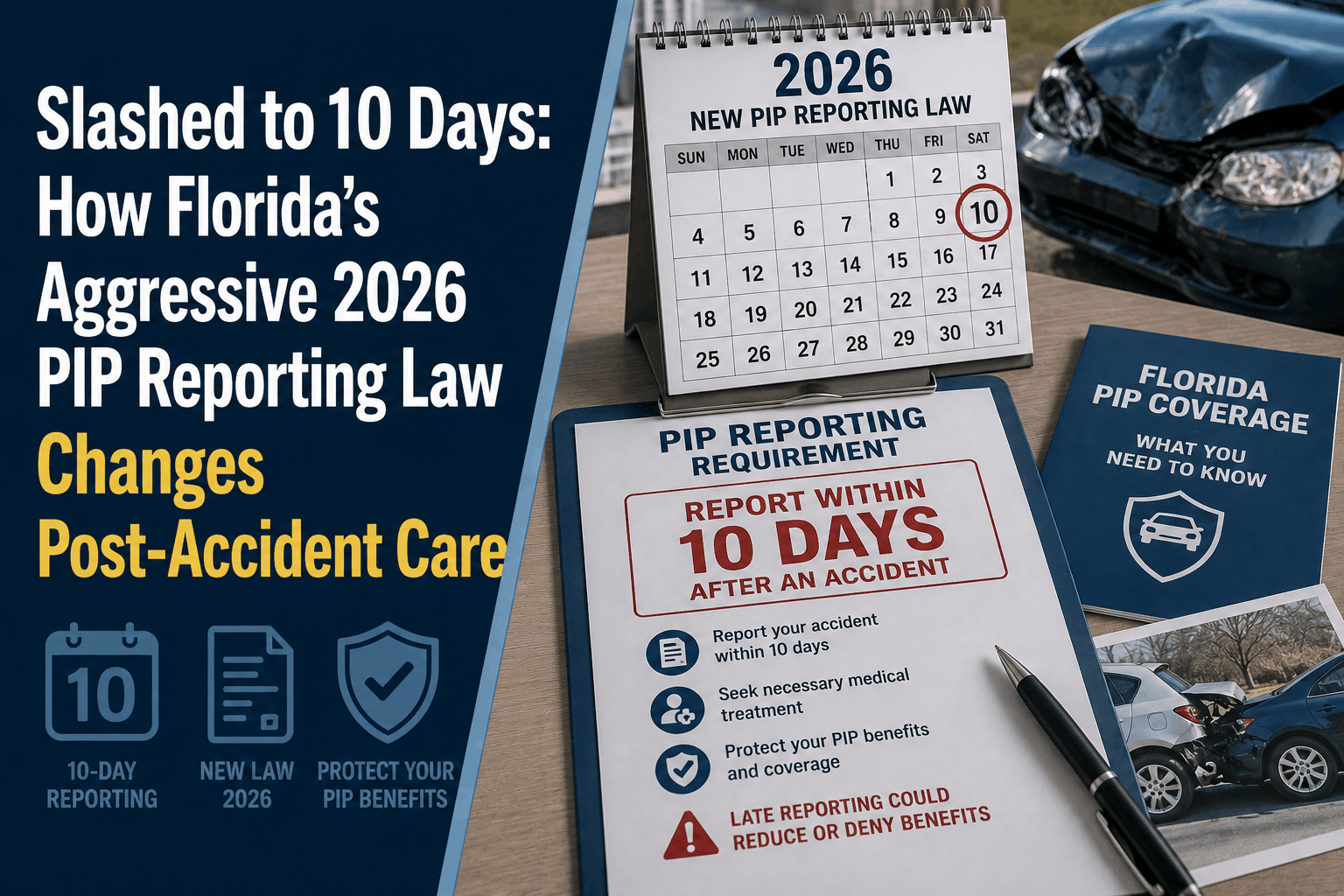

Florida’s 2026 PIP Reporting Law: The 10-Day Emergency Care Limit

Slashed to 10 Days: How Florida’s Aggressive 2026 PIP Reporting Law Changes Post-Accident Care

The Direct Answer: Under Florida’s strict automobile insurance laws, any driver or passenger seeking medical reimbursement after a car crash must navigate an aggressive timeline to secure their benefits. While the standard baseline for initial medical care under Florida Statute § 627.736 gives victims a 14-day window to see a doctor, a series of legislative updates heading into 2026 have dramatically heightened the pressure on post-accident reporting.

Failing to have a qualified professional certify your injuries quickly can trigger an automated denial or permanently cap your Personal Injury Protection (PIP) payouts at a mere $2,500 instead of the full $10,000 minimum you pay for.

To achieve total visibility over your financial and physical recovery, you can no longer afford to "wait and see" if your pain goes away. In the eyes of Florida insurers, an undocumented injury is a non-existent injury.

1. The Trap of the $2,500 Medical Cap

Florida remains a mandatory "No-Fault" state, requiring every registered driver to carry at least $10,000 in PIP coverage to cover 80% of medical bills and 60% of lost wages. However, the insurance industry utilizes a strict multi-tier framework that catches thousands of drivers off guard:

- The Baseline Window: You have exactly 14 days from the date of the crash to seek initial medical treatment from an approved provider (such as an MD, DO, chiropractor, or urgent care facility). Miss this, and your benefits drop to zero.

- The Emergency Medical Condition (EMC) Mandate: Simply seeing a doctor within the window does not unlock your full $10,000 policy limit. To access anything above $2,500, a licensed physician must explicitly diagnose you with an Emergency Medical Condition (EMC).

With insurance adjusters using advanced automated software to audit timeline gaps, any delay past the first few days gives carriers a legal loophole to argue that your injury wasn't acute or accident-related.

2. Why the Post-Accident Timeline is Shrinking

The tightening of medical documentation windows is part of Florida’s broader push toward insurance stabilization. Following massive anti-fraud legislation overhauls, insurers have cracked down on the post-accident timeline for several critical reasons:

- Combating "Delayed-Claim" Fraud: Lawmakers designed strict reporting parameters to stop predatory litigation mills from filing soft-tissue injury claims weeks after a minor fender bender.

- The Comparative Fault Shift: As Florida legal codes enforce strict fault limits (including the 51% bar rule for third-party liability), having definitive, time-stamped medical proof within days of the accident is vital to proving who caused the physical damages.

- Telemetry Synchronization: Insurers are increasingly matching black-box vehicle data with medical check-in timestamps. If your vehicle records a minor impact but you delay your clinical evaluation, the carrier's algorithm will automatically flag the claim for a fraud investigation.

3. The Danger of Hidden Soft-Tissue Injuries

The biggest victims of Florida's unforgiving reporting timelines are individuals who suffer from delayed-onset trauma.

- Adrenaline Masking: Immediately following a crash, your body floods your system with endorphins and adrenaline, completely blocking pain signals.

- The Whiplash Reality: Serious soft-tissue damage, cervical strains, and minor concussions frequently take 3 to 7 days to manifest as severe stiffness, headaches, or nerve pain.

If you spend the first week trying to treat your stiffness with over-the-counter anti-inflammatories, and delay booking an official medical evaluation, you are walking directly into a financial trap. If your medical records do not clearly establish an acute injury pattern early on, you will be left holding the bill for thousands of dollars in diagnostic imaging, physical therapy, and specialist visits.

Why Working with an Independent Agency is Vital

When the legal rules of the road lean heavily in favor of the insurance companies, buying your auto policy from a faceless online application leaves you entirely exposed. At Walker Insurance Agency, we provide the visibility you need to protect your health and your assets before an accident ever occurs.

The Walker Advantage:

- Immediate Post-Accident Advocacy: The moment you notify us of an incident, we map out your medical reporting requirements so you don't accidentally forfeit your PIP limits.

- MedPay Shielding Integration: We advise clients to stack Medical Payments (MedPay) coverage on top of their PIP. MedPay steps in to cover the 20% co-insurance gap that PIP leaves behind, ensuring you have 100% medical coverage out of the gate.

- Carrier Optimization: We shop the stabilizing Florida market to place you with top-tier carriers known for fair, transparent claims handling rather than automated, bureaucratic denials.

FAQ

1. Does a visit to an acupuncturist or massage therapist count toward my initial medical deadline?

No. Under Florida Statute, your initial evaluation must be performed by a state-approved medical professional. This includes Medical Doctors (MD), Doctors of Osteopathy (DO), Chiropractic Physicians (DC), Dentists, Physician Assistants, or Advanced Practice Registered Nurses (APRN). Alternative therapies will not satisfy the legal requirement to open a PIP medical claim.

2. What happens if I am too injured to complete my insurance paperwork within the first few days?

If you are hospitalized immediately following a crash, your emergency room admission, EMT transport, and hospital records completely satisfy the initial medical treatment mandate and establish your clinical timeline automatically.

3. If my PIP claim is capped at $2,500 due to a missing EMC finding, can I sue the at-fault driver for the rest?

Yes, you can still pursue a bodily injury claim against the at-fault driver's insurance to recover excess medical expenses. However, missing your early medical documentation windows gives the defense attorney a powerful weapon to argue that your injuries were exaggerated or occurred after the accident.

Take Control of Your Protection Before the Clock Starts

In the modern Florida auto market, a single administrative delay can instantly wipe out thousands of dollars in medical safety nets. Protecting your family requires knowing your statutory rights before a crisis happens on the highway.

Audit your auto coverages today. Contact Walker Insurance Agency for a comprehensive policy analysis. We provide the visibility you need to structure your limits safely, avoid claims traps, and lock in the most competitive rates available in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your drive today.

Related Articles

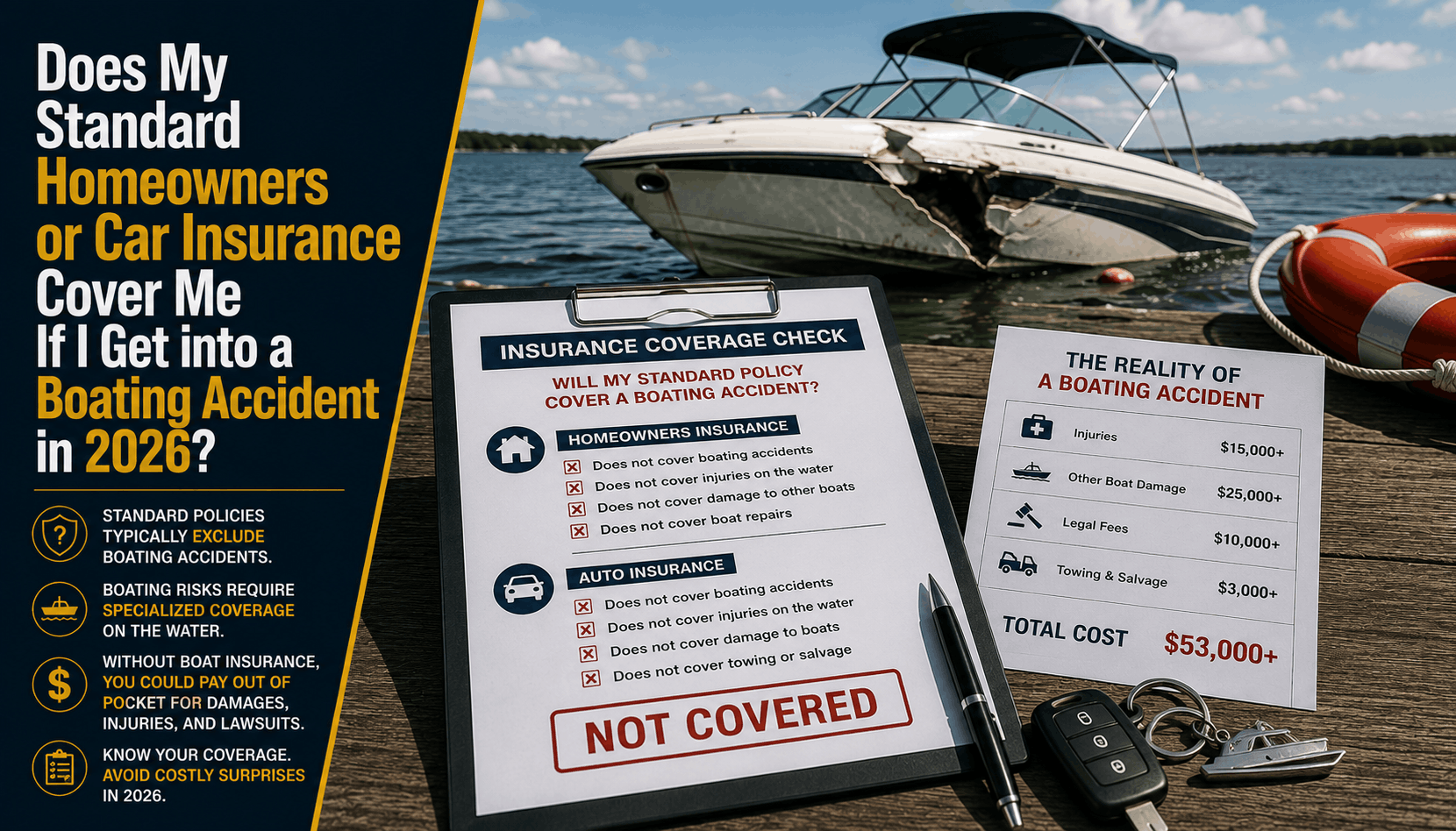

Does Home or Auto Insurance Cover Boating Accidents? (2026)

Planning a boat day in Stuart? Learn why relying on your home or auto insurance policies for watercraft liability is a dangerous financial gap.

Read More →

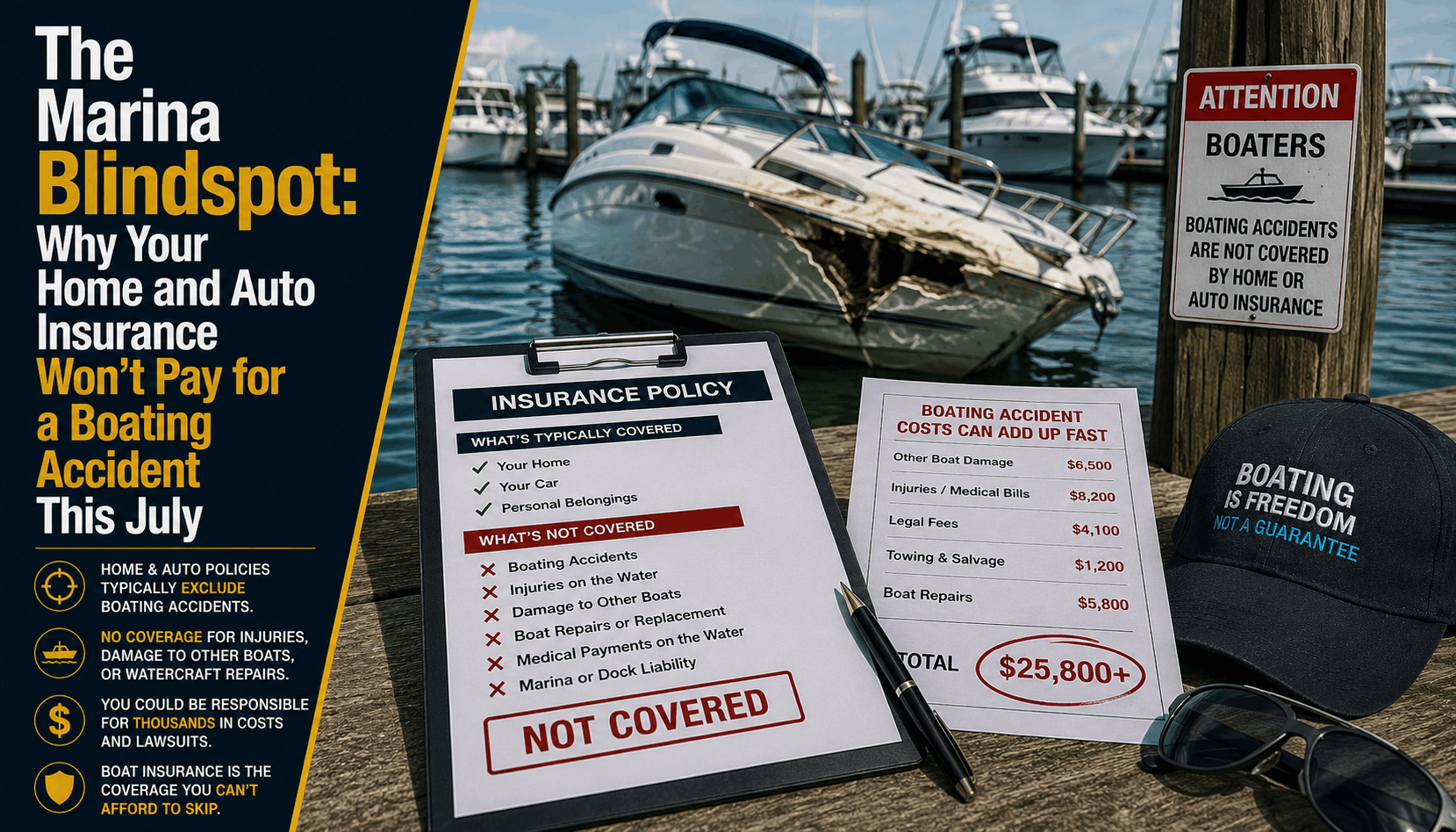

Why Home and Auto Insurance Won't Cover Boat Accidents (2026)

Planning a July boat day in Stuart, FL? Discover why relying on your home or auto insurance policies for watercraft liability is a dangerous financial blindspot.

Read More →

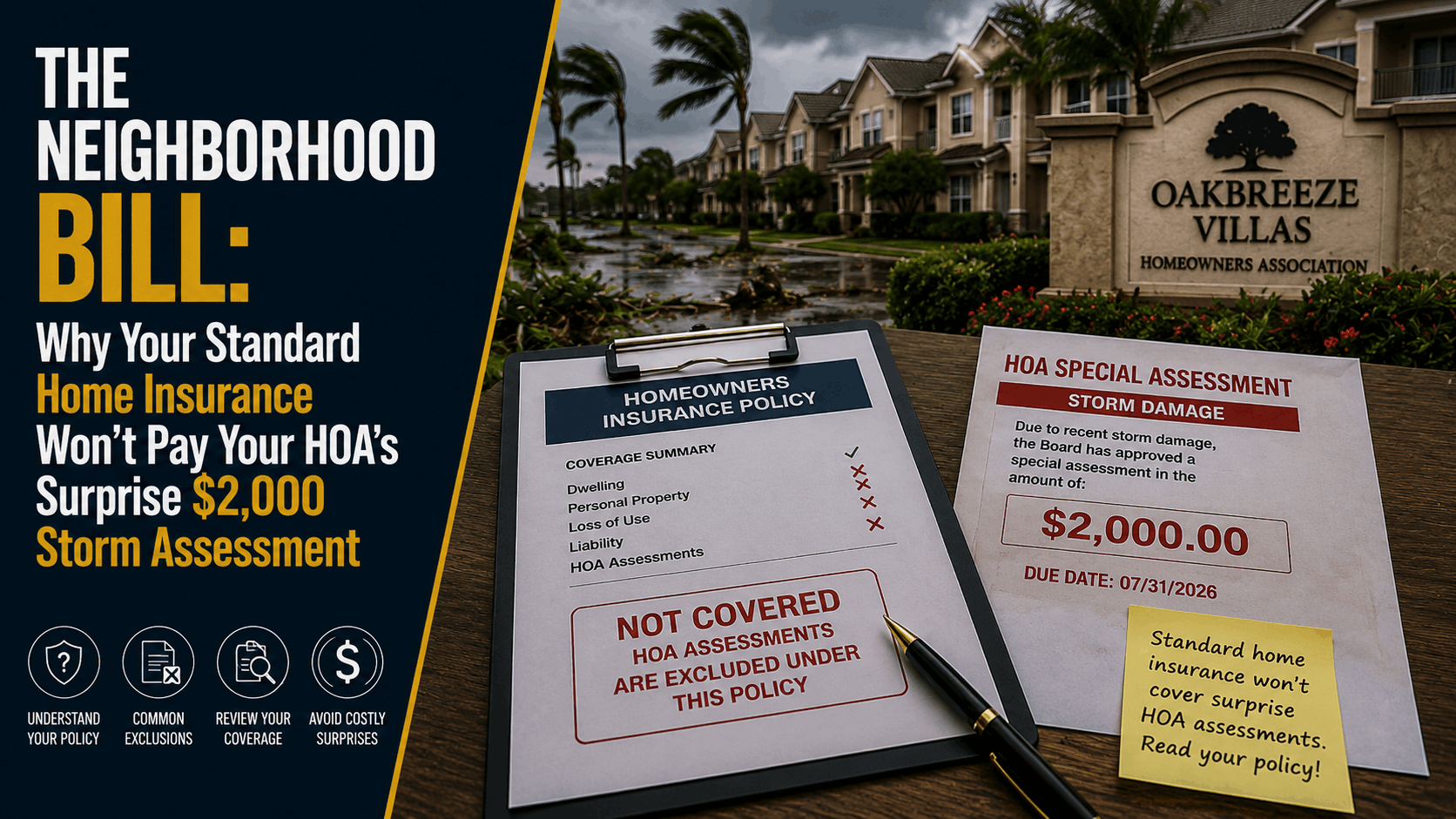

Why Home Insurance Won't Pay Your HOA Storm Assessment (2026)

Received a surprise HOA special assessment after a storm? Discover the critical loss assessment loopholes leaving Stuart homeowners completely exposed in 2026.

Read More →