QUOTE TODAY]

Call our personal lines division at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your property boundaries today.

Related Articles

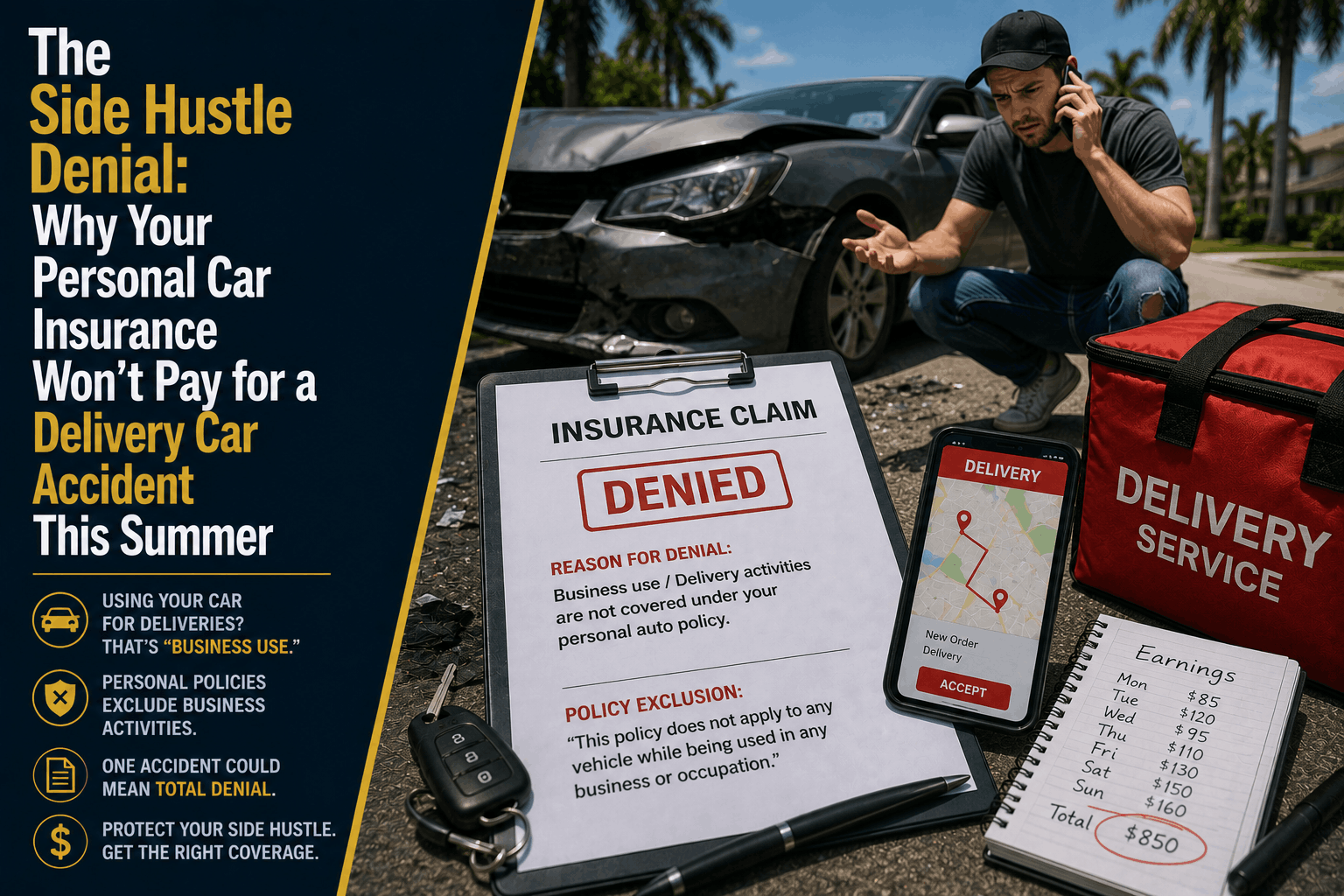

Does Personal Car Insurance Cover Delivery Accidents? (2026)

Driving for DoorDash, Instacart, or Amazon Flex in Stuart? Discover why your personal auto policy won't pay a single dollar for a delivery crash this year.

Read More →

The Delivery Car Side Hustle Trap: Personal Auto Exclusions in 2026

Thinking of driving for DoorDash, Uber Eats, or Instacart in Stuart this summer? Learn why your personal car insurance will completely deny a delivery accident claim.

Read More →

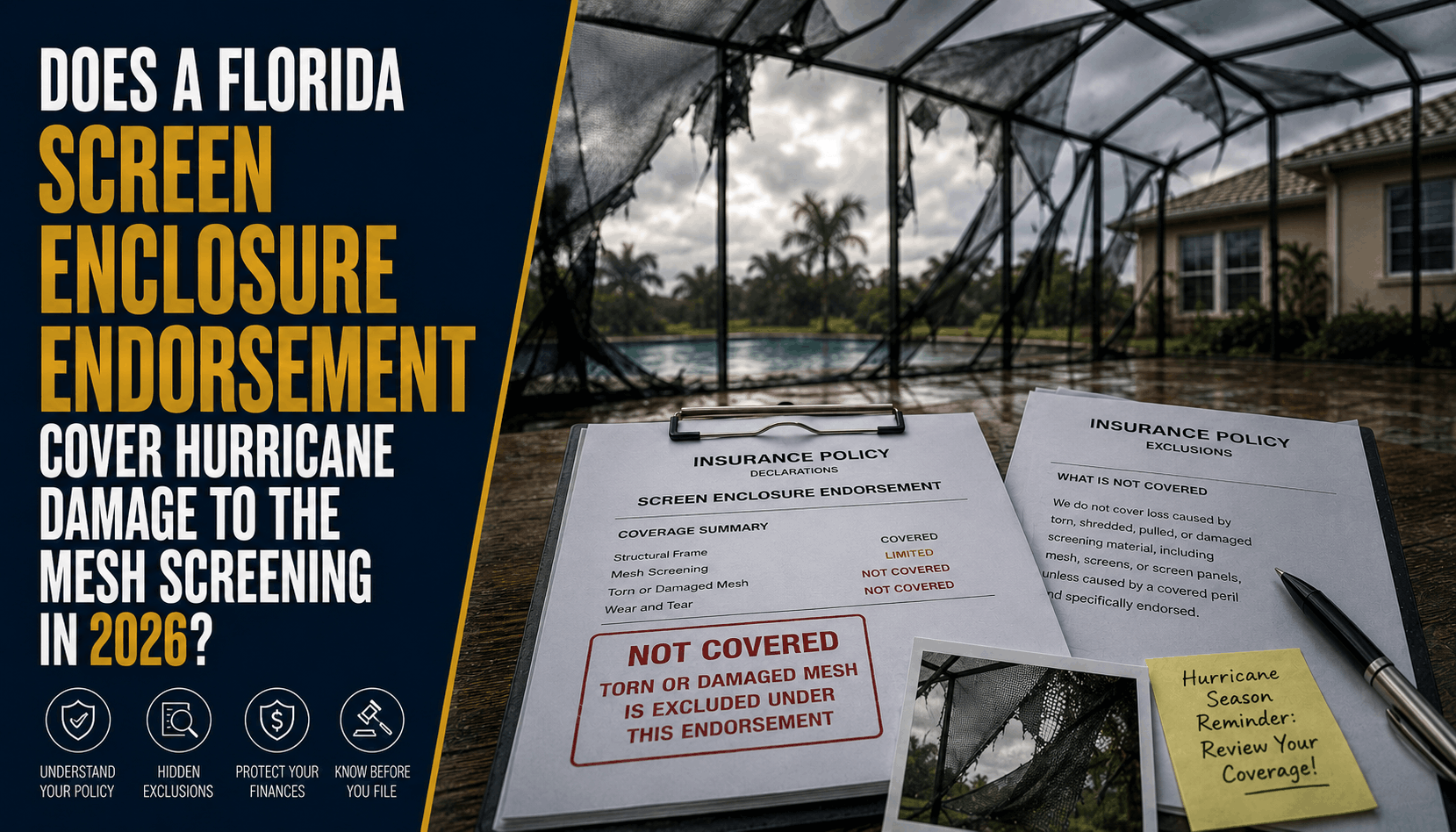

Does a Florida Screen Endorsement Cover Mesh Damage? (2026 Rules)

Think your pool enclosure insurance covers everything? Discover "The Frame-Only Trick" that leaves Florida homeowners paying 100% out of pocket for torn mesh in 2026.

Read More →