Does Auto Insurance Cover Unlisted Drivers in an Accident? (2026 Rules)

Does Auto Insurance Cover Unlisted Drivers in an Accident in 2026?

The Direct Answer: Generally, yes—auto insurance follows the vehicle rather than the individual driver. If you lend your car keys to a licensed friend, neighbor, or out-of-town relative, your insurance acts as the primary coverage to pay for physical and medical damages up to your policy limits. In the insurance industry, this baseline protection is known as Permissive Use.

However, in 2026, as major auto carriers face massive claims inflation and aggressively tighten their policy loopholes, this safety net comes with critical, non-negotiable legal catches.

To achieve total visibility over your financial protection, you must realize that if an unlisted driver violates specific contract parameters—such as being an undisclosed permanent resident of your household, operating with a suspended license, or driving your car for commercial app work—your insurance company has the full legal right to trigger an immediate claims denial, leaving you personally liable for the bills.

1. The Operational Baseline: Permissive Use

Under a standard comprehensive auto policy, an unlisted operator is contractually covered if they fit the definition of an occasional, permissive driver.

- Primary Coverage Status: If you give explicit or implied permission to a licensed friend to borrow your vehicle to run an errand, and they cause an accident, your policy pays first.

- The Secondary Backup: If the total medical and property damage exceeds your personal policy limits, the unlisted driver’s own auto insurance policy (if they own a vehicle) can be tapped as secondary coverage to bridge the remaining financial gap.

2. The 3 Legal Loopholes Triggering Auto Denials This Year

Because car insurance companies are looking for any mechanism to limit risk exposure, claims adjusters utilize advanced data-matching software to scrutinize accidents involving unlisted operators. If any of the following parameters are breached, the permissive use framework collapses entirely:

\[Unlisted Driver Accident\]

│

┌───────────────────────┼───────────────────────┐

▼ ▼ ▼

[Undisclosed Resident] [The Frequency Cap] [The License Rule]

Lives under your roof Uses vehicle regularly License is expired,

but not named. (>12 times/year). suspended, or revoked.

│ │ │

▼ ▼ ▼

DENIED DENIED DENIED

Excluded Parameter 1: The Undisclosed Household Resident

This is the single most common reason unlisted driver claims fail. Insurance contracts mandate that every licensed driver living under your permanent roof must be explicitly named on your policy. This includes spouses, roommates, children with fresh permits, or relatives staying with you long-term.

Insurers assume household members have regular access to the keys. If an unlisted roommate crashes your car, the carrier will view it as a failure to disclose household risk and will deny the claim on the grounds of material misrepresentation.

Excluded Parameter 2: The "Regular Use" Frequency Cap

Permissive use is legally reserved for unpredictable or occasional borrowing. Across modern policies, if an unlisted driver uses your vehicle consistently—such as a babysitter using it twice a week or a neighbor borrowing it more than 12 times in a single calendar year—they cross the line into a regular operator. If trip number 13 ends in a collision, the adjuster will deny the claim because the driver should have been formally added to the policy.

Excluded Parameter 3: The Valid License Mandate

Giving verbal permission to someone does not override statutory law. If you hand your car keys to a friend whose license is expired, suspended, or revoked, you have breached your primary policy terms. The insurance company will legally void coverage for the incident, and you can face secondary legal charges for permitting an unauthorized person to drive.

3. The Dangerous Financial Trap: Step-Down Limits

Even if your carrier agrees to pay an unlisted driver claim under permissive use, you could still face extraordinary out-of-pocket costs due to a mechanism called Step-Down Liability Limits:

The Rule: Many non-standard and preferred policies state that when an unlisted permissive driver is behind the wheel, your custom liability limits (e.g., $100,000/$300,000) automatically step down to the absolute state-mandated financial minimum responsibility limits.

If your policy limits drop to the bare state legal minimums while your friend causes a multi-car highway accident, your carrier will pay out to the lower threshold and stop completely. Any remaining medical collections or vehicle structural bills will fall directly on your shoulders, putting your personal assets, savings, and future earnings at risk.

Why Working with an Independent Agency is Vital

In a volatile market where major carriers are rolling out significant price adjustments (including State Farm's 10.1% cut and Progressive's 8% drop), managing your household risk through an automated app is a massive gamble. At Walker Insurance Agency, we provide the data-driven visibility you need to map out your household protection safely.

The Walker Advantage:

- Step-Down Audits: We review your policy fine print to identify hidden step-down limits or absolute resident exclusions before you ever lend your car keys.

- Driver Tier Synchronization: We help you properly structure your named, deferred, and excluded driver lists to prevent automated resident denials in Stuart.

- Umbrella Safety Integration: We design Personal Umbrella Policies (PUP) that sit seamlessly on top of your auto lines, expanding your liability shield to $1 million or more to protect your investments from catastrophic, multi-driver lawsuits.

FAQ

1. What happens if someone takes my car without permission and crashes it?

This is classified as "non-permissive use" or theft. If an individual takes your vehicle without your consent, your personal liability coverage will not pay for the third-party damages because you did not authorize the operation. Your own vehicle's physical repairs will be covered strictly through your policy's Collision or Comprehensive coverage, provided you file an official police report against the driver.

2. Does car insurance cover a driver using my vehicle for rideshare or delivery work?

Absolutely not. Personal auto insurance policies carry strict commercial and business-use exclusions. If an unlisted friend borrows your vehicle to deliver food or drive for a rideshare app, your policy is completely void during that active commercial window.

3. If I have a clean driving record, will an unlisted driver's accident ruin my insurance history?

Yes. Because insurance follows the vehicle, the claim is filed against your policy record. An at-fault accident caused by a permissive driver will appear on your insurance history report (CLUE report), which will likely result in a significant premium increase or a policy non-renewal at your next term.

Protect Your Financial Health Before You Hand Over Your Keys

Handing over your vehicle keys should never be done blindly. In the current insurance climate, a minor administrative oversight regarding an unlisted driver can instantly transform a casual favor into a devastating financial liability.

Verify your permissive use protections today. Contact Walker Insurance Agency for a comprehensive 2026 Policy Review. We provide the visibility you need to unearth hidden step-down limits, secure your household driver listings, and shield your assets safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your drive today.

Related Articles

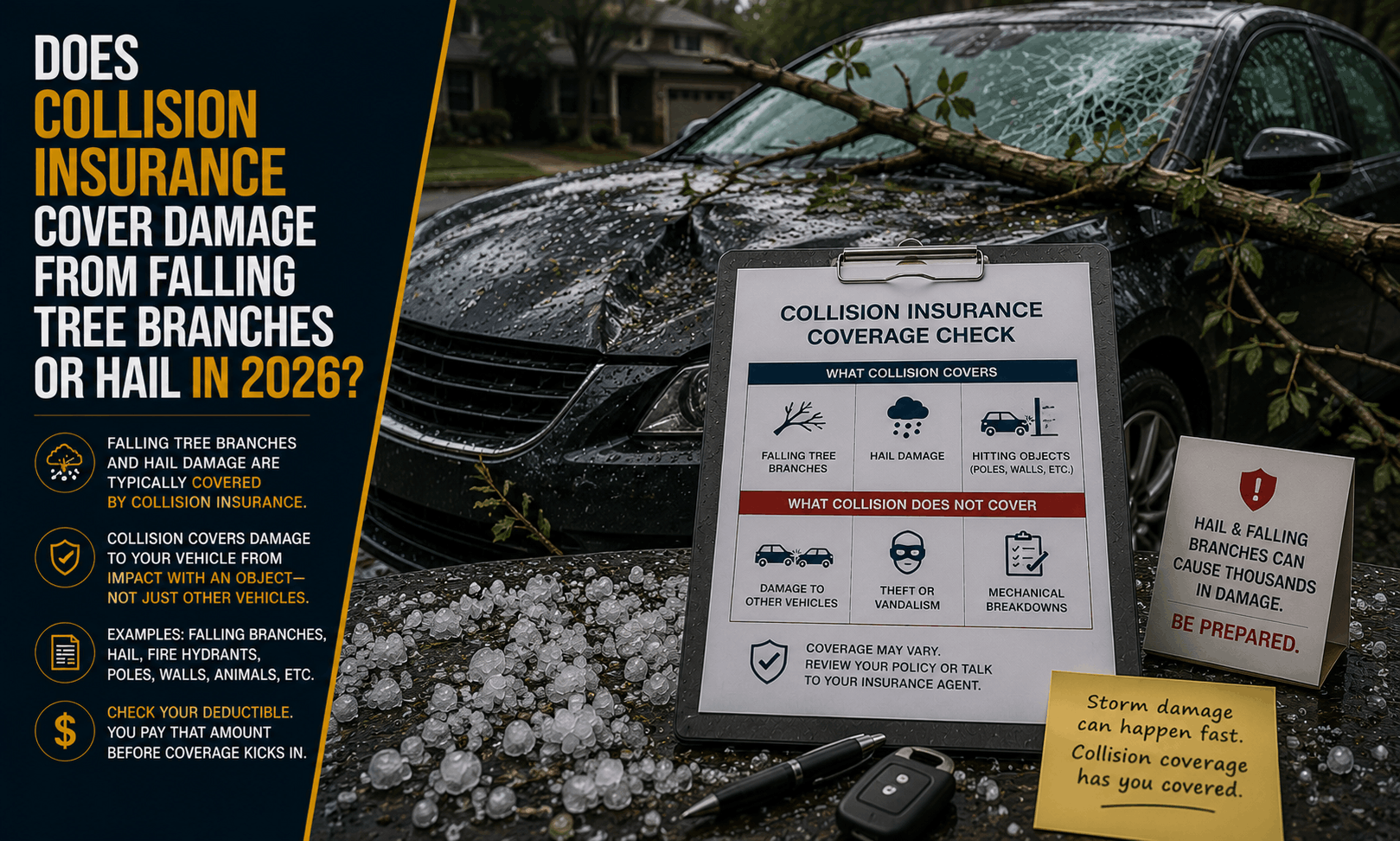

Does Collision Insurance Cover Hail & Tree Damage in 2026?

Did hail or a falling tree branch damage your car? Learn why collision auto insurance won't pay for storm damage and how comprehensive coverage protects you.

Read More →

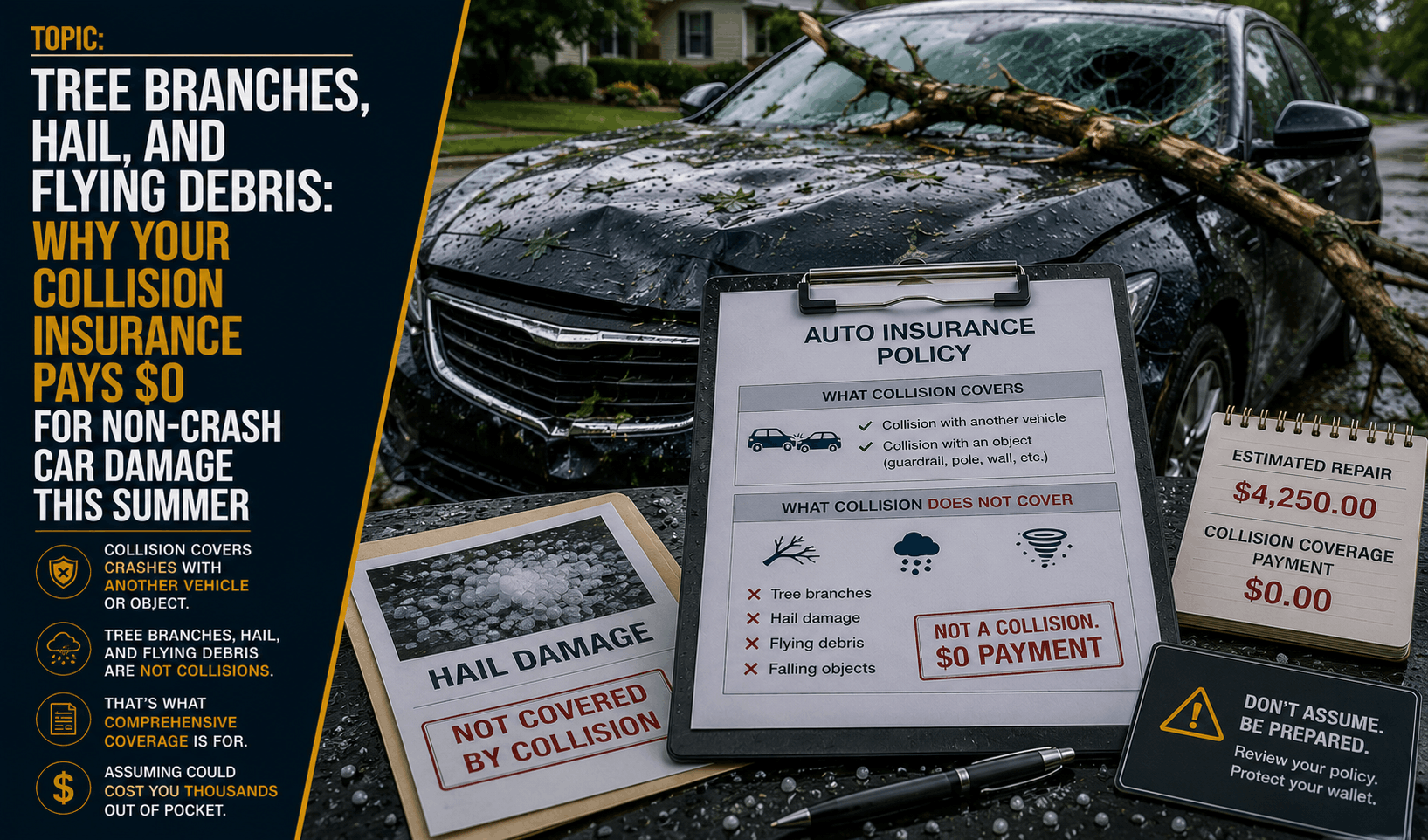

Why Collision Insurance Pays $0 for Non-Crash Summer Damage (2026)

Did a tree branch, hail storm, or flying road debris hit your car this summer? Discover why collision auto insurance pays $0 and how comprehensive coverage protects you.

Read More →

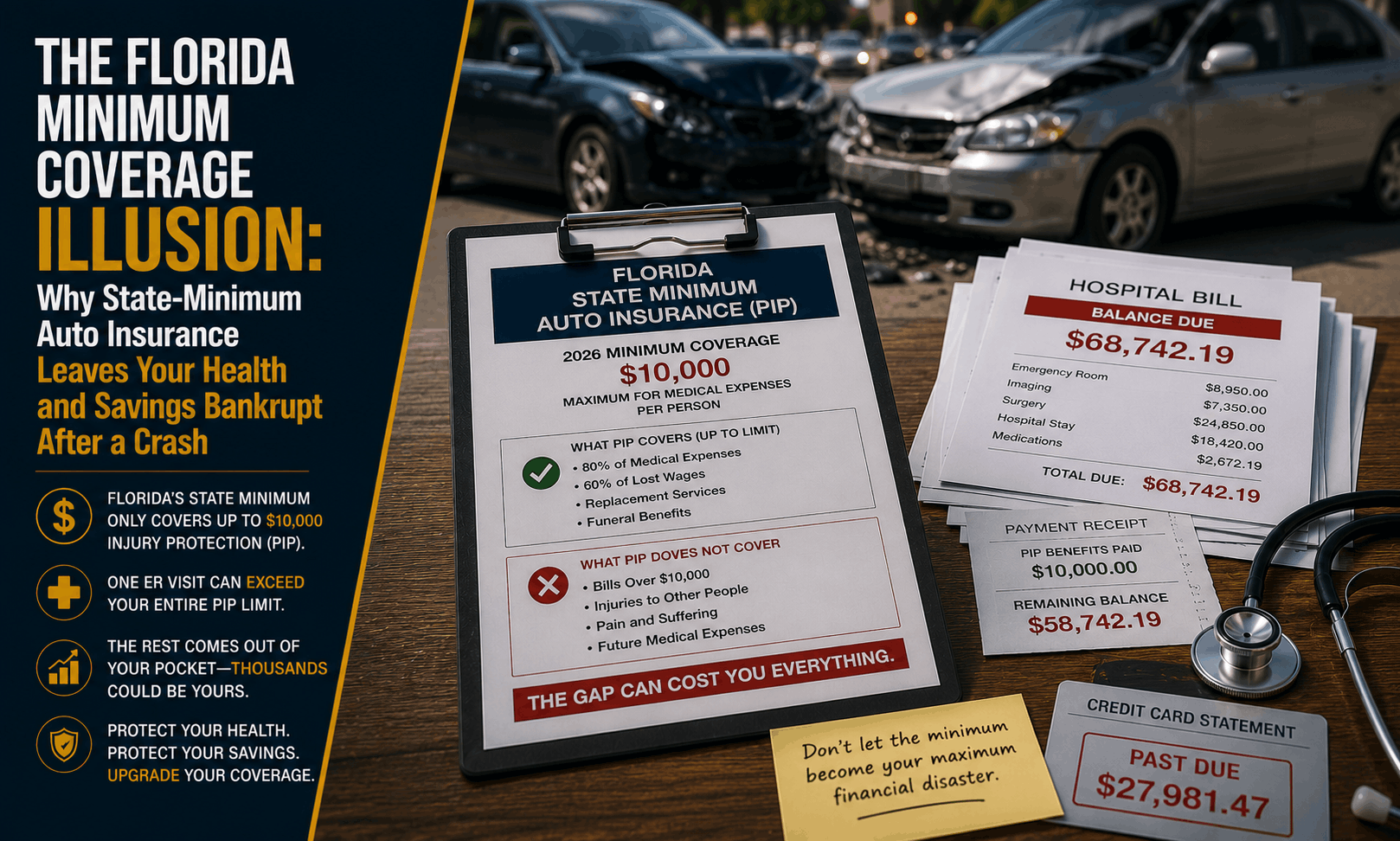

Florida Minimum Auto Insurance Coverage Illusion (2026)

Driving with state-minimum auto insurance in Florida? Learn why carrying only PIP and PDL leaves your health and personal savings vulnerable after a crash.

Read More →