ACV vs. Agreed Value: Classic Car Insurance Guide (2026)

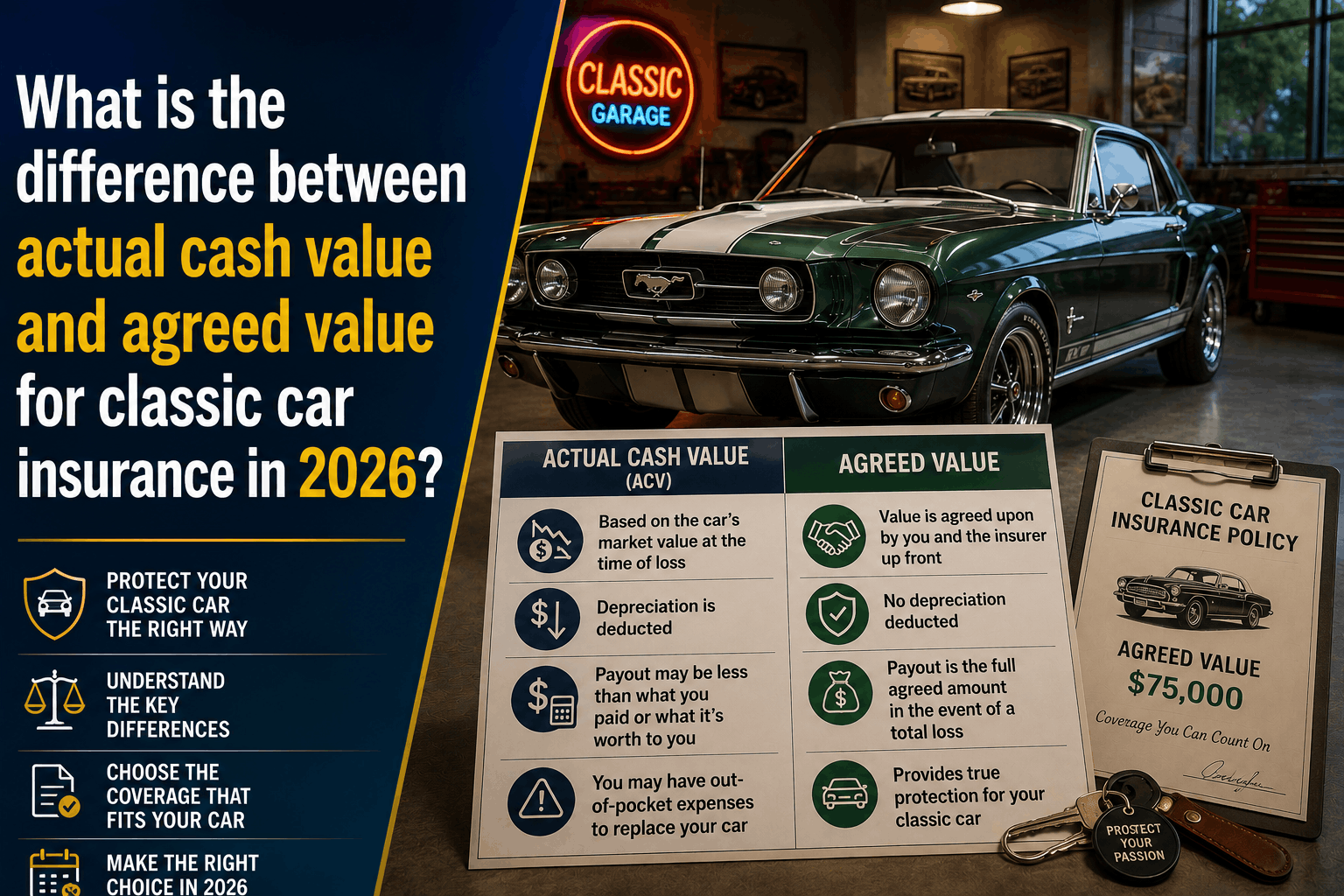

What Is the Difference Between Actual Cash Value and Agreed Value for Classic Car Insurance in 2026?

The Direct Answer: The core difference between Actual Cash Value (ACV) and Agreed Value is how your car's dollar worth is calculated at the exact moment of a total loss. A standard auto policy defaults to Actual Cash Value, which pays out based on the replacement cost of a used car minus ongoing chronological depreciation. Alternatively, a specialty policy utilizes an Agreed Value (or Guaranteed Value) contract, where you and the insurance provider lock in a fixed, un-depreciating payout threshold upfront based on appraisals and enthusiast market guides.

Velocity Restorations+ 1

In 2026, this mathematical gap is wider and more dangerous than ever. Driven by high claims inflation (hitting 8% to 10% due to specialized restoration labor and vintage part scarcity), an ordinary ACV policy will drastically undervalue your vehicle after a crash.

Heritage Insurance

To achieve total visibility over your collector vehicle investment, you must realize that treating an appreciating or restored asset like a depreciating daily commuter car is a shortcut to severe financial loss.

1. The Breakdown: How Each Payout Settles Claims

To understand how these structures operate under pressure, look at how a claims adjuster evaluates a total loss event for an enthusiast vehicle under each framework:

Actual Cash Value (ACV) — The Depreciation Trap

Standard insurance policies are built for ordinary commuter cars that lose value every single month. When you file a claim under an ACV policy, the carrier's automated software calculates your payout using basic market databases. It looks strictly at your vehicle's make, model, age, and mileage, subtracting heavy deductions for wear and tear.

The software has no built-in mechanism to recognize a flawless frame-off restoration, rare matching-numbers factory options, or the thousands of dollars you spent on custom upgrades. It simply views your prized asset as a basic "old used car."

Agreed Value — The Collector’s Gold Standard

With an Agreed Value policy, the post-loss negotiation is completely removed from the timeline. Before the contract is ever bound, you present photos, receipts, and professional appraisals to a specialized collector underwriter. Together, you lock in a fixed sum insured. If the vehicle is written off or stolen, the insurer guarantees to write a check for that exact pre-determined dollar amount. Depreciation is legally banned from the equation.

Velocity Restorations+ 2

2. The 2026 Market Catalyst: Why It Matters More This Year

The collector landscape is experiencing sharp structural shifts. Data from the 2026 Hagerty Bull Market List shows that while mainstream classic values have stabilized, modern enthusiast cars from the 1990s and 2000s—such as the C6 Chevrolet Corvette Z06, the E60 BMW M5, and the R33/R34 Nissan Skyline GT-R—are experiencing intense demand and rising insured valuations.

CarPro

Simultaneously, macro-economic factors have turned minor fender benders into automated "total loss" triggers:

[8%-10% Specialty Claims Inflation] + [Scarcity of OEM Vintage Panels]

= Hyper-Inflated Repair Estimates ───> Exceeds Standard ACV Limits ───> Forced Write-Off

Because specialized body shop labor and raw material costs (like vintage trim polymers and aluminum) are at record highs, a minor structural dent can easily generate a repair bill exceeding 70% of an undervalued ACV calculation. Under a standard policy, the insurer will automatically declare the car a total loss, take your vehicle to a salvage auction, and leave you with a heavily depreciated, bottom-dollar settlement.

3. Side-by-Side Comparison: ACV vs. Agreed Value vs. Stated Value

Many drivers fall for a deceptive third option called Stated Value. To protect your assets, you must understand exactly how these three tiers contrast:

| Feature | Actual Cash Value (ACV) | Stated Value (The Loophole) | Agreed Value / Guaranteed Value |

|---|---|---|---|

| How Value is Formed | Calculated after the crash by automated adjuster software. | You state a value upfront to adjust your monthly premium. | Mutually locked in advance using appraisals and market data. |

| Depreciation Applied? | Yes. Heavy age and mileage deductions are standard. | Yes. It does not guarantee a fixed payout line. | No. Completely exempt from chronological depreciation. |

| The Legal Payout Catch | Pays what the insurer decides a used car is worth today. | Contractually pays the lesser of your stated amount or ACV. | Pays 100% of the written amount in a total loss. |

| Best Suited For | Everyday daily commuters and modern family SUVs. | Commercial haulers or highly modified utility trucks. | Classic, custom, vintage, and modern enthusiast cars. |

How to Safely Build a Collector Shield

If your vintage vehicle or modern classic is currently bundled on the exact same personal auto insurance policy as your daily commuter vehicle, your investment is exposed to the ACV trap.

At Walker Insurance Agency, we specialize in unbundling classic profiles and transitioning them into elite standalone collector programs:

Step 1: Compile Comprehensive Restoration Receipts and High-Resolution Photos

Step 2: Obtain a Certified Enthusiast Appraisal

Step 3: Bind an "Agreed Value" Contract with a Specialty Collector Underwriter

=============================================================================

= Total Valuation Certainty + Freedom from the 2026 Claims Inflation Squeeze

By establishing a true Agreed Value Specialty Policy (through preferred specialist markets like Hagerty or Progressive Classic), you insulate your wealth. Furthermore, because underwriters know these vehicles are stored in secure, locked garages and driven strictly for pleasure rather than a daily highway rush-hour commute, these policies are frequently 30% to 50% cheaper than standard, daily-driver auto lines.

Why Working with an Independent Agency is Vital

Attempting to insure a piece of automotive history through a generic online quoting portal is incredibly high-risk. Automated algorithms do not read restoration build sheets or understand collector market shifts. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to defend your garage.

The Walker Advantage:

- Real-Time Price Guide Syncing: We evaluate your classic's condition against current auction and private-sale data to make sure your Agreed Value limit perfectly reflects its true market worth.

- Flexible Mileage Tiering: We help you select customized limited-use mileage tiers that keep your weekend car club cruises protected without triggering regular-use policy exclusions.

- Comprehensive Asset Bundling: We align your specialty car lines with your home and personal umbrella defenses, keeping your fixed cost of living optimized across Stuart.

FAQ

1. Does an Agreed Value classic policy restrict my choice of repair shops? No. While standard ACV policies utilize corporate direct-repair networks to cut corners with aftermarket components, top-tier Agreed Value policies explicitly guarantee your right to take your vehicle to any high-end restoration facility, specialty hot-rod fabricator, or marque expert of your choice.

2. What are the strict eligibility requirements for an Agreed Value policy in 2026? To qualify for a specialty collector policy, the vehicle must generally be stored in a fully enclosed, locked garage or secure residential structure. Additionally, it cannot be used as your primary daily transportation; every licensed driver in your household must have an active, separate daily-use vehicle insured on a standard personal policy.

3. What happens if the market value of my classic increases significantly mid-policy? If a trending vehicle type experiences a massive surge in market valuation during your policy term, your Agreed Value does not automatically climb with it. To prevent being underinsured, you should work with an independent agent to file a mid-term value adjustment endorsement, backing the increase with updated market sales or appraisal data to update your contract floor.

Insure Your Passion with Absolute Certainty

Your collector vehicle is more than basic transportation—it's an appreciating asset, a historical statement, and a significant personal investment. Leaving its financial protection tied to an ordinary used-car policy is an administrative gamble that will cost you tens of thousands of dollars the moment an accident occurs.

Lock in your guaranteed valuation check today. Contact Walker Insurance Agency for a comprehensive 2026 Agreed Value Portfolio Review. We provide the visibility you need to eliminate depreciation loopholes, bypass corporate claims inflation, and preserve your automotive legacy safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your investment today.

Related Articles

Does Collision Insurance Cover Hail & Tree Damage in 2026?

Did hail or a falling tree branch damage your car? Learn why collision auto insurance won't pay for storm damage and how comprehensive coverage protects you.

Read More →

Why Collision Insurance Pays $0 for Non-Crash Summer Damage (2026)

Did a tree branch, hail storm, or flying road debris hit your car this summer? Discover why collision auto insurance pays $0 and how comprehensive coverage protects you.

Read More →

Florida Minimum Auto Insurance Coverage Illusion (2026)

Driving with state-minimum auto insurance in Florida? Learn why carrying only PIP and PDL leaves your health and personal savings vulnerable after a crash.

Read More →