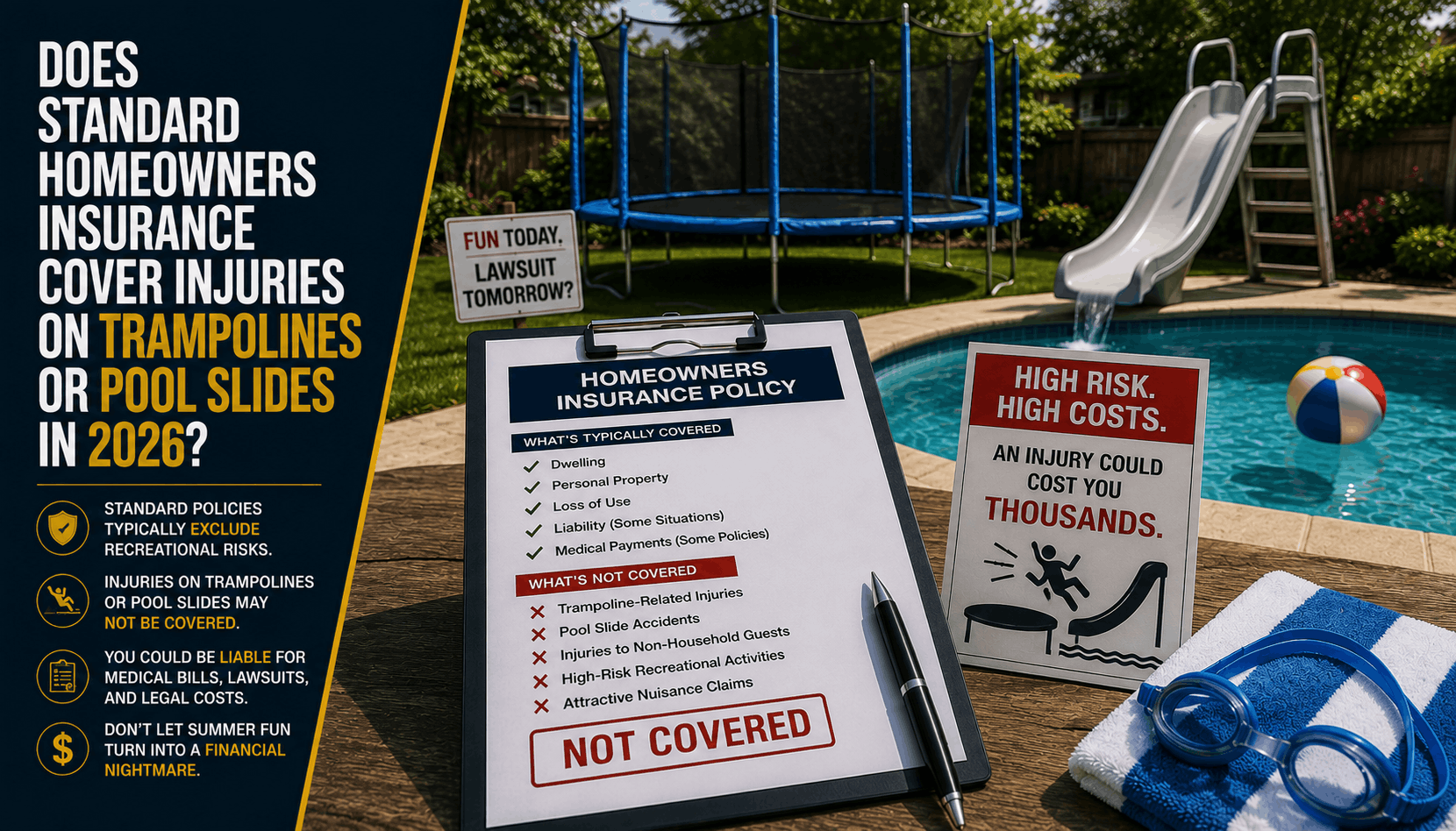

Does Homeowners Insurance Cover Trampolines or Pool Slides? (2026)

The Backyard Liability Trap: Why Your Homeowners Insurance Won't Pay for a Trampoline or Pool Slide Injury This Summer

The Direct Answer

The short answer is a definitive no—your standard homeowners insurance policy will not automatically cover medical bills or liability lawsuits resulting from a trampoline or pool slide injury. In the insurance industry, trampolines and pool slides are classified as attractive nuisances and high-risk liabilities. In 2026, most major Florida home insurance carriers write strict, absolute exclusion clauses directly into their policy contracts for these specific items. If a neighborhood child gets injured on an undeclared trampoline or pool slide in your Stuart backyard, your insurance company has the full legal right to deny your personal liability claim entirely. Even worse, if an inspector discovers you have installed these items without notifying your carrier, your insurance provider can cancel or non-renew your entire homeowners policy with virtually no warning.

As families across Stuart and the Treasure Coast gear up for peak summer fun, setting up a new backyard setup without checking your policy's fine print is a massive financial gamble. Understanding where your land-based liability stops is essential to protecting your home.

Without proper safety features and explicit carrier approval, backyard trampolines can void your home insurance liability coverage.. Fuente: CBC

1. The Underwriting Reality: How Carriers Treat "Attractive Nuisances"

In insurance terms, an attractive nuisance is anything on your property that is highly inviting to children but poses a significant danger of physical harm. Trampolines and pool slides top this list alongside diving boards.

Because of the high frequency of severe spinal, neck, and bone injuries associated with these items, standard home insurance underwriting in 2026 generally falls into three strict categories:

- Absolute Exclusion: The carrier will write your policy but explicitly state in the contract that they will pay $0 for any medical or liability claims involving a trampoline or slide.

- Strict Safety Mandates: The carrier will only cover the risk if you meet exact physical requirements. For a trampoline, this means a professional safety net and a locked, fenced yard. For a pool slide, it means professional installation, no diving boards, and a secured perimeter fence.

- Flat Refusal (The Blacklist): Many premier Florida carriers will simply refuse to write a homeowners policy for your property if a trampoline or pool slide is present, regardless of safety nets or fences.

[ Backyard Installation ]

──\> \[ Fails to Meet Safety Rules OR Unreported to Carrier \]

──\> \[ Neighborhood Child Suffers Injury \]

──\> Standard Policy Clause: Absolute Liability Exclusion

──\> Out-of-Pocket Result: Personal Lawsuits & Potential Policy Cancellation

2. The Pool Slide Loophole: Why Water Safety Isn't Automatically Covered

Many Stuart homeowners believe that because their standard home policy already covers a backyard swimming pool, any accessory—like a slide or a diving board—is automatically grandfathered into that coverage. This is a highly dangerous misconception.

While standard in-ground pools are generally covered under your policy's "Other Structures" (for physical damage) and personal liability sections, slides and diving boards are viewed as completely separate, elevated hazards:

- Diving Boards and Slides: Adding a slide or a diving board dramatically increases the risk of head, neck, and spinal cord injuries from shallow-water impacts. Most carriers require an explicit policy endorsement and a premium surcharge to cover these additions.

- The Unreported Risk Penalty: If you install a pool slide over the weekend without notifying your insurance agent, you have committed what carriers call a material change in risk. If an injury occurs, your insurer can legally deny the liability claim and retroactively cancel your policy back to the date of installation due to a failure to report the hazard.

3. How to Secure Your Backyard and Keep Your Liability Coverage Active

You can still enjoy your backyard this summer, but you must actively align your insurance framework with your physical setup. At Walker Insurance Agency, we advise Stuart homeowners to follow these three protective steps:

- Step 1: Check Your Policy Declaration Pages. Search your current policy documents specifically for "Trampoline Exclusion," "Watercraft Exclusion," or "Other Pool Structures." Know exactly where your current carrier stands.

- Step 2: Install Mandatory Physical Barriers. If your carrier permits a trampoline or pool slide, you must secure the perimeter. This means a minimum six-foot-tall fence with a self-closing, self-latching gate to prevent neighborhood children from wandering onto your property unsupervised.

- Step 3: Secure a High-Limit Personal Umbrella Policy. If you have a pool, slide, or trampoline, a standard $300,000 personal liability limit is simply not enough to cover a major injury lawsuit. Binding a $1 Million or $2 Million Personal Umbrella Policy provides an essential, inexpensive layer of excess liability protection that sits directly on top of your primary home insurance.

Why Working with an Independent Agency is Vital

Relying on direct-to-consumer websites or automated online quotes often hides these critical exclusions in the fine print until it is too late. At Walker Insurance Agency, we provide the expert advocacy needed to audit your backyard setup and preserve your coverage.

The Walker Advantage:

- Carrier Matching: We shop Florida's top independent insurance carriers to find companies that offer affordable, approved liability riders for homes with pools and recreational equipment.

- Comprehensive Risk Audits: We review your property layouts to ensure your fences, gates, and safety nets align perfectly with local Stuart building codes and strict insurance underwriting guidelines.

- Umbrella Integration: We help you structure your primary and umbrella liability limits seamlessly, ensuring you are fully protected against catastrophic personal injury lawsuits.

FAQ

1. Does my homeowners insurance cover injuries to my own children on a backyard trampoline?

Generally, no. Your homeowners policy's "Personal Liability" and "Medical Payments to Others" sections are designed to cover third-party guests (like neighbors or friends) who are injured on your property. Your own family members are expected to be covered under your primary health insurance policy.

2. Can my insurance company drop my coverage if an inspector sees a trampoline in my yard?

Yes. Insurance companies frequently use aerial photography, drone surveys, and random physical drive-by inspections. If an inspector spots an undisclosed trampoline or pool slide on your property, the carrier can issue a cancellation notice for "undisclosed hazards" or "increased hazard risk."

3. What is the difference between "Medical Payments" and "Personal Liability" for backyard injuries?

"Medical Payments" is a small, no-fault coverage limit (typically $1,000 to $5,000) that quickly pays for a guest's minor medical bills (like stitches or X-rays) without needing to prove you were negligent. "Personal Liability" (typically starting at $100,000 to $300,000) kicks in if you are sued for negligence following a severe, life-altering injury on your property.

Protect Your Family and Your Homeowner Equity This Summer

Your backyard should be a place for relaxation and family fun, not a financial trap that leaves your entire estate exposed to devastating lawsuits. Ensuring your physical setup matches your insurance policy is the only way to protect your hard-earned wealth.

Take control of your home protection today. Contact Walker Insurance Agency for a comprehensive backyard risk and policy evaluation. We provide the visibility you need to eliminate hidden exclusions, secure robust liability limits, and keep your summer fun completely safe.

[GET A FREE QUOTE TODAY]

Call our personal lines division at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your property boundaries today.

Related Articles

Does Home or Auto Insurance Cover Boating Accidents? (2026)

Planning a boat day in Stuart? Learn why relying on your home or auto insurance policies for watercraft liability is a dangerous financial gap.

Read More →

Why Home and Auto Insurance Won't Cover Boat Accidents (2026)

Planning a July boat day in Stuart, FL? Discover why relying on your home or auto insurance policies for watercraft liability is a dangerous financial blindspot.

Read More →

Why Home Insurance Won't Pay Your HOA Storm Assessment (2026)

Received a surprise HOA special assessment after a storm? Discover the critical loss assessment loopholes leaving Stuart homeowners completely exposed in 2026.

Read More →