Does Florida Home Insurance Cover Roof Replacement Cost in 2026?

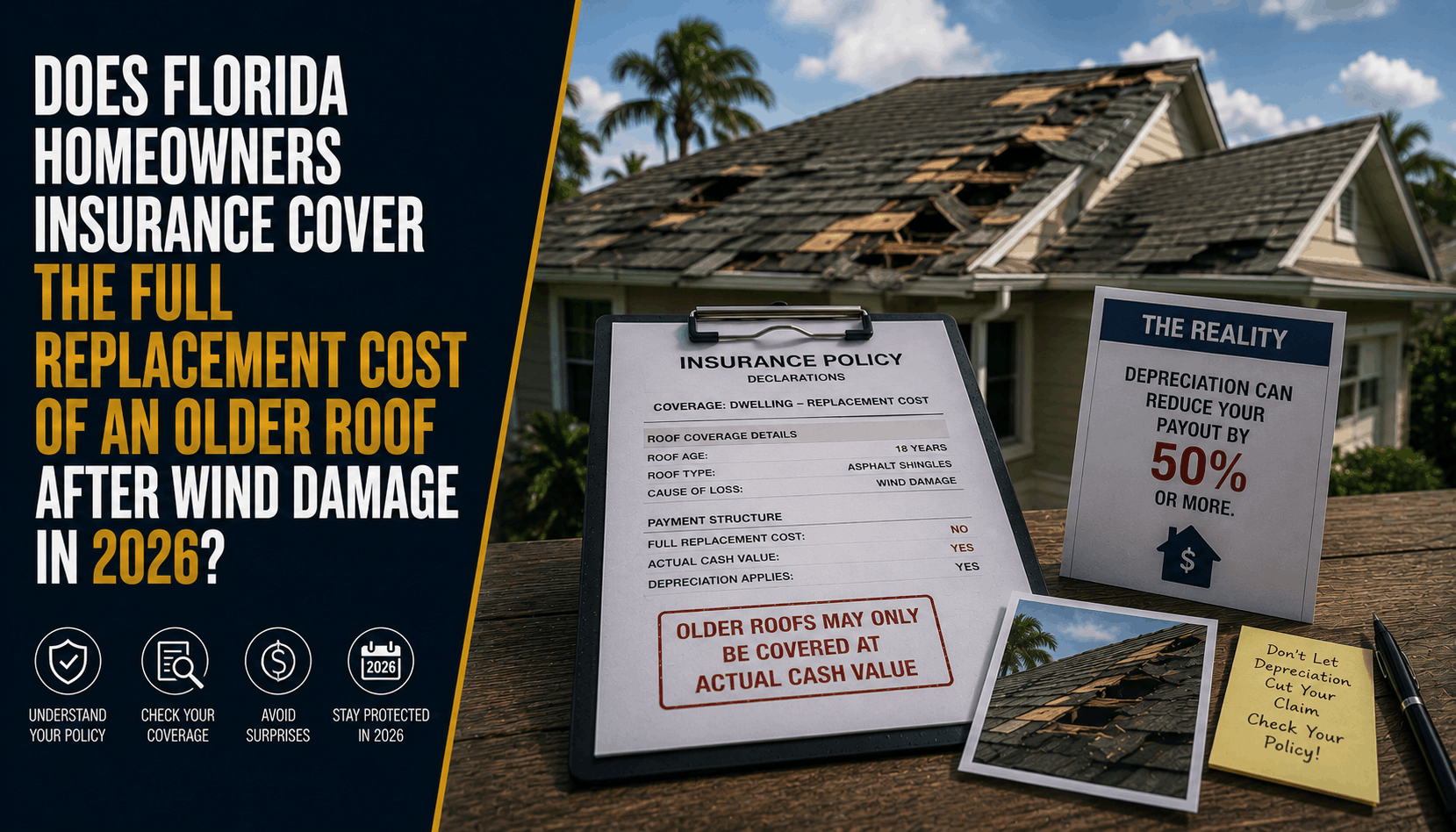

Does Florida Homeowners Insurance Cover the Full Replacement Cost of an Older Roof After Wind Damage in 2026?

The Direct Answer

The short answer is no, not automatically anymore. In 2026, whether your Florida property insurance covers the full replacement cost of an older roof after wind damage depends entirely on your specific policy endorsements, not just the "Replacement Cost Value" label on your front page. Following sweeping rule changes by the Federal Housing Finance Agency (FHFA), major mortgage backers like Fannie Mae and Freddie Mac now officially permit private insurance carriers to offer Actual Cash Value (ACV) roof endorsements. This means that if a tropical storm or severe wind event rips shingles or tiles off a roof that is older than 10 to 15 years, your insurance carrier is legally allowed to pay you a highly depreciated payout based strictly on the roof's age, leaving you to pay tens of thousands of dollars out of pocket to complete the build.

For years, Sunshine State homeowners operated under the assumption that a storm-damaged roof meant a brand-new roof funded entirely by their insurer, minus a standard deductible. In 2026, the stabilizing but highly restrictive Florida property market has completely flipped that script. Private carriers are aggressively utilizing "Roof Surface Payment Schedules" to protect their capital reserves from windstorm exposure, shifting the financial maintenance of aging roofs back onto property owners in Stuart and across the Treasure Coast.

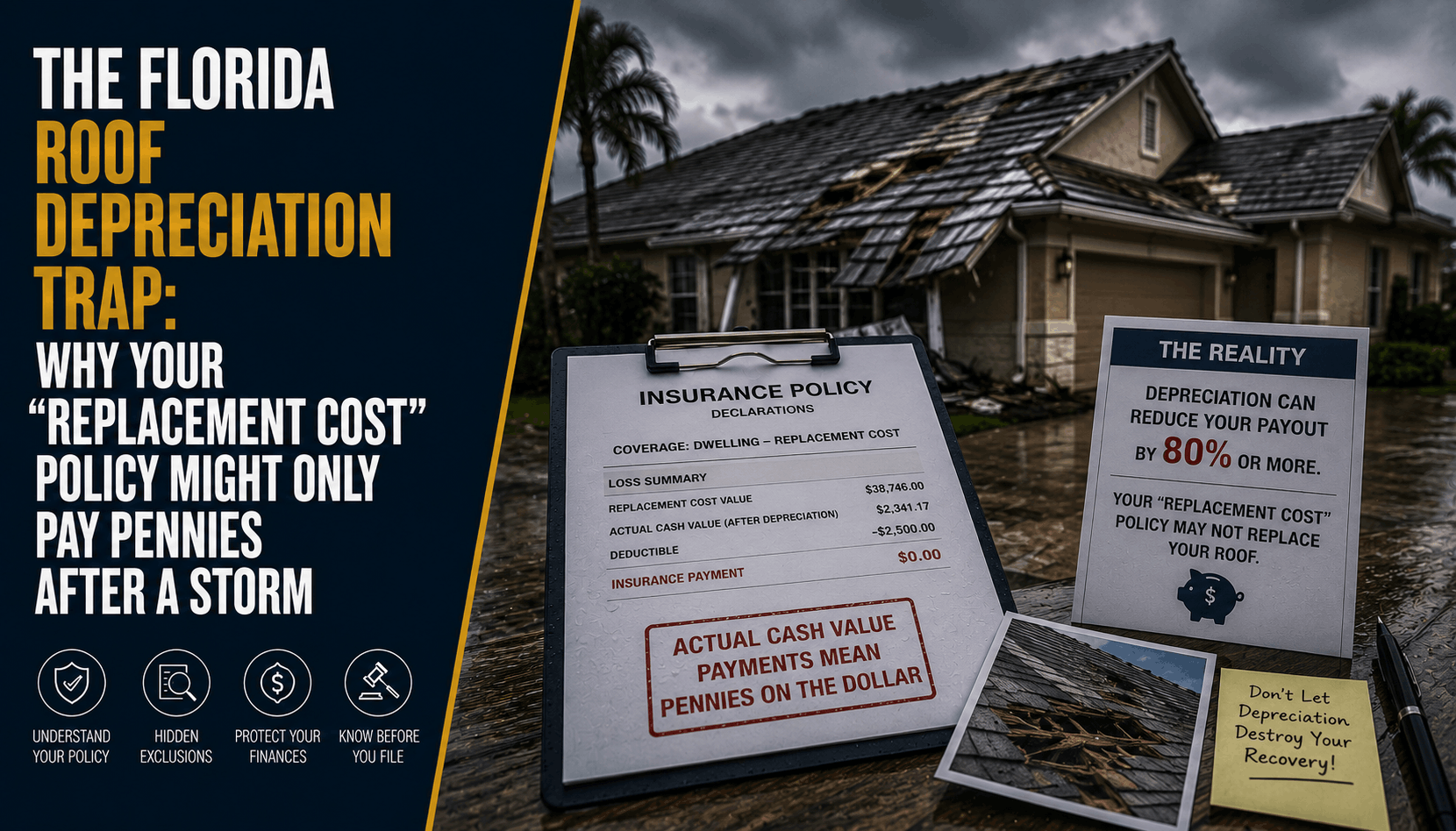

1. The Real Cost Breakdowns Across Different Roof Materials

When severe wind vectors or flying debris compromise an older roof, the insurance company no longer looks at what local contractors charge today. Instead, they calculate depreciation based on rigid mathematical formulas designed to reduce their payout volume.

The out-of-pocket reality for a typical Stuart homeowner under an ACV or depreciated roof schedule is staggering:

- Architectural Asphalt Shingles: If you have a standard shingle roof that is 12 years old, a complete tear-off and replacement in Martin County currently averages around $18,000. If your policy contains a standard depreciation schedule, the carrier can deduct roughly 60% of that value based on age. Your upfront insurance payout drops to just $7,200, leaving you to fund a massive $10,800 gap entirely out of your own bank account before your deductible is even applied.

- Concrete or Clay Tiles: For a Mediterranean-style tile roof that has hit its 18-year mark, a full structural replacement routinely costs $38,000 or more due to recent Florida Building Code updates. With a typical 45% depreciation penalty applied by the carrier, the insurer shaves $17,100 off the top. You must bridge that seventeen-thousand-dollar deficit out of pocket just to get a local crew to start the job.

- Standing Seam Metal Systems: While highly durable, premium metal roofs are frequently subjected to a 40% depreciation wall once they cross 20 years of age. On a $42,000 total wind-damage replacement bill, your carrier will legally legally withhold $16,800. If you do not have those personal cash reserves liquid, your home remains exposed to the elements.

2. The 2026 Florida Rules: SB 808 and the 25% Rule Myth

Navigating the legal framework of Florida property claims in 2026 requires understanding how state legislation actively impacts your coverage limits. Two major factors dominate roof claims today:

The 15-Year Inspection Safeguard (SB 808)

Under Florida's active insurance guidelines (SB 808), property insurance providers cannot automatically deny your policy renewal or cancel your coverage solely because your roof is greater than 15 years old, provided it is a steep-slope roof. However, there is a catch: you must hire an authorized inspector at your own expense to certify that the roof has at least 5 years of useful life remaining. While this keeps your policy active, it does not stop the carrier from switching your wind-damage coverage to a depreciated roof schedule at your next renewal.

The Modified 25% Building Code Rule

Many homeowners are still operating under the old assumption that if greater than 25% of a roof is damaged, the insurance company is legally forced to buy a whole new roof. In 2026, that rule is heavily modified. If your roof was built or fully replaced after March 1, 2009—meaning it already meets the structural standards of the 2007 Florida Building Code or newer—local building departments allow for partial, localized repairs rather than a mandatory full replacement. Insurers will use this code exception to pay for minor patches instead of funding a full roof line, even if a significant portion of your shingles are compromised.

3. How to Protect Your Home and Savings Account

Allowing an un-audited property contract to sit in your filing cabinet leaves your household wealth completely vulnerable to the next severe storm track. At Walker Insurance Agency, we advise Stuart residents to protect their properties using a clear, three-step evaluation:

- Step 1: Dissect Your Complete Policy Jacket. Do not rely on the one-page declarations summary. Request the full 100-plus-page policy booklet from your carrier and search explicitly for terms like "Roof Surface Reimbursement Schedule," "Actual Cash Value Roof Endorsement," or "ACV Limitation."

- Step 2: Install a Secondary Water Barrier Proactively. If you are planning minor repairs or preparing for an upgrade, ensure your contractor installs a self-adhering polymer underlayment (peel-and-stick). This not only prevents interior water leaks if wind tears shingles away, but it also triggers substantial wind-mitigation credits that lower your baseline premiums.

- Step 3: Secure an Independent Portfolio Audit. Work with a dedicated local broker to strip away restrictive depreciation endorsements and move your asset to a true, non-restricted Replacement Cost Value policy, or buy down your financial risk with an isolated, manageable flat roof deductible.

Why Working with an Independent Agency is Vital

Attempting to protect complex coastal property assets through a generic corporate smartphone application or an automated online form guarantees you will miss the hidden exclusions that lead to claims denials. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to defend your property line.

The Walker Advantage:

- Endorsement Text Analysis: We thoroughly analyze your underlying policy forms to verify whether your roof surface is protected at actual replacement value or hidden under a sliding depreciation scale.

- Local Labor Volume Scaling: We align your policy limits with real, active contractor labor rates in Martin County so you are never left underinsured after a wind storm.

- Carrier Market Matching: As the stabilizing Florida market introduces 20 brand-new private insurance companies to the state, we continuously shop your profile to locate providers offering complete, non-restricted roof coverage at competitive premiums.

FAQ

1. If my mortgage lender approved my policy, doesn't that mean my roof replacement is fully covered?

No. Following recent federal policy adjustments from the Federal Housing Finance Agency, lenders like Fannie Mae and Freddie Mac now legally accept Actual Cash Value (ACV) roof policies to help lower homeowners' monthly escrow payments. Satisfying your mortgage bank’s bare minimum requirements does not mean your personal bank account is protected after a storm.

2. If wind blows off a few shingles, does my standard insurance cover the interior water damage from a roof leak?

Yes, generally. If a sudden, covered wind event creates a physical opening in your roof structure and rain enters, your standard homeowners policy will typically cover the resulting interior damage (drywall, flooring, personal property). However, the payout to fix the older roof surface itself will still be subjected to your specific roof depreciation schedules or your hurricane deductible.

3. How does my roof's age affect my primary hurricane deductible?

Your roof's age does not lower your deductible. If you carry a standard 2% or 5% hurricane deductible on a $400,000 home, your out-of-pocket obligation is a fixed $8,000 or $20,000 before insurance pays a dime. If your older roof surface is also hit with a heavy age depreciation penalty, the total calculated insurance payout might not even clear your deductible threshold, resulting in a total net payout of zero dollars.

Insulate Your Home Lifestyle Before the Storm Tracks West

Your roof is your home's primary shield, but leaving its protection to a basic, un-vetted insurance rider is an administrative gamble that can instantly compromise your family's hard-earned wealth. True peace of mind requires pulling back the curtain on your policy’s hidden fine print and ensuring your written contract matches the physical reality of your roofline.

Take control of your hurricane protection today. Contact Walker Insurance Agency for a comprehensive portfolio evaluation. We provide the visibility you need to eliminate hidden depreciation loopholes, deploy high-limit comprehensive roof riders, and protect your lifestyle safely in Stuart.

[GET A FREE QUOTE TODAY]

Call our personal lines division at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your property boundaries today.

Related Articles

The Florida Roof Depreciation Trap: Why RCV Policies Fail in 2026

Think your Florida home insurance covers 100% of a new roof after a hurricane? Discover the "Roof Surface Payment Schedule" trap leaving Stuart homeowners exposed.

Read More →

The Frame-Only Trick: Why Pool Enclosure Insurance Fails in 2026

Think your Florida screen enclosure rider covers everything? Discover "The Frame-Only Trick" that leaves homeowners paying 100% out of pocket for torn mesh this hurricane season.

Read More →

Does Florida Full Coverage Pay Medical Bills in a Hit-and-Run?

Relying on Florida "full coverage" auto insurance to pay your medical bills after a hit-and-run in 2026? Discover why it fails and leaves you broke.

Read More →