5 Common Insurance Myths Debunked | Florida Insurance Guide

5 Common Insurance Myths Debunked: The Truth for Florida Residents

Navigating the insurance landscape in Florida can be as complex as a summer storm. With unique risks like hurricanes, high traffic density, and specific state regulations, residents often find themselves relying on "street wisdom" that is simply incorrect. These misconceptions, or insurance myths, are more than just harmless talk; they can lead to significant financial gaps when you need protection the most.

Whether you are a homeowner in Stuart or a business owner looking to secure your Florida-based assets, understanding the reality of your policy is essential. In this guide, we will strip away the confusion and provide you with the transparency and visibility you need to make informed decisions about your coverage.

The Problem with Insurance Misinformation in Florida

In Florida, insurance is not just a monthly bill; it is a critical safety net. However, misinformation spreads quickly. When policyholders believe myths—such as thinking the state's minimum coverage is "enough"—they unknowingly leave their homes, vehicles, and savings exposed to litigation and total loss.

The problem is twofold: first, myths lead to underinsurance, and second, they prevent people from seeking better rates because they misunderstand how premiums are actually calculated. In a state where litigation and weather events are frequent, operating on myths is a high-risk gamble that most families and business owners cannot afford to lose.

Myth 1: The "Red Car" Premium and Vehicle Color

One of the most persistent insurance myths in Florida is that driving a red car will automatically increase your insurance rates. The legend suggests that red cars are sportier, attract more police attention, and therefore are more expensive to insure.

The Reality: Insurance companies do not even ask for the color of your vehicle during the quoting process. They are interested in data-driven risk factors provided by your Vehicle Identification Number (VIN):

- Safety Ratings: How well the car protects occupants in a crash.

- Repair Costs: The price of parts and specialized labor for your specific model.

- Theft Rates: Certain models are targeted more frequently by thieves.

- Engine Performance: High-performance engines carry higher risk, regardless of paint color.

Myth 2: Why Florida’s Minimum Coverage is Often Not Enough

Many drivers believe that if they carry the "state minimum" insurance, they are fully protected. In Florida, the requirements focus heavily on Personal Injury Protection (PIP) and Property Damage Liability (PDL).

Factors that make minimum coverage a risk:

- Low Liability Limits: If you cause an accident that results in $50,000 of damage and you only have $10,000 in coverage, you are personally responsible for the $40,000 gap.

- High Medical Costs: Medical expenses in Florida can skyrocket quickly. PIP only covers 80% of medical bills, up to $10,000.

- Uninsured Motorists: Florida has a high rate of uninsured drivers. If you only have minimum coverage, you may not have protection for your own vehicle if an uninsured driver hits you.

Myth 3: The Dangerous Gap in Homeowners Flood Coverage

A common and potentially devastating myth is that a standard homeowners insurance policy covers flood damage. Given Florida's geography, this misconception is particularly dangerous.

When it applies vs. when it doesn't:

- Homeowners Policy: Typically covers "sudden and accidental" water damage from inside the house (like a burst pipe).

- Flood Insurance: This is a separate policy required for damage caused by "rising water" from the outside (storm surges, heavy rain, or overflowing bodies of water).

Without a dedicated flood policy, many Florida residents find themselves with zero coverage after a hurricane or tropical storm, leading to a complete loss of their property's visibility and value.

Myth 4: Life Insurance is Only for the "Breadwinner"

There is a widespread belief that life insurance is only necessary for the spouse who brings home the primary paycheck. This ignores the massive economic contribution of a stay-at-home parent or partner.

Why stay-at-home partners need coverage:

- Service Replacement: If a stay-at-home parent passes away, the cost of childcare, household management, and transportation can exceed $50,000 a year.

- Debt Protection: Life insurance can cover mortgages and personal loans, ensuring the family stays in their home.

- Funeral Costs: Immediate final expenses can put a sudden strain on a single-income household.

Why Working with an Independent Agency Makes the Difference

Why try to navigate these myths alone? Working with an independent agency like Walker Insurance Agency provides a layer of expert advocacy that "big box" insurers can't offer.

Practical Benefits:

- Comparison Shopping: We compare multiple carriers to find the best rate, debunking the myth that "one size fits all."

- Local Expertise: We understand the specific risks of the Stuart, FL area and the wider Florida market.

- Claim Advocacy: If a disaster strikes, you have a local partner to help you navigate the process.

- Audit of Coverage: We provide the visibility you need by identifying gaps in your current policies that you might not even know exist.

FAQ

1. Does my credit score affect my insurance rates in Florida? Yes. Most insurers in Florida use a credit-based insurance score to help determine risk. A higher score typically leads to lower premiums.

2. Is my business insurance tax-deductible? In many cases, yes. Generally, the cost of business insurance is a deductible business expense if it is for the purpose of trade, business, or profession.

3. Do I need insurance for a home office in Florida? Standard homeowners policies offer very limited coverage for business equipment. If you run a business from home, you likely need a home-based business endorsement or a separate policy.

4. Can I change my insurance agent at any time? Yes. You are not "locked in" to an agent. You can switch to an agency that provides better service and more transparent visibility of your policies at any point.

Local Business Schema

Don’t Leave Your Future to Chance

Myths belong in storybooks, not in your financial planning. Every day you operate under a misconception about your coverage is a day you are at risk. In Florida, the cost of a mistake can be life-altering.

Stop guessing and start protecting. Contact Walker Insurance Agency today for a comprehensive coverage audit. We will help you see through the myths and provide the visibility you need to ensure your home, family, and business are truly secure.

[GET A FREE QUOTE TODAY] Call us at +1-772-247-0269 or visit our office in Stuart, FL. Your peace of mind is just one call away.

Related Articles

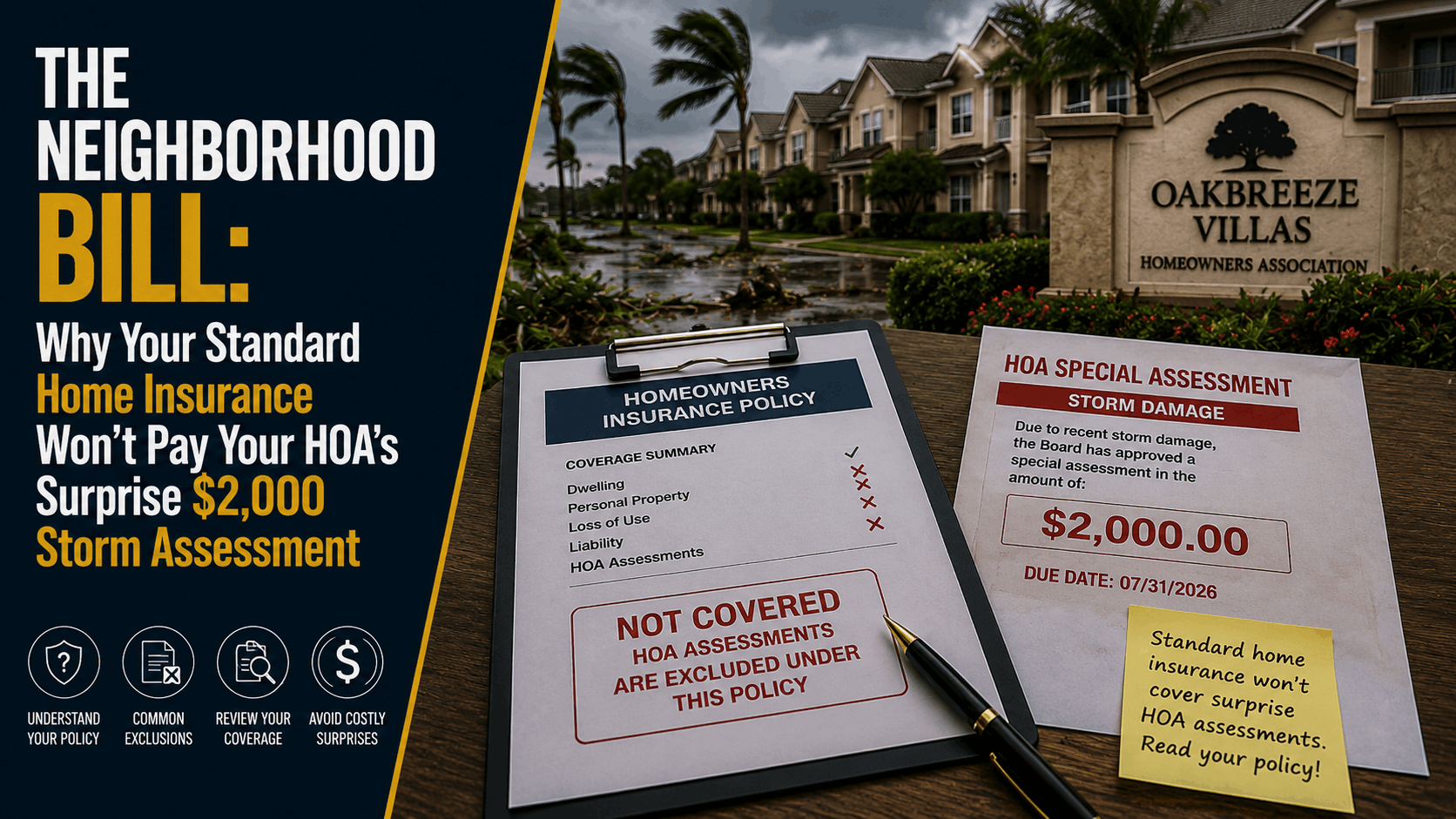

Why Home Insurance Won't Pay Your HOA Storm Assessment (2026)

Received a surprise HOA special assessment after a storm? Discover the critical loss assessment loopholes leaving Stuart homeowners completely exposed in 2026.

Read More →

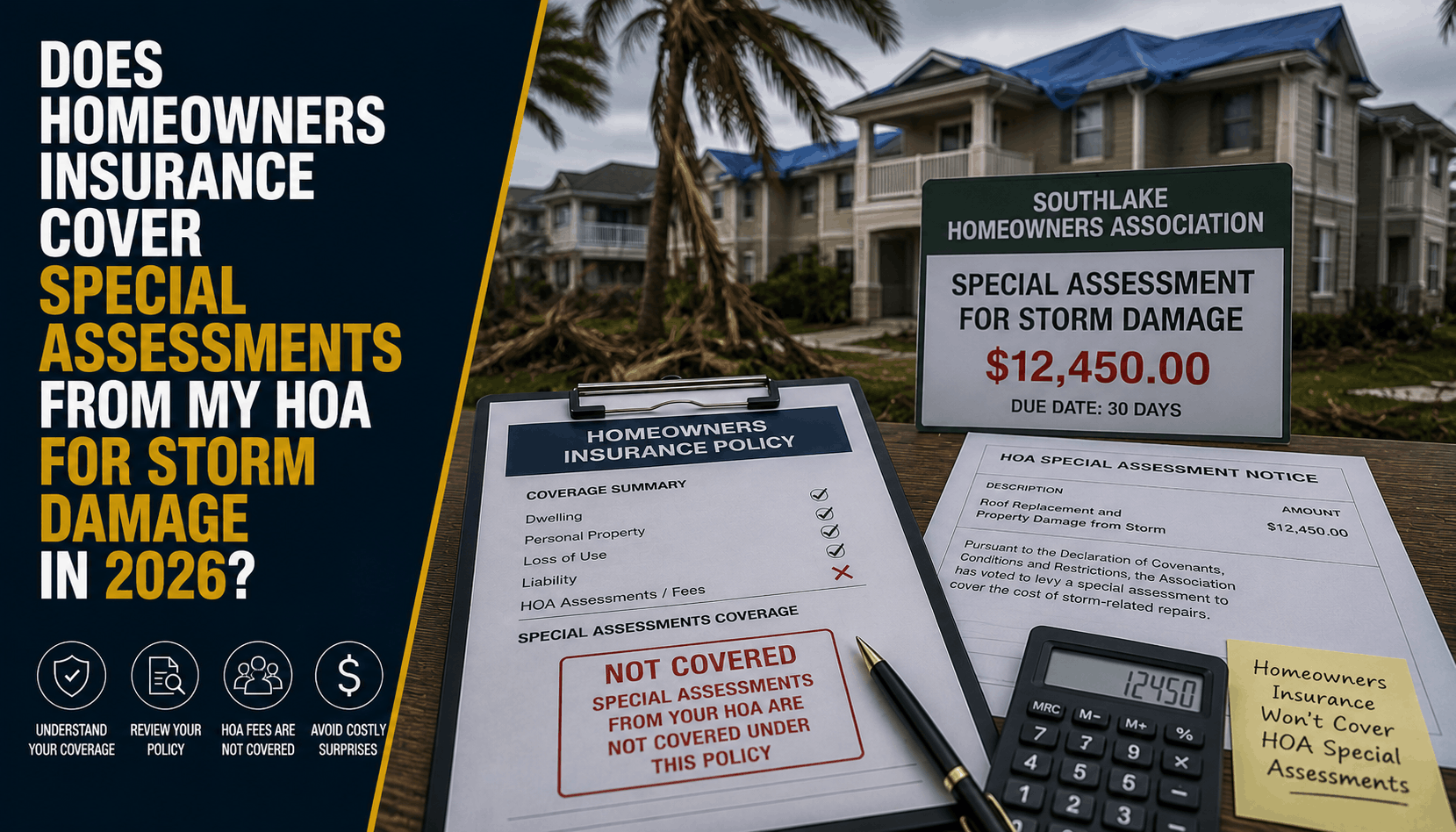

Does Florida Home Insurance Cover HOA Storm Special Assessments? (2026)

Think your Stuart home or condo insurance automatically covers an HOA special assessment after a hurricane? Discover the loss assessment limits leaving local owners exposed.

Read More →

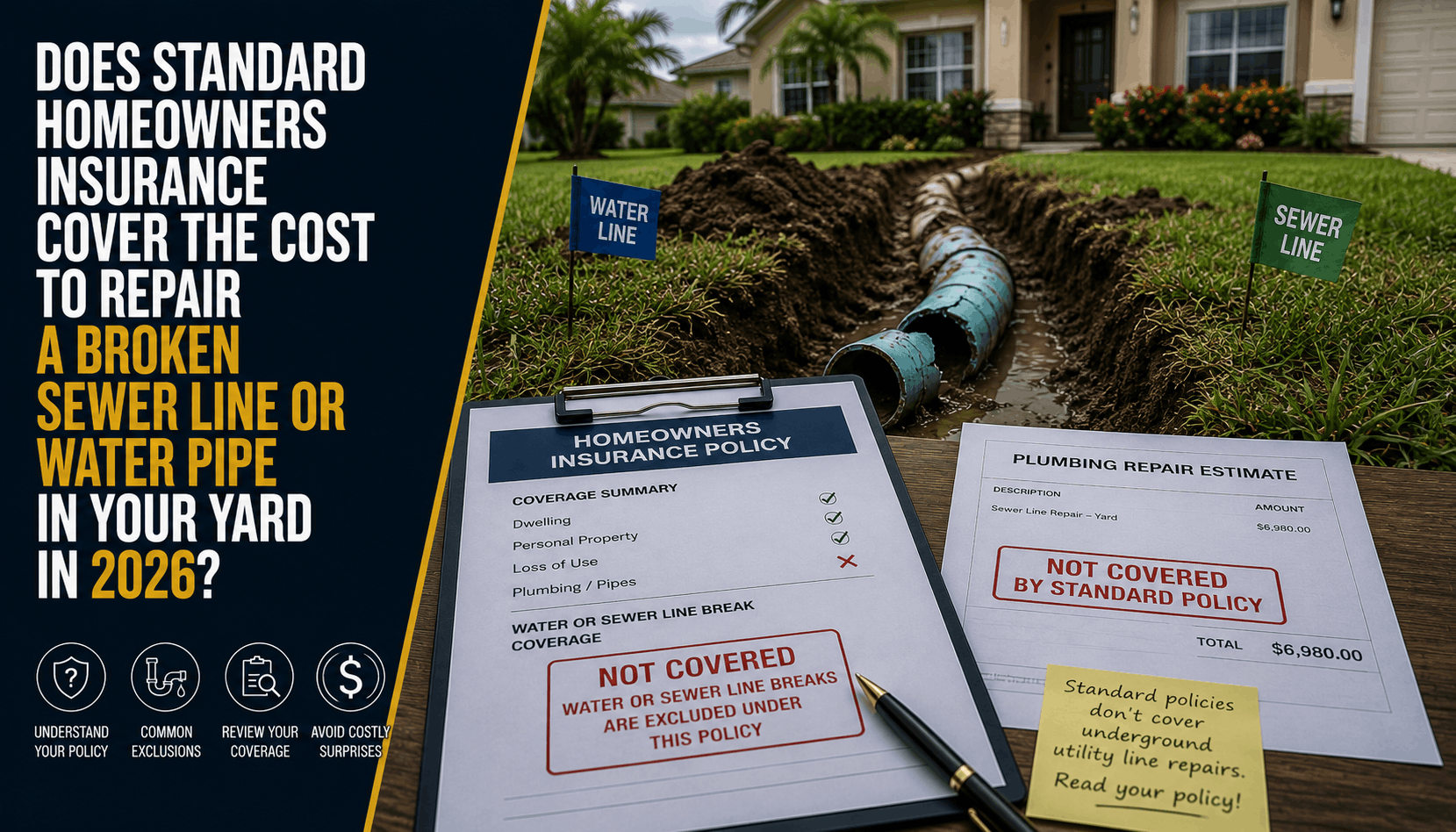

Does Home Insurance Cover Broken Pipes in the Yard? (2026)

Discover why standard homeowners insurance completely denies the cost to repair a broken sewer line or water main in your yard, and how Stuart homeowners can fix this gap.

Read More →