Florida Car Accident Medical Treatment Deadline (2026 PIP Guide)

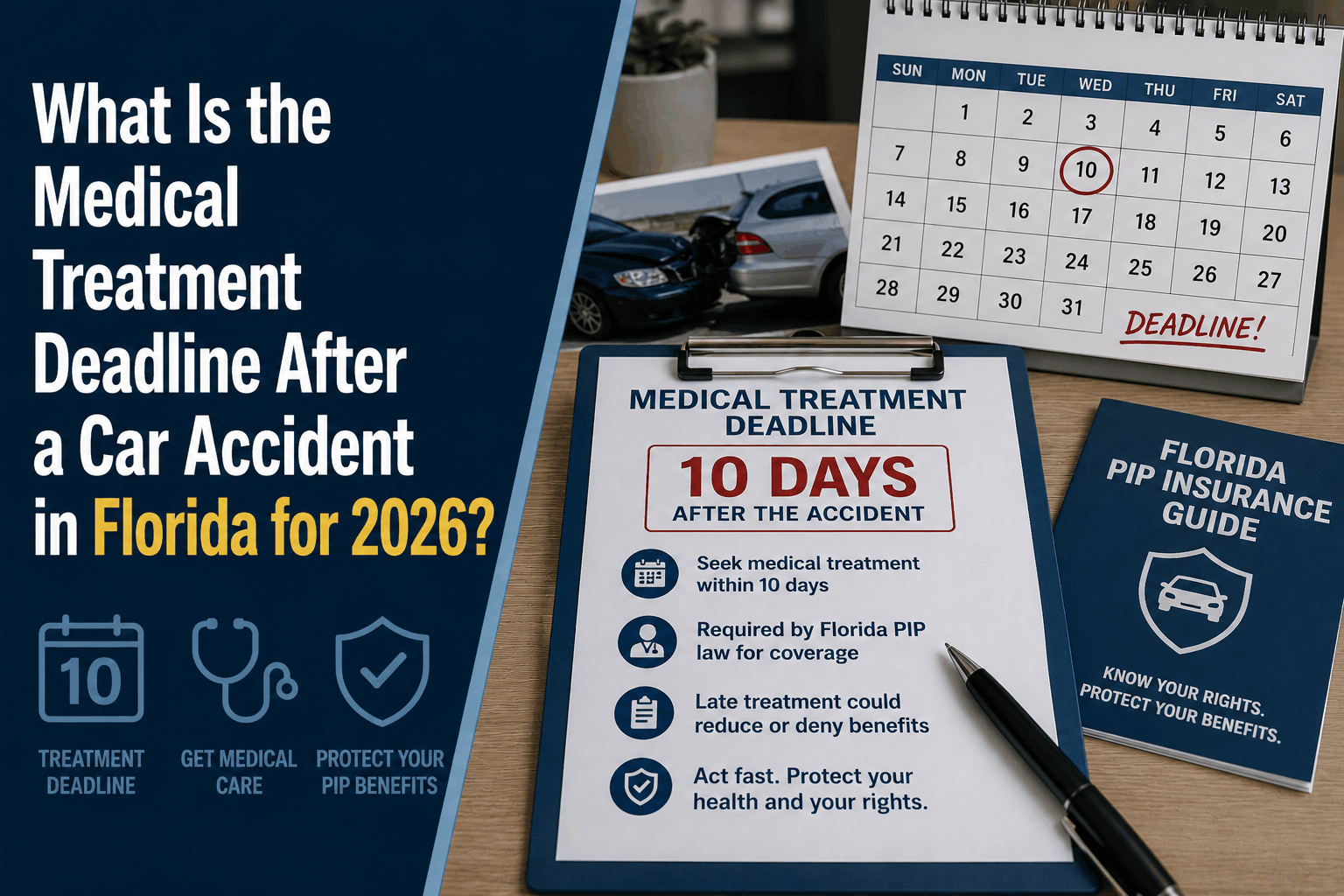

What Is the Medical Treatment Deadline After a Car Accident in Florida for 2026?

The Direct Answer: Under Florida Statute § 627.736, you have exactly 14 calendar days from the date of a car accident to seek initial medical treatment. If you fail to receive an evaluation from a qualified medical provider within this two-week window, you automatically forfeit your entire $10,000 Personal Injury Protection (PIP) benefit, regardless of how severe your injuries are or who caused the crash.

To achieve total visibility over your recovery, you must also understand that simply visiting a clinic within 14 days isn't enough to unlock your full safety net. Unless a licensed physician explicitly diagnoses you with an Emergency Medical Condition (EMC) during your treatment timeline, your medical benefits are capped at a mere $2,500.

1. How the 14-Day Clock Works

The 14-day rule functions as a strict statutory boundary line. In the stable 2026 Florida insurance market, claims adjusters aggressively audit timestamps, leaving no room for late exceptions.

- Day Zero: The clock begins ticking the exact day the car accident occurs.

- The Deadline: You must have an initial medical consultation completed by the midnight cutoff of Day 14.

- No Hardship Waivers: The state provides absolutely no extensions for hidden or delayed symptoms, lack of transportation, or a simple misunderstanding of the insurance codes.

2. Who Can Provide Qualifying Treatment?

Not every healthcare visit satisfies the statutory requirement to open a PIP claim. To preserve your $10,000 in benefits, your initial 14-day visit must be conducted by one of these state-approved entities:

- Medical Doctors (MD) or Doctors of Osteopathy (DO)

- Chiropractic Physicians (DC)

- Dentists (vital for facial/jaw impacts)

- Hospital-owned emergency rooms or urgent care facilities

- Licensed EMTs or paramedics providing on-scene emergency transport

Warning: Initial visits to physical therapists, massage therapists, or acupuncturists do not qualify under Florida law to satisfy the 14-day requirement. You must see a primary qualifying provider first.

3. The 2-Year Lawsuit Deadline Connection

A major point of confusion for Florida drivers is the difference between their medical deadline and their legal deadline.

Following sweeping tort reforms, the statute of limitations for filing a personal injury lawsuit against an at-fault driver is two years from the date of the accident. While you have two years to take legal action, you still only have 14 days to open your medical benefits. If you miss the 14-day window, you lose your PIP medical cash immediately, which severely weakens your ability to negotiate a third-party injury settlement down the road.

[Day 0: Car Accident] ──> [Day 14: Strict PIP Medical Treatment Deadline] ──> [Year 2: Strict Lawsuit Filing Cutoff]

4. The Trap of Delayed Soft-Tissue Trauma

The 14-day rule exists to combat insurance fraud, but it frequently penalizes responsible drivers who experience delayed-onset injuries.

Immediately following a crash, your body releases a massive flood of adrenaline that masks physical trauma. Soft-tissue damage—such as severe whiplash, herniated discs, and minor concussions—frequently takes 3 to 7 days to manifest as severe muscle spasms, nerve pain, or blinding headaches. If you spend those first two weeks waiting to see if the stiffness "just goes away," you will blow past the statutory window and be left personally responsible for 100% of your medical bills.

Why Working with an Independent Agency is Vital

When the legal parameters of Florida auto insurance penalize minor delays, purchasing a policy through an automated app without professional guidance is incredibly high-risk. At Walker Insurance Agency, we give you the visibility you need to protect both your health and your assets.

The Walker Advantage:

- Claims Concierge Action: The moment you report an incident to us, we immediately coordinate the timeline steps required to secure your PIP and EMC documentation.

- MedPay Shield Stacking: We advise clients to protect themselves by adding Medical Payments (MedPay) coverage. MedPay covers the 20% co-insurance gap that standard PIP leaves behind, creating a 100% medical safety net out of the gate.

- Market Stabilization Evaluation: As auto premiums level off following the legal overhauls, we shop the entire Florida marketplace to connect you with highly rated carriers that prioritize fast, fair claims handling over automated denials.

FAQ

1. What happens if I go to an urgent care clinic on Day 15?

Your insurance company is legally permitted to deny your medical claim entirely. You will have to pay for your diagnostics, imaging, and treatment out of pocket or through your private health insurance.

2. Does PIP pay for 100% of my medical bills within the 14 days?

No. Florida PIP covers 80% of reasonable and necessary medical expenses and 60% of documented lost wages up to your policy limit, provided you meet the 14-day deadline and secure an EMC finding.

3. What if I am hospitalized immediately after the crash?

If you are taken to the hospital via ambulance or admitted to an emergency room on the day of the accident, your hospital intake records automatically satisfy the 14-day rule and establish your clinical documentation timeline.

Protect Your Health and Your Policy Limits

In the modern Florida auto market, a minor administrative delay can instantly erase the medical safety net you pay for every single month. Real protection requires taking charge of your rights before an emergency occurs on the highway.

Audit your auto coverage limits today. Contact Walker Insurance Agency for a comprehensive policy evaluation. We provide the visibility you need to structure your deductibles safely, bypass costly claim traps, and lock in the most competitive rates available in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your drive today.

Related Articles

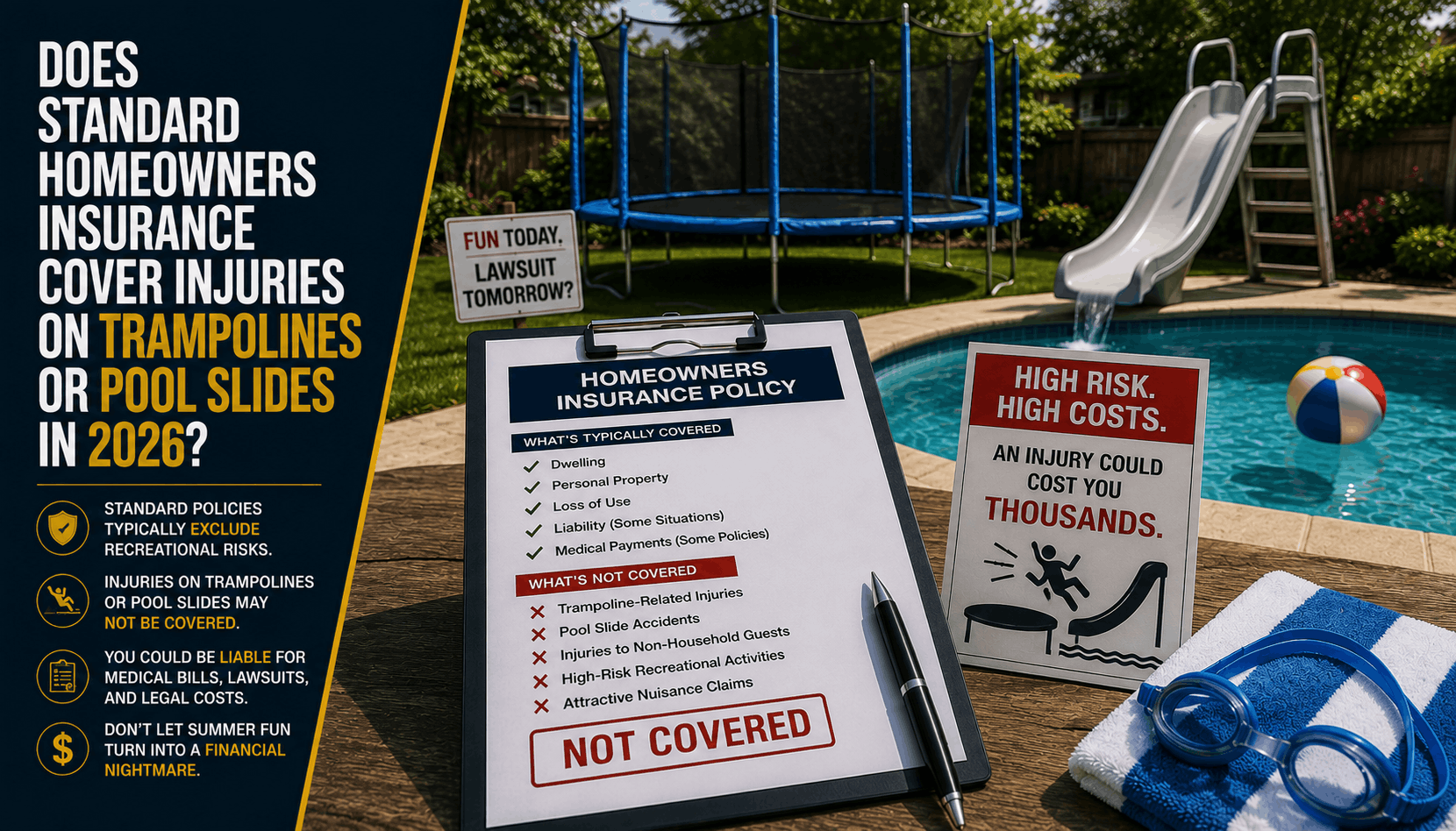

Does Homeowners Insurance Cover Trampolines or Pool Slides? (2026)

Planning summer fun in Stuart, FL? Discover why trampolines and pool slides are major homeowners insurance liability traps that can lead to dropped coverage.

Read More →

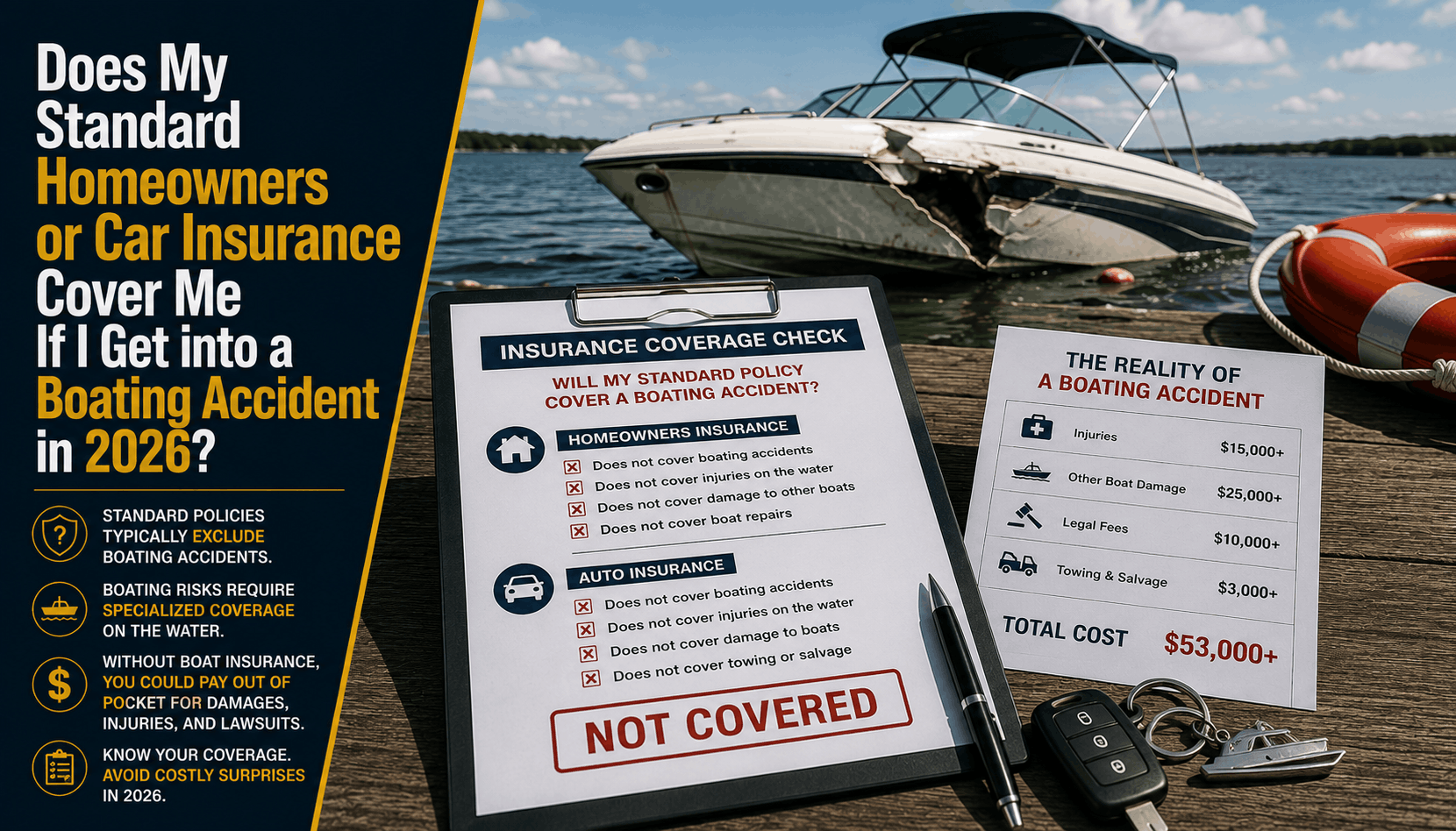

Does Home or Auto Insurance Cover Boating Accidents? (2026)

Planning a boat day in Stuart? Learn why relying on your home or auto insurance policies for watercraft liability is a dangerous financial gap.

Read More →

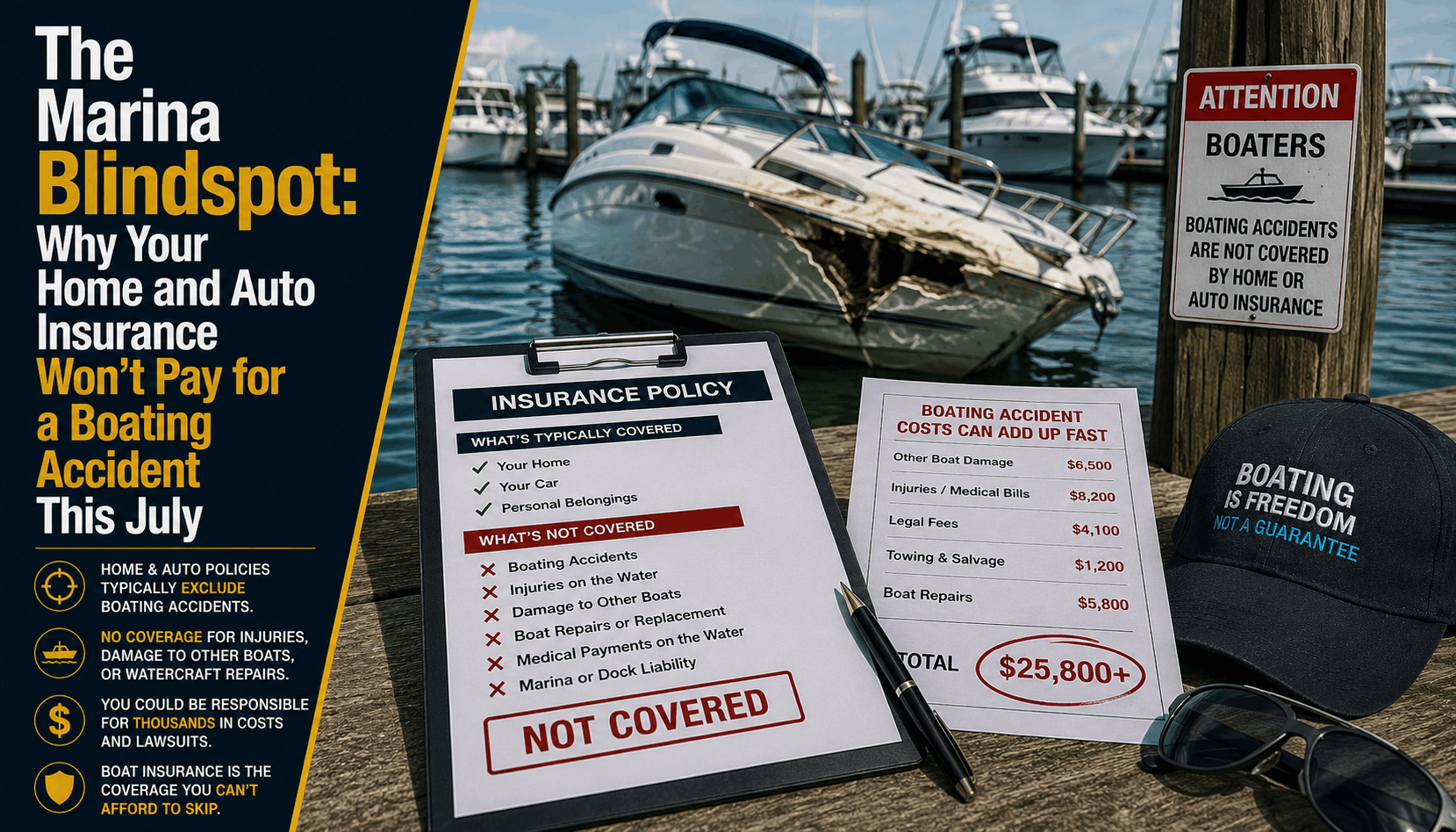

Why Home and Auto Insurance Won't Cover Boat Accidents (2026)

Planning a July boat day in Stuart, FL? Discover why relying on your home or auto insurance policies for watercraft liability is a dangerous financial blindspot.

Read More →