Why Home and Auto Insurance Won't Cover Boat Accidents (2026)

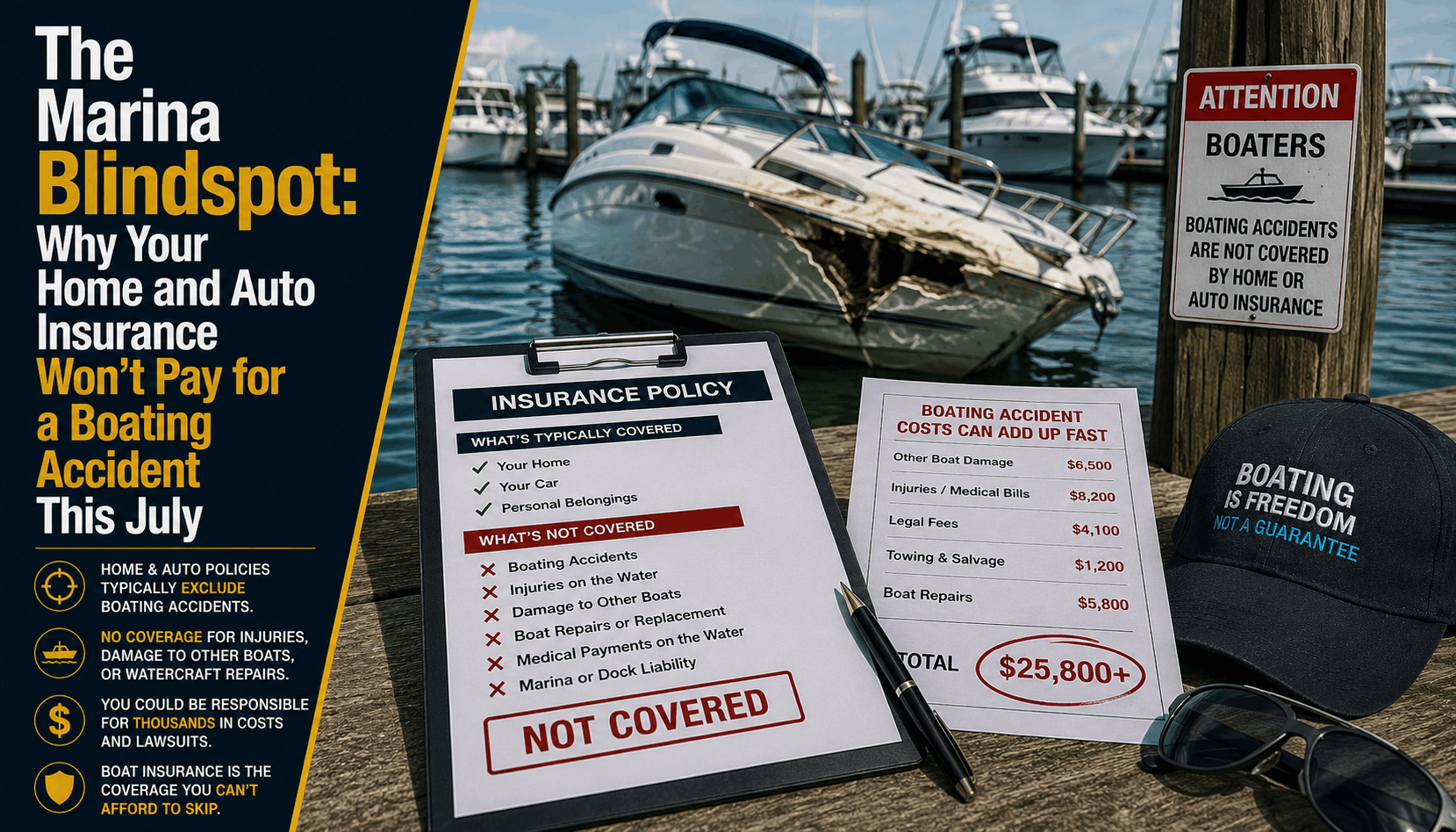

The Marina Blindspot: Why Your Home and Auto Insurance Won't Pay for a Boating Accident This July

The Direct Answer

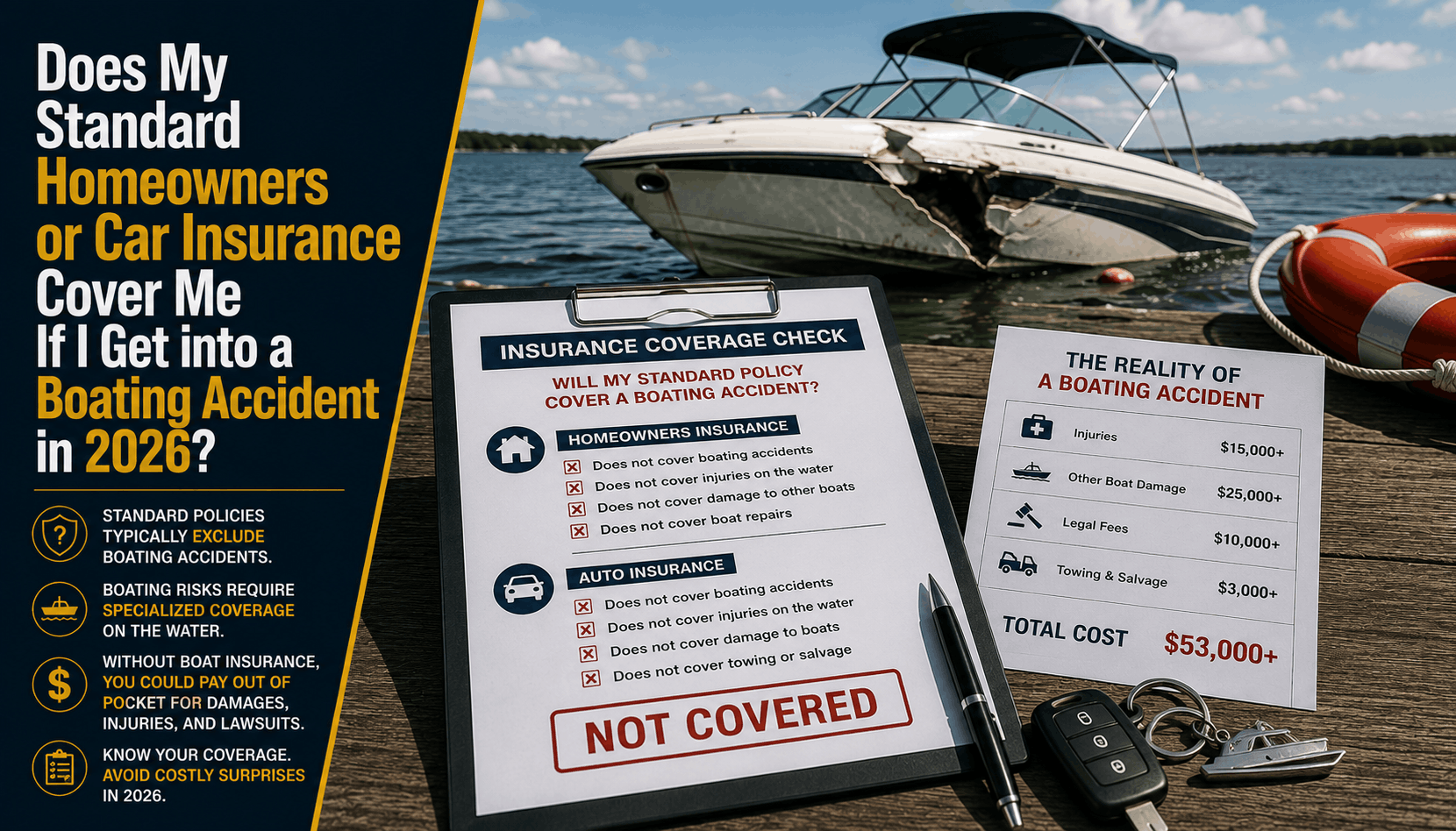

The short answer is absolutely not—your standard homeowners and auto insurance policies will not cover physical damage, medical bills, or liability claims resulting from a boating accident. A common and highly dangerous misconception among Florida boaters this July is that a personal umbrella, home, or auto policy automatically stretches to cover their recreational watercraft. In reality, auto insurance stops completely at the water's edge, and standard homeowners policies (HO-3) place strict, severe limits on watercraft—typically capping physical damage coverage at just $1,000 for small, non-motorized boats or tiny outboard motors under 25 horsepower. If you operate a standard center console, jet ski, or pontoon boat along the St. Lucie River this summer without a dedicated, standalone marine policy, any collision or liability claim will be denied instantly, exposing you to catastrophic out-of-pocket expenses.

With July's peak summer heat bringing high traffic to Stuart's local sandbars and marinas, marine liability exposure is at an all-time high. Relying on basic land-based policies to shield your assets on the water is a financial risk that could cost you your home.

1. The Home vs. Auto Fallacy: Deconstructing the Exclusion Zones

Many coastal property owners assume that because they park their boat on a trailer in their driveway, it shares the same robust liability protections as their cars or home structures. This is a critical legal misunderstanding:

- The Auto Insurance Barrier: Your auto insurance policy only covers your boat while it is physically hitched to your towing vehicle and being transported on dry land. If a distracted driver rear-ends your trailer on Dixie Highway, your auto policy covers the damage. The microsecond your boat slides off the trailer and splashes into the marina boat ramp, your auto policy's physical damage and liability protection drops to exactly $0.

- The Homeowners Insurance Mirage: While a standard home policy may extend minor, limited liability coverage to extremely small, low-speed vessels (such as a kayak, canoe, or a small sailboat under 26 feet without an engine), it completely excludes any standard motorized pleasure craft.

[ Your Boat on the Trailer ] ──> Covered by Auto Policy (Transit Only)

[ Your Boat in the Driveway ] ──> Limited Physical Cover by Home Policy (Excludes Liability)

[ Your Boat in the Water ] ──> ZERO COVERAGE without a Dedicated Marine Policy

If you operate a standard 21-foot boat with a 150-horsepower outboard motor, you have absolutely zero liability protection under your home or auto policy the moment you start the engine.

2. Real-World Marina Risks: The Expenses Your Land Policies Exclude

Operating a vessel on public waterways carries unique, high-stakes liabilities that land-based policies are physically and legally unequipped to handle. If you cause an accident in Stuart’s waters this July, a dedicated marine policy is the only barrier protecting you from the following expenses:

- Environmental Wreck Removal & Fuel Spill Liability: If your vessel collides with a channel marker or another boat and sinks, you are legally responsible under federal maritime law for recovering the wreck. Furthermore, if your fuel tank ruptures and leaks oil into protected waters, the Coast Guard can levy massive clean-up fines. Standard home insurance will never cover marine pollution remediation or mandatory wreck salvage, which frequently exceeds $20,000.

- The Shared Slip Liability: If a fire starts in your boat's electrical system while it is docked at a local Stuart marina, and the flames spread to destroy neighboring vessels or the marina's dock slips, you are personally liable for the millions of dollars in structural damage. Marina slip contracts explicitly require you to carry high-limit marine liability insurance for this exact reason.

- Water Sports Liability: Pulling family or friends on wakeboards, tubes, or waterskis is a summer staple. If a skier is injured while being towed by your boat, standard home and auto policies will exclude the medical and legal claims. Dedicated boat insurance includes specific water sports liability riders to shield your personal assets.

3. How to Properly Insure Your Vessel Before Launching This July

Protecting your family, your assets, and your vessel requires transitioning your coverage off the land and onto the water. At Walker Insurance Agency, we advise local boaters to implement these three crucial steps before heading to the boat ramp:

- Step 1: Secure an Agreed Value Marine Policy. Avoid "Actual Cash Value" policies that depreciate your boat's worth over time. An "Agreed Value" policy ensures that in the event of a total loss (like a major storm or sinking), you receive the exact insured value stated on your policy declarations page without depreciation.

- Step 2: Match Your Marine Liability to Your Net Worth. Do not opt for basic, low-limit liability. Ensure your marine liability limits (including Fuel Spill Liability and Medical Payments) match or exceed the liability limits on your primary home and auto policies. This allows your personal umbrella policy to sit properly on top of your watercraft coverage.

- Step 3: Verify Your Navigational Limits. Marine policies carry strict geographical boundaries. Ensure your policy's "navigational limits" explicitly cover the entire Florida coastline, the Bahamas (if you plan to cross the Gulf Stream), and the inland waterways you intend to traverse this summer.

Why Working with an Independent Agency is Vital

Boating insurance is not a one-size-fits-all product. Navigating the complexities of marine warranties, lay-up periods, and salvage coverage requires specialized local knowledge. At Walker Insurance Agency, we cross-reference your lifestyle with Florida’s top marine underwriters to keep your summer safe.

The Walker Advantage:

- Multi-Policy Coordination: We align your home, auto, marine, and personal umbrella policies to guarantee there are no hidden liability gaps when transitioning from land to sea.

- Sourcing Specialized Coverages: We shop specialized marine carriers to secure critical riders, including towing assistance, fishing equipment protection, and dock contract compliance.

- Local Treasure Coast Expertise: We live and work in Stuart. We understand local waterway hazards, marina requirements, and storm risks, giving you tailored, real-world advice.

FAQ

1. Does my personal umbrella policy cover my boat if I don't have a primary boat insurance policy?

No. Personal umbrella policies are designed to act as an "excess" layer of protection on top of existing primary policies (like auto, home, or watercraft liability). If you do not have an active, primary boat insurance policy that meets the underlying liability limits required by your umbrella carrier, your umbrella policy will not pay for watercraft accidents.

2. If my friend is driving my boat and causes an accident, whose insurance covers it?

Under a dedicated marine policy, coverage typically "follows the boat," meaning permissive operators (friends or family members driving with your permission) are covered under your policy. However, this coverage is entirely absent if you are relying on a home policy, and any "guest operator" coverage is subject to strict exclusions on cheap, cut-rate marine contracts.

3. What is a "Lay-Up Period" in a boat insurance policy, and how does it affect my July coverage?

A lay-up period is a specified timeframe during the winter months (e.g., November to April) when you agree not to use your boat in exchange for a lower premium. If your policy has an active lay-up clause and you take your boat out during those restricted months, you will have no coverage. Fortunately, because July is the peak of the Florida boating season, your policy will be fully active, but it is vital to review your declarations page to confirm your operational months.

Navigate Stuart's Waterways with Real Peace of Mind

Your boat is a source of family memories, but treating it like a standard land vehicle is an administrative gamble that can leave your entire estate exposed to marine lawsuits and federal fines. True protection requires securing dedicated coverage built specifically for the unpredictable dynamics of the open water.

Take control of your watercraft protection today. Contact Walker Insurance Agency for a comprehensive marine portfolio evaluation. We provide the specialized guidance you need to eliminate hidden coverage blindspots, secure high-limit marine liability, and protect your hard-earned assets both on land and at sea.

[GET A FREE QUOTE TODAY]

Call our personal lines division at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your property boundaries today.

Related Articles

Does Home or Auto Insurance Cover Boating Accidents? (2026)

Planning a boat day in Stuart? Learn why relying on your home or auto insurance policies for watercraft liability is a dangerous financial gap.

Read More →

Why Home Insurance Won't Pay Your HOA Storm Assessment (2026)

Received a surprise HOA special assessment after a storm? Discover the critical loss assessment loopholes leaving Stuart homeowners completely exposed in 2026.

Read More →

Does Florida Home Insurance Cover HOA Storm Special Assessments? (2026)

Think your Stuart home or condo insurance automatically covers an HOA special assessment after a hurricane? Discover the loss assessment limits leaving local owners exposed.

Read More →