The Frame-Only Trick: Why Pool Enclosure Insurance Fails in 2026

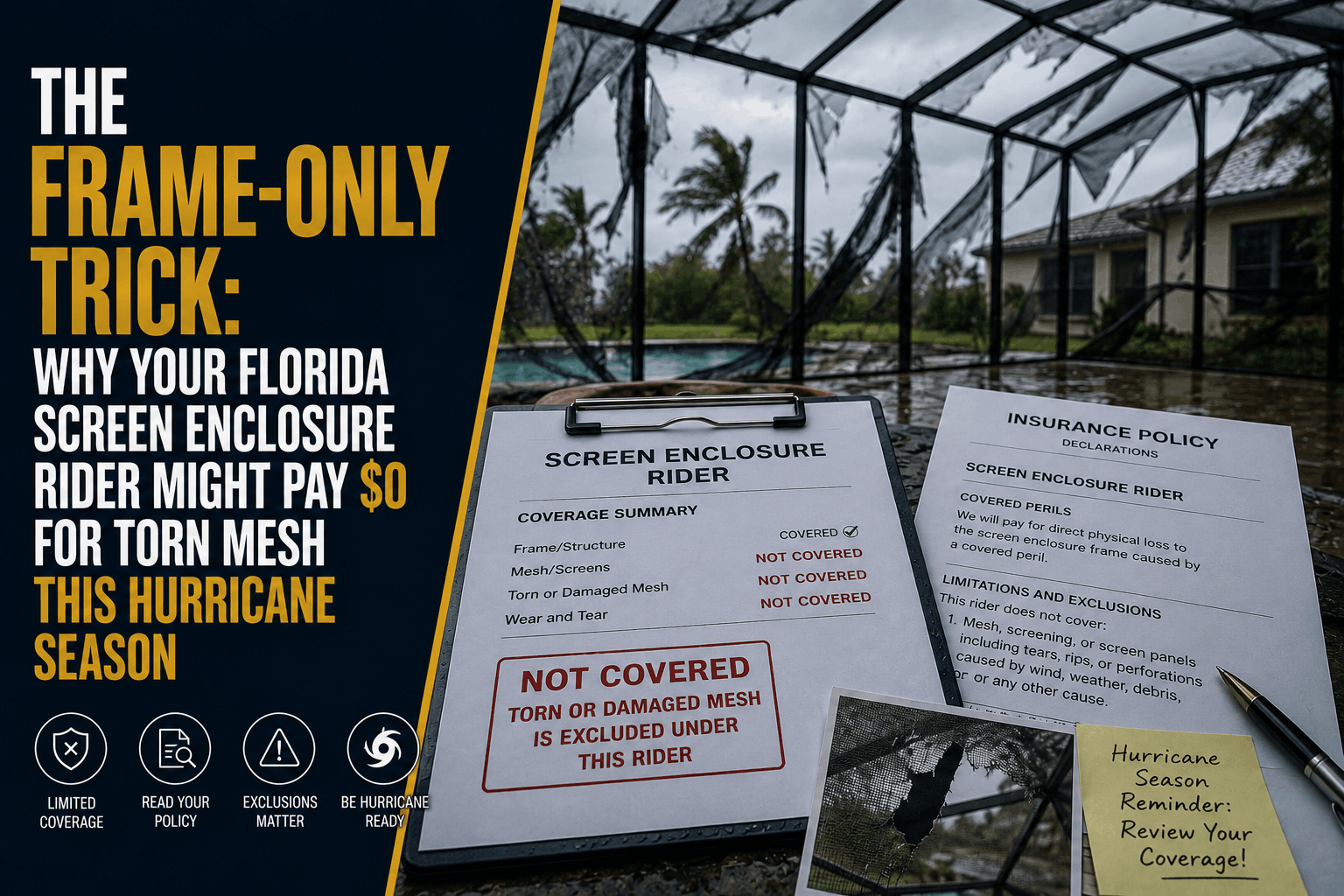

The Frame-Only Trick: Why Your Florida Screen Enclosure Rider Might Pay $0 for Torn Mesh This Hurricane Season

The Direct Answer: Even if you proactively paid extra for a "Screen Enclosure Endorsement" on your Florida homeowners policy, your carrier will likely pay exactly $0 to replace your torn mesh screening after a hurricane. There is an aggressive industry strategy known as the Frame-Only Trick. Under this restrictive policy language, the insurance company contractually covers only the physical, rigid aluminum structural beams and anchoring cables. The mesh fabric panels themselves—along with the massive cost of labor to rescreen the cage—are completely excluded.

In 2026, this fine-print trap is catching thousands of pool and patio owners completely off guard across the state. As private insurance carriers restructure their portfolios to minimize windstorm risk, "Frame-Only" clauses have quietly become the default baseline for standard property riders.

To achieve total visibility over your property defenses, you must understand that if a tropical storm or major hurricane forces heavy wind gusts through your zip code, ripping out 30 mesh panels but leaving the aluminum skeleton standing, your insurance company will legally deny the entire cost of the cleanup and rescreening.

1. The Anatomy of a Frame-Only Denial

When a hurricane strikes, the primary damage to a pool cage or lanai almost always begins with the screen mesh. The fabric acts like a giant sail, absorbing immense pressure until it stretches, splits, and tears away from its rubber spline tracks.

If you submit this multi-thousand-dollar rescreening claim under a standard, low-cost endorsement, a claims adjuster will navigate directly to the "Property Not Covered" or "Limitations" subsection of your rider jacket:

[Hurricane Damage: Bent or Collapsed Aluminum Extrusions] ───> COVERED (Minus Deductible).

[Hurricane Damage: Shredded Nylon, Fiberglass, or Poly Mesh] ─> 0% PAID via Frame-Only Clause.

The Labor Allocation Exclusion: Homeowners often assume that if a couple of aluminum struts bend, the policy will at least pay for a technician to come out, which might help cover the overall job. It won't. Under "Frame-Only" language, insurers systematically separate structural labor from textile labor. The policy will completely refuse to fund the specialized labor required to climb the cage, remove the old spline, and roll out new mesh over undamaged sections of the aluminum frame.

2. The 2026 Maintenance Overhead: A Severe Budget-Killer

Allowing this gap to remain in your home insurance portfolio leaves your personal cash reserves entirely exposed to record-high contractor overhead. If you have to fund a comprehensive patio rescreening out of pocket this summer, you face heavy cost accumulations across multiple fronts:

- The Material and Spline Overhead: Standard fiberglass or insect-resistant mesh for a standard-sized backyard pool enclosure promedias $1,500 to $3,500 for materials alone. Upgraded solar-shading or pet-resistant heavy-duty polymers can easily double that material baseline.

- The High-Altitude Labor Squeeze: Due to stringent structural permitting rules and strict workers' comp liability laws for high-altitude exterior work in Florida, professional labor rates for rescreening crews have skyrocketed. Re-splining a full, two-story or panoramic pool enclosure routinely commands $3,000 to $7,000 in pure labor costs.

3. How to Build a Comprehensive Enclosure Shield

If your outdoor living asset is currently sitting on an un-audited property contract, your emergency funds are entirely vulnerable to the next storm tracker update. At Walker Insurance Agency, we advise clients to secure their pool cages using a precise, three-step defensive layout:

Step 1: Locate and Pull Your Current Policy Declarations & Rider Jackets

Step 2: Audit the Wording for "Frame-Only" or "Mesh/Fabric Excluded" Terms

Step 3: Bind an All-Perils Screen Rider That Explicitly Includes the Mesh Panels

===================================================================================

= 100% Comprehensive Safety From Structural Aluminum Foundations to Exterior Mesh

To close this loophole, you must verify that your Screened Enclosure and Carport Endorsement features explicit language stating that coverage applies to "the aluminum framing and the screening material attached thereto."

Furthermore, you must double-check the deductible rule. If your pool cage rider is tied to your primary Hurricane Deductible (2% to 10% of your home's total insured value), you will still end up paying out of pocket for minor or moderate tears because the cost won't clear the heavy structural deductible threshold. Look for preferred private carriers that allow you to isolate the screen rider under a separate, manageable flat $500 or $1,000 deductible.

Why Working with an Independent Agency is Vital

Attempting to manage complex coastal property assets through a generic smartphone application or automated online form ensures you will miss the fine-print exclusions that cause catastrophic claims denials. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to defend your property line.

The Walker Advantage:

- Rider Text Dissection: We thoroughly analyze your carrier’s underlying endorsement forms to confirm whether your screen mesh, framing members, or both are fully protected against tropical-force winds.

- Replacement Volume Scaling: We align your selected rider dollar limits with actual local Stuart contractor labor rates so you never find yourself underinsured after a storm.

- Carrier Market Matching: As the stabilizing Florida market introduces 20 brand-new private insurance companies to the state, we continuously shop your profile to locate providers that offer complete, non-restricted screen mesh coverage at the lowest available premium floors.

FAQ

1. If my screen enclosure collapses into my pool during a storm, will my standard insurance at least pay to clean up the mess?

A standard home policy without a screen enclosure rider will pay $0 for any part of the cleanup. If you carry a "Frame-Only" endorsement, the policy will pay to cut apart and remove the collapsed aluminum framing from your pool because that debris removal is necessary to repair a covered loss (the frame itself). However, the labor costs to fish the shredded mesh out of your pool water or clear it from your filtration pump will still be denied or severely limited.

2. Why do Florida insurance companies exclude the screen mesh by default?

From an actuarial standpoint, screen mesh has a nearly 100% failure rate when exposed to category-strength hurricane wind vectors or flying debris. Additionally, standard nylon and fiberglass mesh degrades naturally over 5 to 7 years due to constant exposure to intense Florida UV radiation. To avoid paying for routine material wear and tear under the guise of storm damage, carriers use the "Frame-Only" trick to shift that regular maintenance cost entirely onto the property owner.

3. Should I cut my pool screens open if a major hurricane is tracking directly toward Stuart?

Yes, but only if it can be done safely from ground level before the storm hits. If you do not carry a specialized rider that covers the mesh, or if your deductible is too high, using a utility knife to slice large "X" patterns into the center of the outer screen panels can save your entire structure. Slicing the mesh relieves the intense barometric wind pressure, allowing hurricane-force gusts to blow clean through the cage rather than catching the walls like a sail and collapsing the expensive aluminum frame.

Insulate Your Outdoor Lifestyle Before the Storm Tracks West

Your pool cage is an essential part of your Florida home, but leaving its structural protection to a basic, un-vetted insurance rider is an administrative gamble that can instantly compromise your household budget. True peace of mind requires pulling back the curtain on your policy’s exclusions and ensuring your written contract matches the physical reality of your backyard.

Take control of your hurricane protection today. Contact Walker Insurance Agency for a comprehensive portfolio evaluation. We provide the visibility you need to eliminate hidden frame-only loopholes, deploy high-limit comprehensive screen riders, and protect your family's hard-earned wealth safely in Stuart.

[GET A FREE QUOTE TODAY]

Call our personal lines division at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your property boundaries today.

Related Articles

Does Florida Home Insurance Cover Roof Replacement Cost in 2026?

Think your Florida home insurance covers 100% of a new roof after wind damage? Learn how new 2026 guidelines leave Stuart homeowners paying out of pocket.

Read More →

The Florida Roof Depreciation Trap: Why RCV Policies Fail in 2026

Think your Florida home insurance covers 100% of a new roof after a hurricane? Discover the "Roof Surface Payment Schedule" trap leaving Stuart homeowners exposed.

Read More →

Does Florida Full Coverage Pay Medical Bills in a Hit-and-Run?

Relying on Florida "full coverage" auto insurance to pay your medical bills after a hit-and-run in 2026? Discover why it fails and leaves you broke.

Read More →