Buying Homeowners Insurance During a Tropical Storm in Florida (2026 Rules)

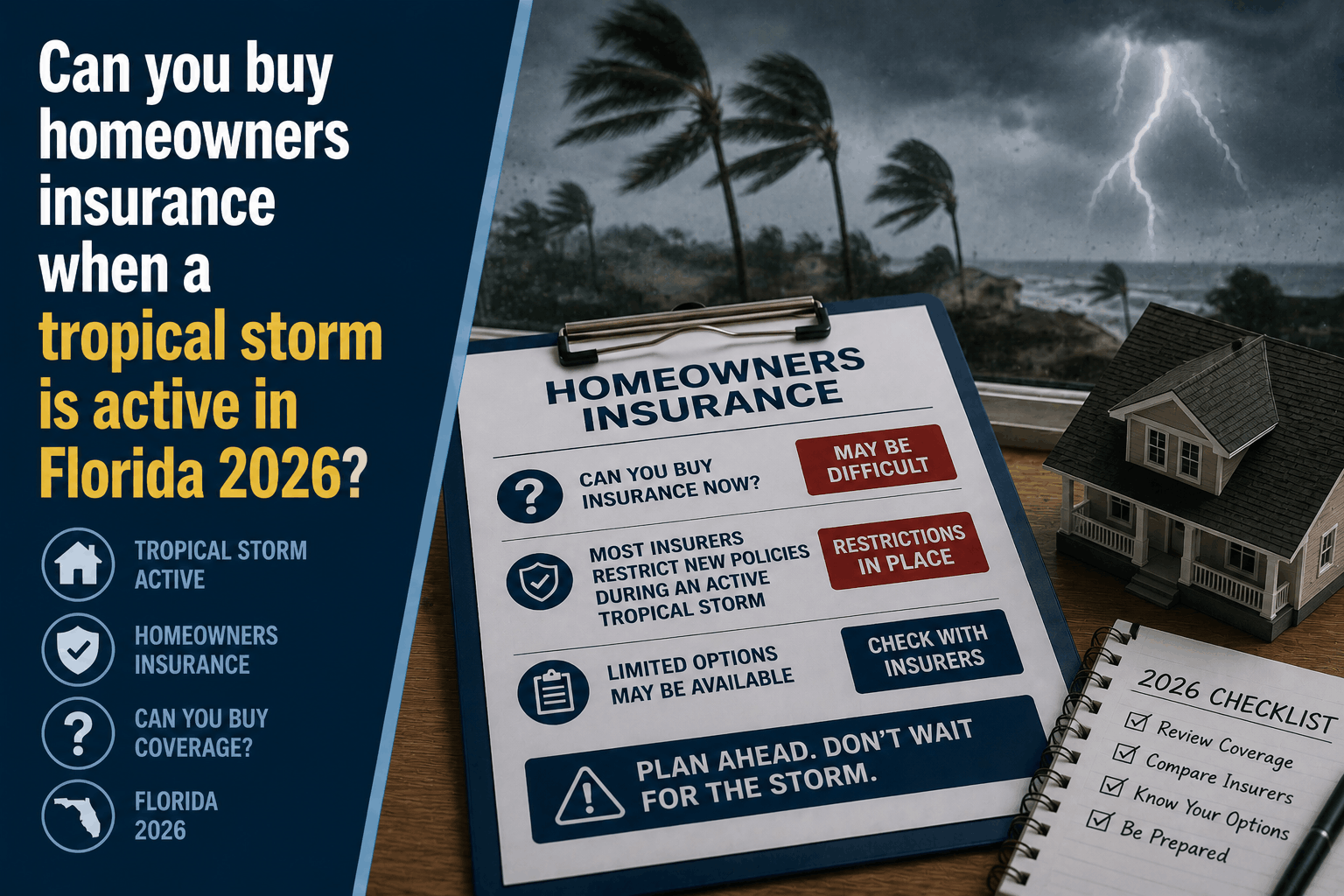

Can You Buy Homeowners Insurance When a Tropical Storm Is Active in Florida?

The Direct Answer: No, you generally cannot buy, alter, or bind a new homeowners insurance policy in Florida once a tropical storm or hurricane becomes active and threatens the state. The moment the National Hurricane Center (NHC) issues a formal tropical storm or hurricane watch or warning for any portion of Florida, the Florida Office of Insurance Regulation (OIR) permits insurance carriers to activate a binding moratorium.

During a moratorium, insurance company software automatically locks, legally prohibiting agents from issuing new coverage or increasing policy limits until the storm completely passes and the warnings are officially lifted.

To achieve total visibility over your home purchase or policy renewal, you must realize that waiting until a storm enters the Gulf or Atlantic means you are already too late. The insurance gate shuts down days before the first raindrops ever hit your roof.

1. How the 2026 Binding Moratorium Works

An insurance binding moratorium is an underwriting firewall. It prevents homeowners from buying a "last-minute" safety net only when damage is completely imminent.

- The Trigger: The absolute second the NHC maps a watch or warning box over any county in Florida, carriers activate their internal moratorium protocols. Under state rule updates, insurers must notify the OIR if they plan a temporary suspension of new business, but storm moratoriums are grandfathered into standard policy contracts.

- The Geographic Box: Moratoriums are rarely limited to the exact city in the storm's cone. Because Florida weather is highly unpredictable, most private carriers lock down bindings statewide or across vast regional zones (e.g., the entire Gulf Coast or Central Florida) rather than just the target county.

- The Duration: The lockdown remains firmly in place through the duration of the weather event. It typically terminates 72 hours after the final watch or warning is officially lifted by the authorities, allowing adjusters time to assess regional structural damages before new risks are taken on.

2. The Real Danger: Real Estate Closing Meltdowns

The biggest victims of a tropical storm moratorium aren't people looking to switch carriers—it is homebuyers with pending real estate transactions.

If you are scheduled to close on a home in Stuart, Destin, or Miami, and a tropical storm triggers a moratorium before your agent officially binds your insurance contract, your closing will stall completely.

[Loan Approved] ──> [Storm Forms] ──> [Moratorium Triggers] ──> [Insurance Locked] ──> [Closing Delayed]

The Lender Mandate: Federal regulations strictly prohibit mortgage companies from funding a loan without active, verified hazard insurance. If the insurance is frozen by a moratorium, the bank will pull your funding package back from the table, forcing a mandatory delay that can cause your purchase contract to expire or blow past your locked interest rate.

3. The One Exception to the Rule

There is only one legal workaround to a live storm moratorium in Florida, and it applies strictly to buyers using a mortgage:

- The Loan Nexus Exception: If a policy has already been fully quoted and processed through underwriting, and the binding date is scheduled to match a formal real estate closing, some traditional carriers—along with Citizens Property Insurance Corp. (the state-backed carrier)—will allow the policy to bind only if the mortgage lender requires it to finalize the transfer of the title on that exact day.

- The Catch: You cannot use this exception to shop around for a cheaper rate at the last minute or add missing coverage lines. The paperwork must have been completely finalized before the NHC issued its storm warnings.

4. The 30-Day Flood Insurance Trap

Even if you manage to secure a standard homeowners insurance policy right before a storm forms, you are completely unprotected against rising water.

- The Core Exclusion: Standard homeowners insurance policies never cover flood damage or storm surge.

Local Life Homes - The 30-Day Clock: Private flood policies and federal policies written through the National Flood Insurance Program (NFIP) carry a strict 30-day waiting period before the coverage becomes active. If you purchase a flood policy while a tropical storm is tracking across the Caribbean, the storm will hit your property weeks before your flood shield ever goes live.

Orlando & Tampa Property Management | True North Managed

Why Working with an Independent Agency is Vital

In Florida's highly competitive market—where 20 brand-new property insurance companies have entered the state following successful tort reforms—timing your policy placement perfectly is everything. At Walker Insurance Agency, we monitor the weather radar and carrier underwriting desks simultaneously to give you the visibility required to bypass closing delays.

The Walker Advantage:

- Pre-Cone Binding Execution: We track tropical disturbances long before they receive a name. If a system shows a 40% chance of development, we proactively reach out to clients with pending closings to bind their coverage early.

- Citizens Depopulation Management: If you are transitioning from Citizens to a private market carrier, we time the swap outside of the seasonal storm windows to prevent coverage gaps.

- Multi-Line Shielding: We ensure your homeowners, wind-mitigation credits, and private flood timelines are perfectly aligned, securing maximum protection before a storm ever enters your hemisphere.

FAQ

1. Can I add comprehensive wind coverage to my policy while a tropical storm is active? No. A moratorium blocks all new business and endorsements that increase a carrier's exposure. You cannot lower your deductible, add optional windstorm endorsements, or increase your Coverage A limits until the storm has cleared the state.

sigma programs

2. Does a tropical storm activate my hurricane deductible? No. Under Florida law, your high-percentage hurricane deductible (typically 2% to 5% of your dwelling value) only triggers when the National Hurricane Center officially issues a hurricane warning for any part of Florida. If the storm remains classified strictly as a tropical storm, your standard, lower "All Other Perils" (AOP) deductible applies to the wind damage.

Chapman Insurance Group

3. What happens if my home insurance expires during a storm moratorium? If your policy is already active and set to renew on a day a storm hits, your current carrier cannot legally drop you. Under OIR consumer protection mandates, insurance companies are completely barred from canceling or non-renewing policies during a state-declared emergency window. Your coverage will automatically extend until the danger passes.

Don't Risk Your Home on a Weather Forecast

The 2026 hurricane season is active, and waiting until a storm cone is pointing at your county to secure property protection is a catastrophic financial mistake. Real peace of mind requires establishing your baseline coverage long before the storm sirens sound.

Secure your home coverage today. Contact Walker Insurance Agency for an immediate property audit. We provide the visibility you need to lock in competitive rates with Florida's newest carriers, finalize your real estate closings safely, and shield your assets from seasonal storm traps in Stuart.

[GET A FREE QUOTE TODAY] Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us protect your property today.

Related Articles

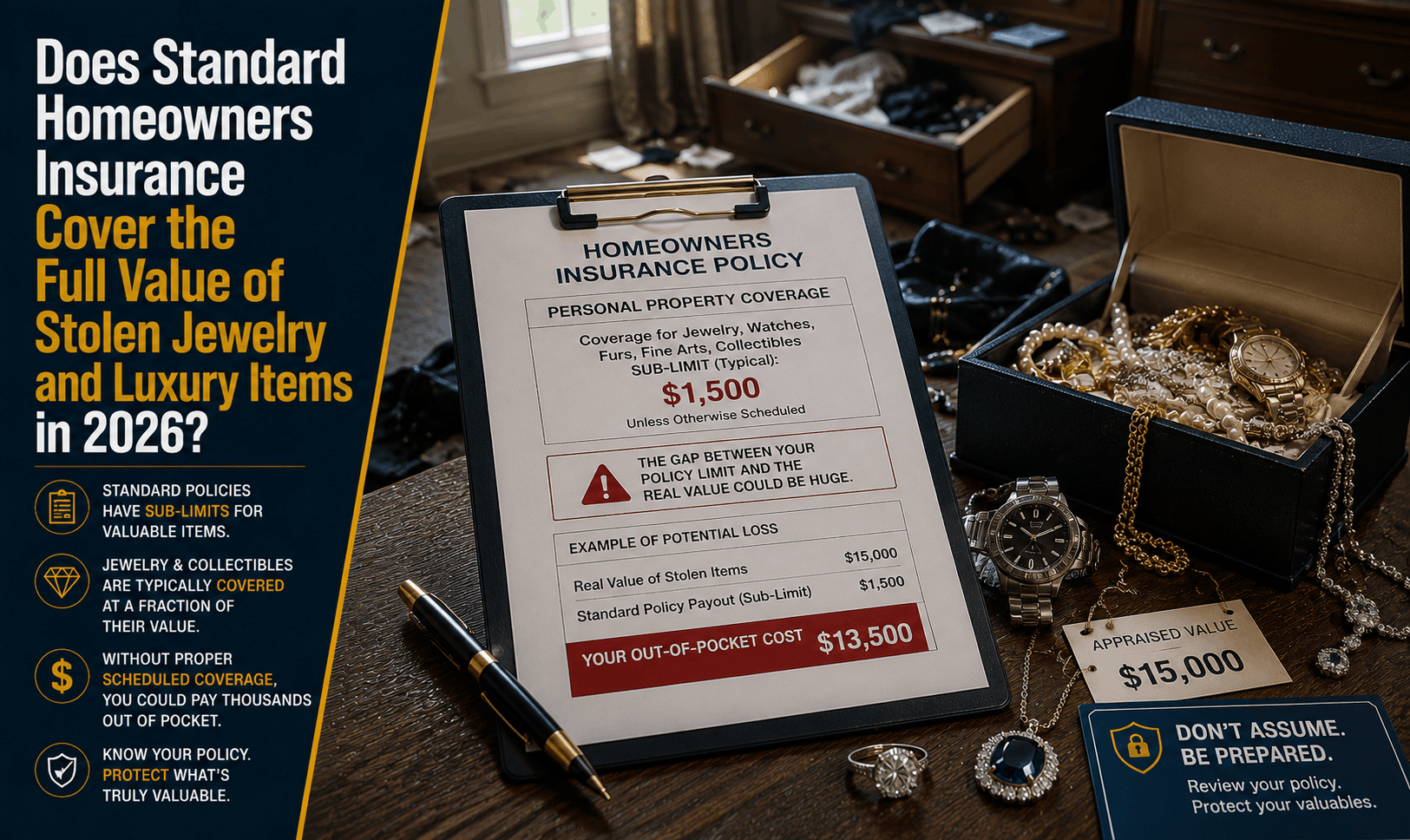

Does Homeowners Insurance Cover Stolen Jewelry & Luxury Goods? (2026)

Had luxury watches or jewelry stolen? Learn why standard homeowners insurance caps theft payouts at $1,500 and how to fully insure your high-value items.

Read More →

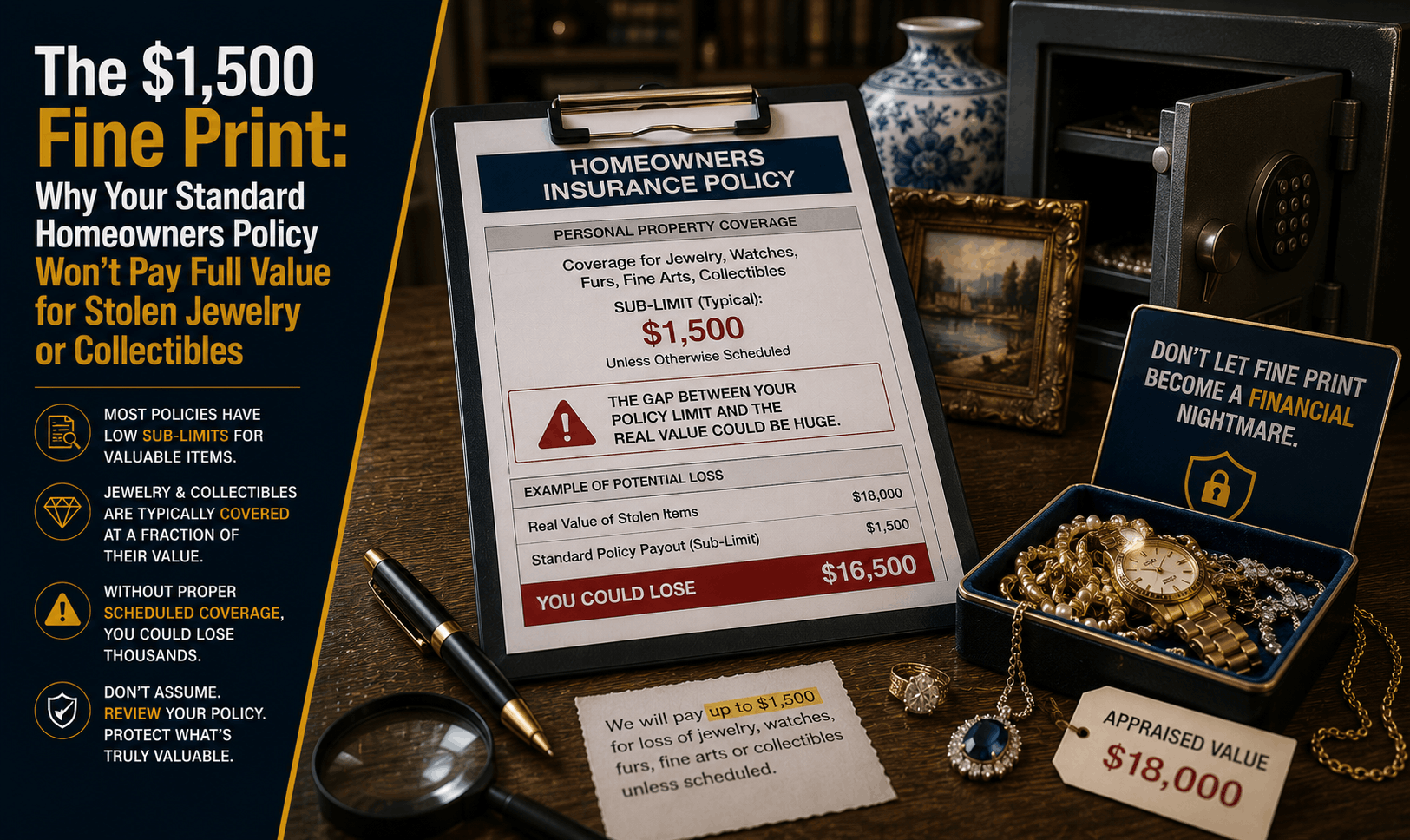

Does Home Insurance Cover Stolen Jewelry & Collectibles? (2026)

Had jewelry or valuables stolen? Discover why standard homeowners insurance limits theft payouts to $1,500 and how to fully insure your high-value items.

Read More →

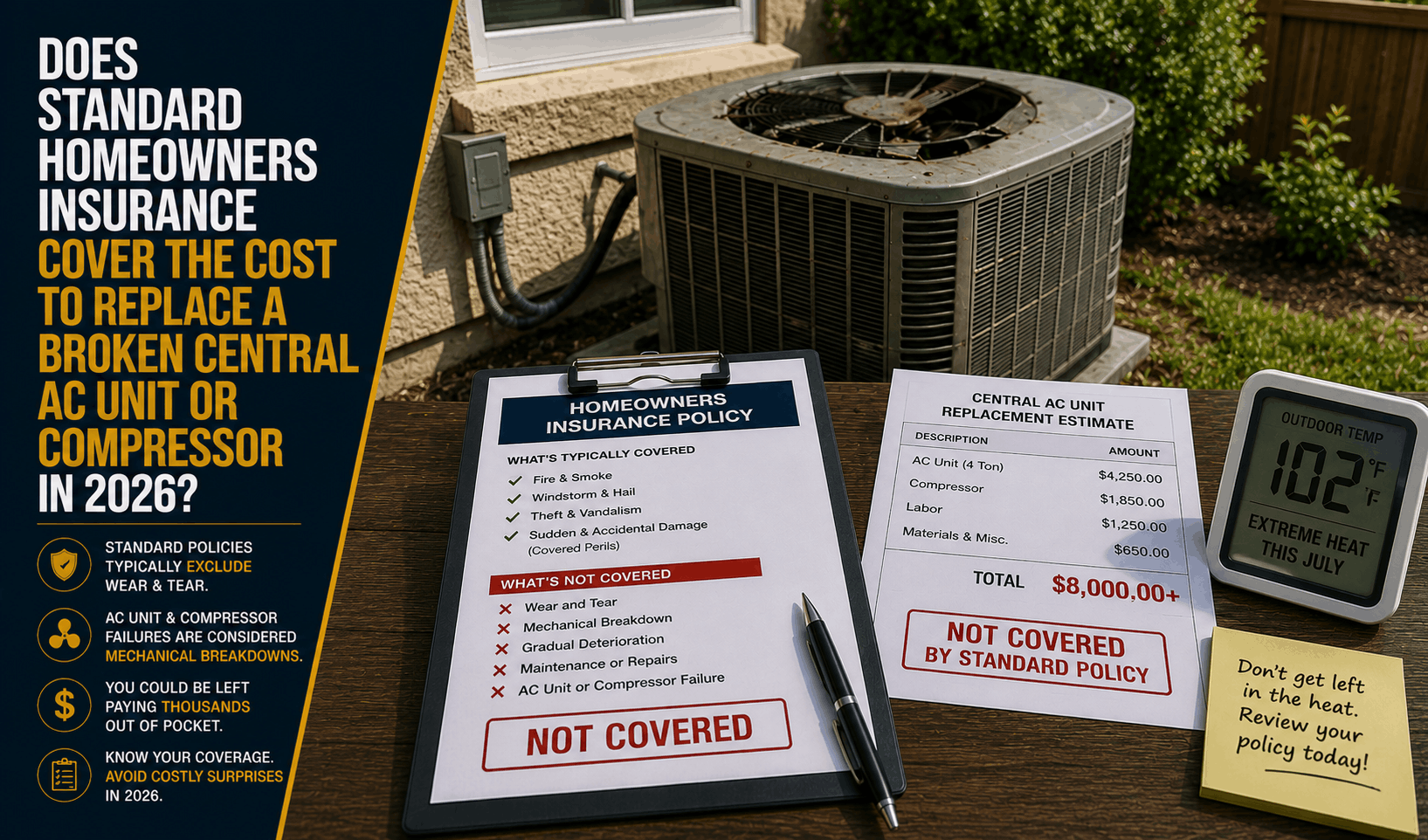

Does Homeowners Insurance Cover Broken AC Units? (2026)

AC broken in the summer heat? Learn why standard homeowners insurance won't pay to replace a broken central AC unit or compressor due to mechanical wear.

Read More →