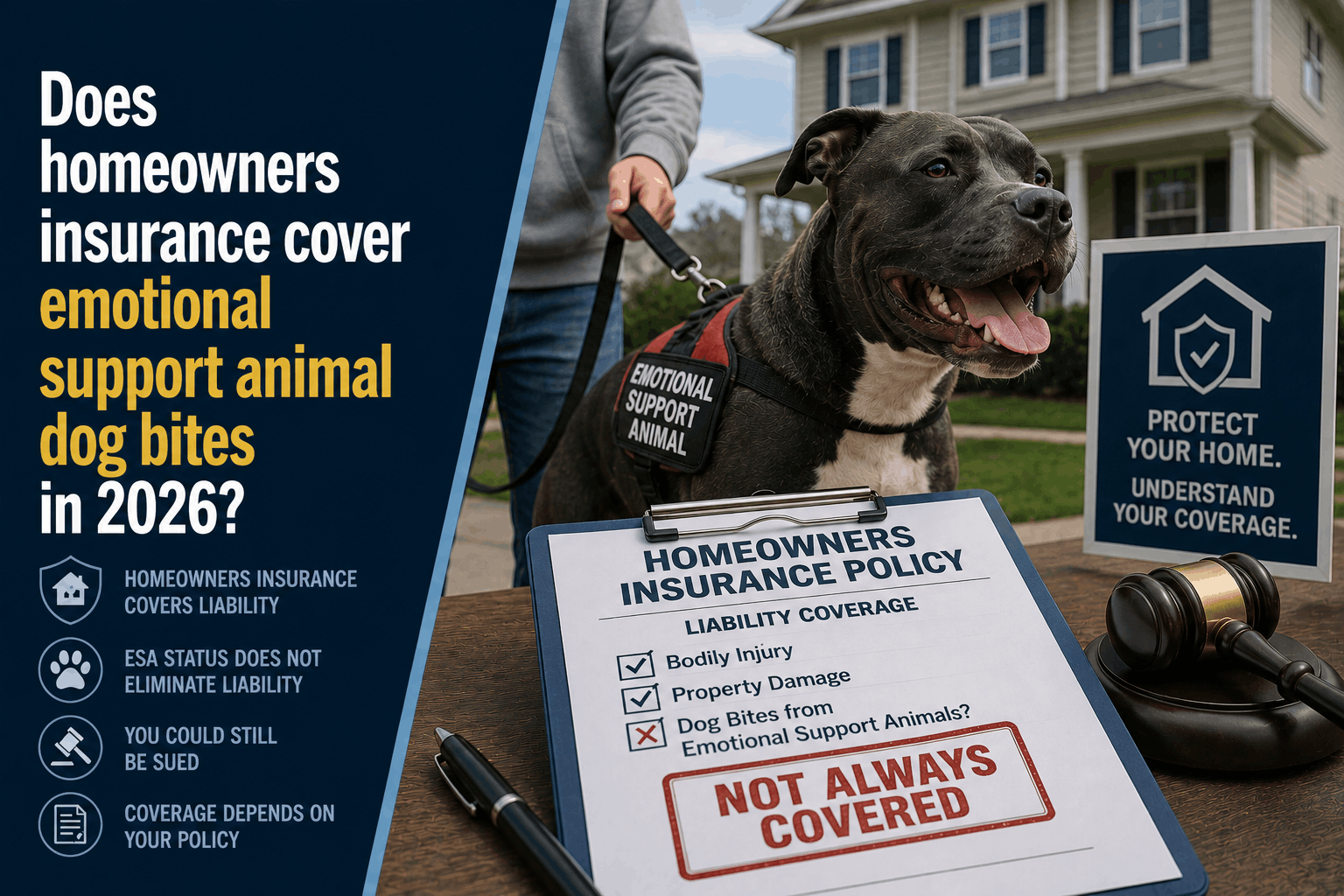

Does Homeowners Insurance Cover ESA Dog Bites? (2026 Guide)

Does Homeowners Insurance Cover Emotional Support Animal Dog Bites in 2026?

The Direct Answer: Legally, standard homeowners insurance policies treat an Emotional Support Animal (ESA) exactly like a standard household pet—not a trained service animal. This means your homeowners insurance personal liability section will cover a lawsuit or medical claim resulting from an ESA dog bite, but only if your policy doesn't already exclude your dog's specific breed or bite history.

In 2026, this distinction is incredibly high-stakes. Following HUD's sweeping enforcement policy shift, the federal government officially aligned housing standards with the Americans with Disabilities Act (ADA) definition. Because federal civil rights enforcement no longer recognizes untrained ESAs, insurance underwriters have tightened their restrictions.

If your ESA belongs to a blacklisted breed (such as a Pit Bull, Rottweiler, or German Shepherd), your homeowners policy likely contains a hidden animal liability exclusion, meaning your claim will be denied, leaving you personally exposed to asset garnishment.

1. The Underwriting Reality: ESA vs. Service Animal

Many property owners mistakenly believe that an ESA registration letter from an online medical professional forces an insurance company to cover their animal. It does not.

Insurance underwriters divide animals into two strict risk categories:

- Trained Service Animals (Protected): Under ADA and updated 2026 insurance parameters, these are dogs individually trained to perform specific physical or psychiatric tasks (e.g., guide dogs, blood-sugar alert dogs). Carriers rarely apply breed restrictions or exclusions to true service animals.

- Emotional Support Animals (Unprotected): Because ESAs require zero specialized training and provide generalized comfort, insurers classify them purely as standard pets. If your carrier excludes certain breeds from liability coverage, that exclusion applies to your ESA—even if you have a doctor’s note allowing the dog in your apartment.

2. How standard Home Insurance Handles the Claim

If your ESA is not an excluded breed and has no history of aggression, a third-party bite claim is split across two core coverages inside your policy:

- Medical Payments to Others (Coverage F): This pays for immediate, smaller medical bills (like stitches or antibiotic treatments) for guests injured on your property, usually capped between $1,000 and $5,000. It pays out regardless of who was at fault.

- Personal Liability (Coverage E): If the victim sues you for severe scarring, nerve damage, or lost wages, this coverage handles your legal defense costs and court judgments—typically starting at $100,000 to $300,000.

[ESA Dog Bite Incident]

│

├──\> Small medical bill? ───\> Medical Payments (Coverage F) pays up to $5,000

│

└──\> Severe injury / Lawsuit? ───\> Personal Liability (Coverage E) pays up to $300,000

The Household Exclusion: Personal liability insurance is strictly designed to protect third parties. If your ESA bites you, your spouse, or anyone living inside your household, your homeowners insurance will not pay a single penny. Your family must rely entirely on private health insurance.

3. The 2026 Anti-Fraud Breed Triggers

With the national average cost of a dog bite claim climbing past $64,000 due to rising medical costs and legal inflation, carriers are actively minimizing their exposure. If you own an ESA, you must audit your policy declarations page for these three common carrier strategies:

- The Total Breed Exclusion: Carriers like Progressive and Allstate maintain strict lists of "vicious or high-risk breeds." If your ESA falls into these genetic lines, the carrier excludes all liability for that animal by default.

- The "One-Bite" Non-Renewal: If your ESA has a clean history and bites someone, your current insurer will likely cover that first claim. However, once a bite is documented in the national insurance database (CLUE report), the carrier will immediately strip the coverage or non-renew your entire homeowners policy at your next term.

- The Liability Waiver Requirement: Some regional carriers will agree to write your home insurance policy only if you sign a formal rider legally waiving all corporate liability for animal-related incidents.

How to Close the ESA Insurance Gap

If you discover that your current homeowners policy excludes your emotional support dog, sitting on autopilot is an extraordinary financial gamble.

At Walker Insurance Agency, we advise pet owners to secure their assets using a dedicated, dual-layer strategy:

Step 1: Unbundle Animal Liability From Your Home Policy

Step 2: Secure a Standalone Specialty Animal Policy

======================================================

= 100% Guaranteed Liability Shield regardless of Breed

By purchasing a standalone Animal Liability Insurance Policy through specialty underwriters, you bypass your home insurance policy's breed blacklists entirely. These specialized lines are designed specifically to cover legal defense fees, medical judgments, and canine property damage up to $1 million—guaranteeing that an unexpected behavioral flashpoint won't destroy your retirement savings or cause you to face eviction.

Why Working with an Independent Agency is Vital

Relying on a generic online quote portal to analyze your pet liability risk is dangerous. Portals look at the cheapest baseline rate; they do not read the restrictive exclusion endorsements attached to the fine print. At Walker Insurance Agency, we provide the data-driven visibility you need to protect your family and your property.

The Walker Advantage:

- Exclusion Verification Audits: We meticulously read your policy jacket to pinpoint hidden animal or breed exclusions before an incident ever occurs.

- Specialty Market Placement: If your current carrier rejects your dog's profile, we immediately shop specialized markets to find separate, affordable animal liability shields.

- Umbrella Coverage Stacking: We structure comprehensive Personal Umbrella Policies (PUP) that sit on top of your primary lines, expanding your liability limits to $1 million or more to defend against catastrophic injury lawsuits in Stuart.

FAQ

1. Can my landlord evict me if my homeowners insurance doesn't cover my ESA dog breed?

Following the 2026 HUD enforcement shifts, if your homeowners insurance excludes your dog's breed and you do not carry a separate specialty policy, your landlord can argue that your animal creates an uninsurable liability hazard for the property. Landlords are legally permitted to mandate that all household pets or ESAs be backed by active, verified liability insurance as a condition of the lease.

2. Does my homeowners insurance cover my ESA if it bites someone at a public park?

If your policy includes standard animal liability without breed restrictions, that coverage is "portable." It will follow you and your dog anywhere in the world—including dog parks, vet offices, or vacation rentals—to defend you against third-party personal injury lawsuits.

3. What is the fastest way to verify if my ESA is covered?

Do not guess. Call your independent agent and request your formal Coverage Endorsements Page. Specifically ask if there are any Animal Liability Exclusions or Designated Breed Restrictions active on your policy ID number.

Protect Your Hard-Earned Assets from an Unpredictable Bite

An emotional support animal provides invaluable mental health relief, but a single stressful encounter can transform your companion into a massive financial liability. In the modern, highly restrictive legal environment, hoping your standard home policy covers an untrained animal is no longer a viable defense.

Claim your custom coverage check today. Contact Walker Insurance Agency for a comprehensive 2026 Policy Review. We provide the visibility you need to eliminate hidden breed traps, verify your true liability lines, and drive down your real cost of living safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us secure your home and assets today.

Related Articles

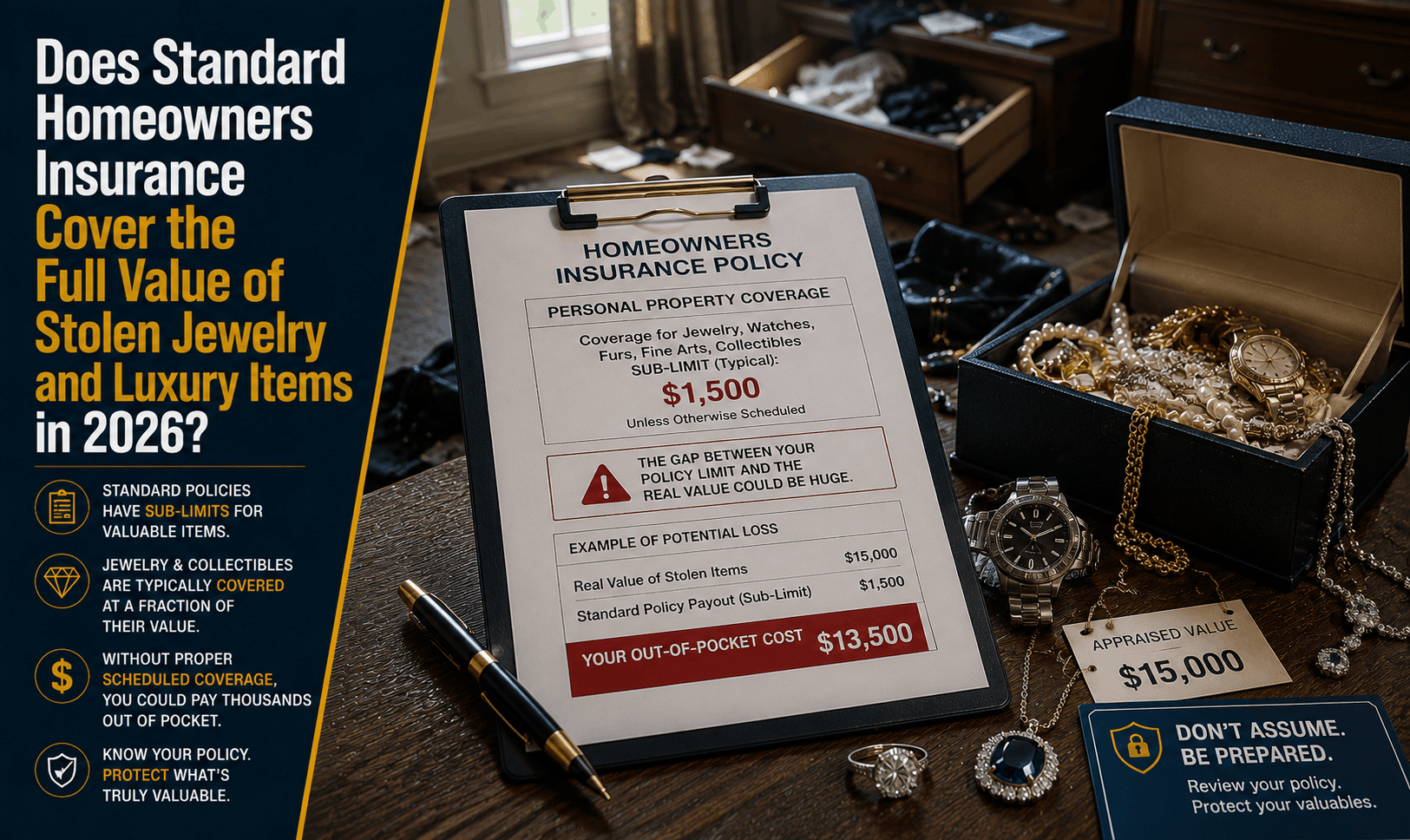

Does Homeowners Insurance Cover Stolen Jewelry & Luxury Goods? (2026)

Had luxury watches or jewelry stolen? Learn why standard homeowners insurance caps theft payouts at $1,500 and how to fully insure your high-value items.

Read More →

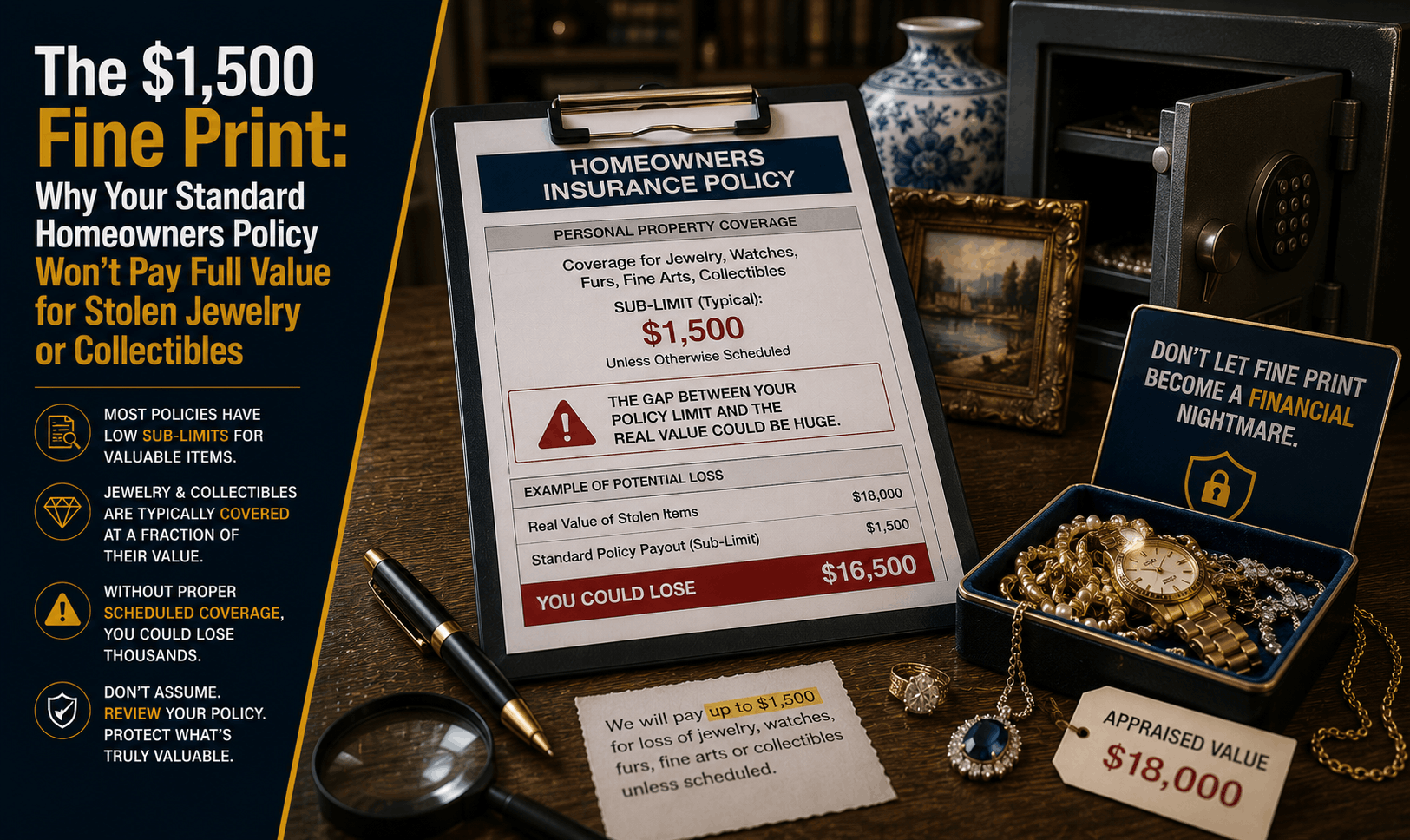

Does Home Insurance Cover Stolen Jewelry & Collectibles? (2026)

Had jewelry or valuables stolen? Discover why standard homeowners insurance limits theft payouts to $1,500 and how to fully insure your high-value items.

Read More →

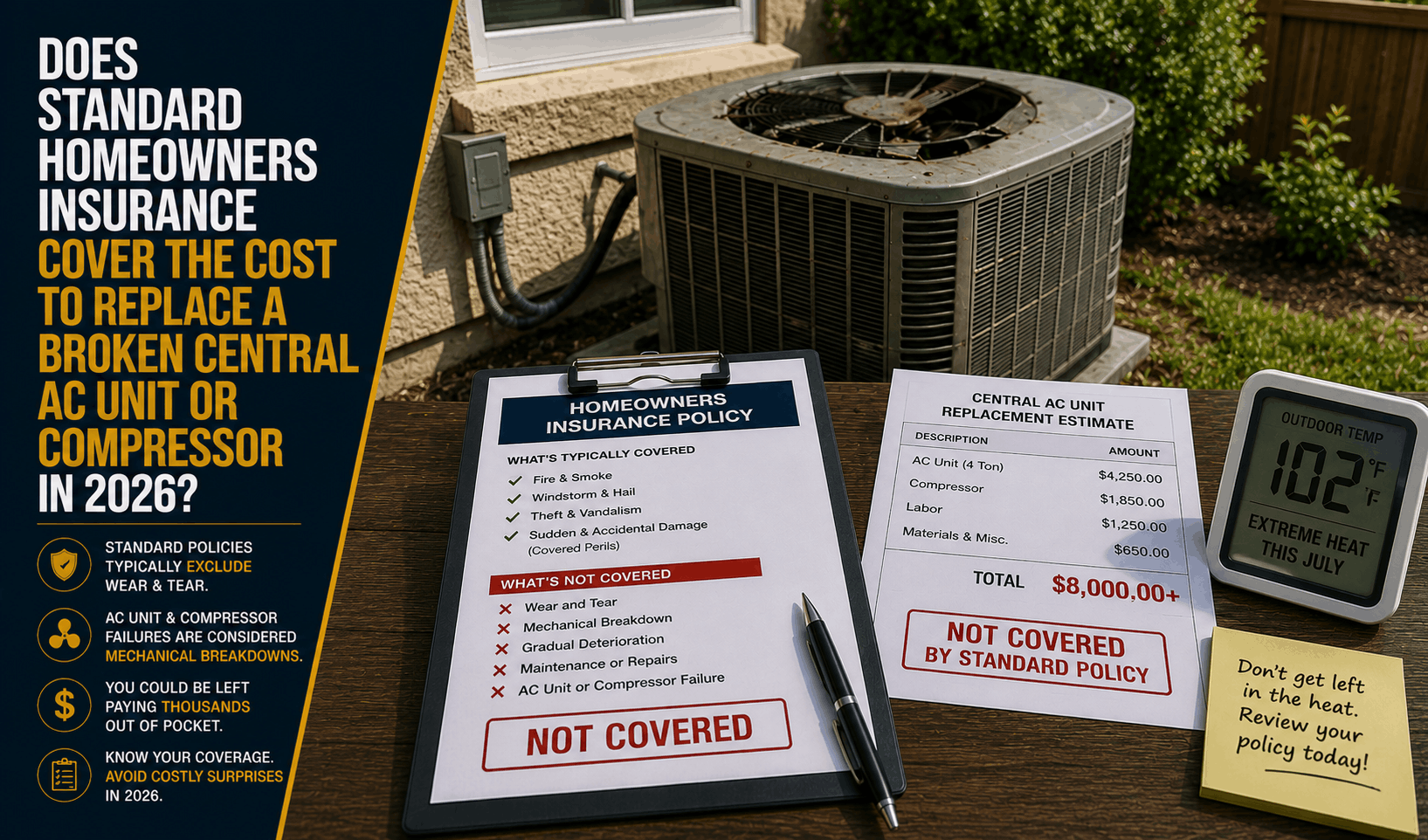

Does Homeowners Insurance Cover Broken AC Units? (2026)

AC broken in the summer heat? Learn why standard homeowners insurance won't pay to replace a broken central AC unit or compressor due to mechanical wear.

Read More →