General Liability vs. Professional Liability Florida (2026 Guide)

General Liability vs. Professional Liability: Which Does Your Small Business Need?

The Quick Answer: The difference between General Liability and Professional Liability comes down to physical vs. professional risk. General Liability covers "slip and fall" accidents, bodily injuries, and property damage caused by your operations. Professional Liability (also called Errors & Omissions or E&O) covers financial losses a client suffers due to your mistakes, bad advice, or professional negligence. In Florida, most businesses need General Liability to protect their physical space, while service-based professionals (consultants, accountants, and IT) almost always need Professional Liability to protect their expertise.

To achieve total visibility over your business protection in 2026, you must understand that these two policies do not overlap. Having one does not replace the need for the other.

General Liability: Protection for the Physical World

General Liability (GL) is the "foundation" policy for almost every Florida business. It is designed to handle third-party claims that arise from your daily operations or your physical location.

- What it covers: Medical bills if a customer trips in your Stuart office, repairs if you accidentally break a client's property, and legal costs if you are sued for libel or slander.

- Who needs it: Any business with a physical storefront, those who visit client homes (like contractors), or businesses that interact with the public.

- Florida 2026 Context: With increased foot traffic in Florida's growing commercial hubs, GL is often a requirement for commercial leases.

Professional Liability: Protection for Your Expertise

Professional Liability insurance is for businesses that provide specialized services or advice. It protects you when a client claims your work was inaccurate, late, or professionally negligent.

- What it covers: Financial losses your client suffers because of a clerical error, a missed deadline, or a technical oversight.

- Who needs it: Accountants, consultants, real estate agents, IT professionals, and engineers.

- Florida 2026 Context: Many Florida professional licenses and high-value client contracts now legally require proof of E&O coverage before work can begin.

Side-by-Side Comparison: Triggers and Costs

In 2026, Florida small businesses are seeing a wide range of premiums. Understanding the "trigger" for each policy helps you identify your specific gaps.

| Feature | General Liability (GL) | Professional Liability (E&O) |

|---|---|---|

| Claim Trigger | Physical accident or injury | Professional error or bad advice |

| Primary Loss | Bodily injury / Property damage | Financial loss to the client |

| Florida Avg. Cost | $40 - $70 per month | $60 - $90 per month |

| Required by | Landlords / Vendors | Clients / Professional Licenses |

Common Scenarios: Which Policy Responds?

To provide better visibility into your risk, let's look at how these policies play out in real life:

- Scenario A: An IT consultant spills coffee on a client's server, frying the hardware. Policy: General Liability (Property Damage).

- Scenario B: The same IT consultant fails to secure a network, leading to a data breach that costs the client $100k. Policy: Professional Liability (Negligence).

- Scenario C: A client trips on a loose rug in an accountant's office. Policy: General Liability (Bodily Injury).

- Scenario D: An accountant makes a math error that results in a $20,000 IRS penalty for a client. Policy: Professional Liability (Error/Omission).

Do You Need Both?

The short answer is yes for most service-based businesses. If you have an office where people meet you AND you provide professional advice, a gap in either policy could be bankrupting. In 2026, many Florida insurers offer a Business Owner’s Policy (BOP) which bundles General Liability and Property insurance, but you often have to add Professional Liability as a separate "rider" or standalone policy.

Why Working with an Independent Agency is Vital

In 2026, Florida's business insurance market is highly specialized. A "one size fits all" policy often leaves massive holes in your coverage. At Walker Insurance Agency, we perform a deep-dive audit of your service contracts to ensure your limits match your exposure.

The Walker Advantage:

- Industry-Specific Knowledge: We understand the unique liability risks for Florida professionals, from Clearwater to Fort Lauderdale.

- Contract Review: We ensure your policy limits meet the requirements of your largest clients.

- Claims-Made Expertise: Professional Liability is often "claims-made," meaning timing is everything. We help you manage your "Retroactive Dates" so you never lose coverage for past work.

FAQ

1. Is General Liability insurance required by law in Florida?

Florida law does not universally require General Liability for all LLCs. However, it is almost always required by landlords for commercial leases and by general contractors for subcontractors.

2. What is the difference between E&O and Professional Liability?

They are the same thing. "Errors and Omissions" (E&O) is simply the technical term often used in industries like real estate and tech, while "Professional Liability" is more common in medical or legal fields.

3. Does General Liability cover my employees?

No. General Liability covers third-party injuries (customers/vendors). Injuries to your own employees are covered by Workers' Compensation, which is mandatory in Florida for businesses with 4+ employees (or 1 in construction).

4. How much Professional Liability coverage do I need?

For most Florida consultants, a $1 million per-claim limit is the standard starting point, though your specific client contracts may dictate higher amounts.

Local Business Schema

Don’t Let a Misunderstanding Close Your Doors

One lawsuit is all it takes to wipe out years of hard work. Whether it’s a trip in your lobby or a mistake in your advice, you need to be prepared for the risks of doing business in 2026.

Protect your expertise today. Contact Walker Insurance Agency for a comprehensive business insurance audit. We will help you see the gaps in your coverage and provide the visibility you need to grow your Florida business with confidence.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us help you safeguard your business legacy.

Related Articles

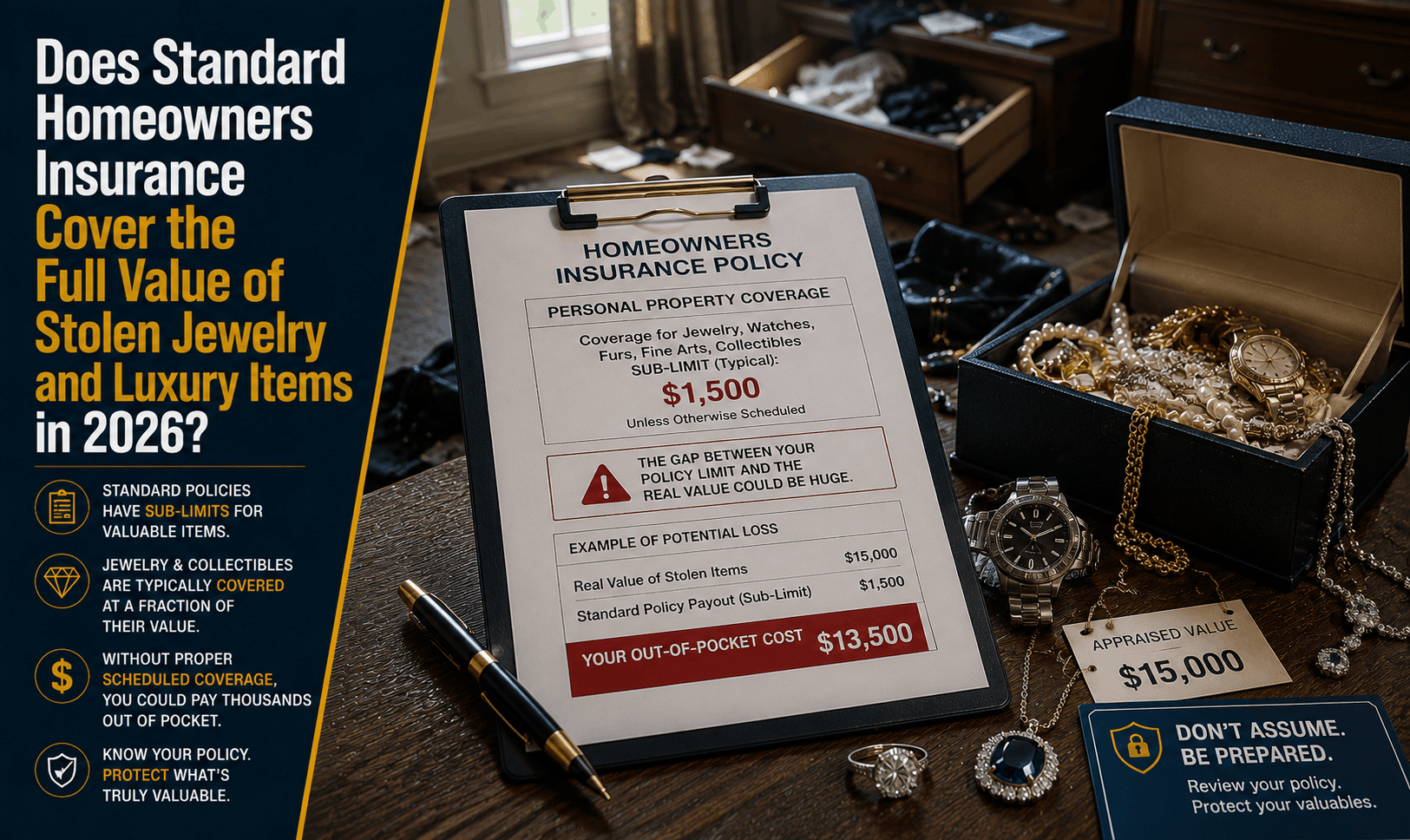

Does Homeowners Insurance Cover Stolen Jewelry & Luxury Goods? (2026)

Had luxury watches or jewelry stolen? Learn why standard homeowners insurance caps theft payouts at $1,500 and how to fully insure your high-value items.

Read More →

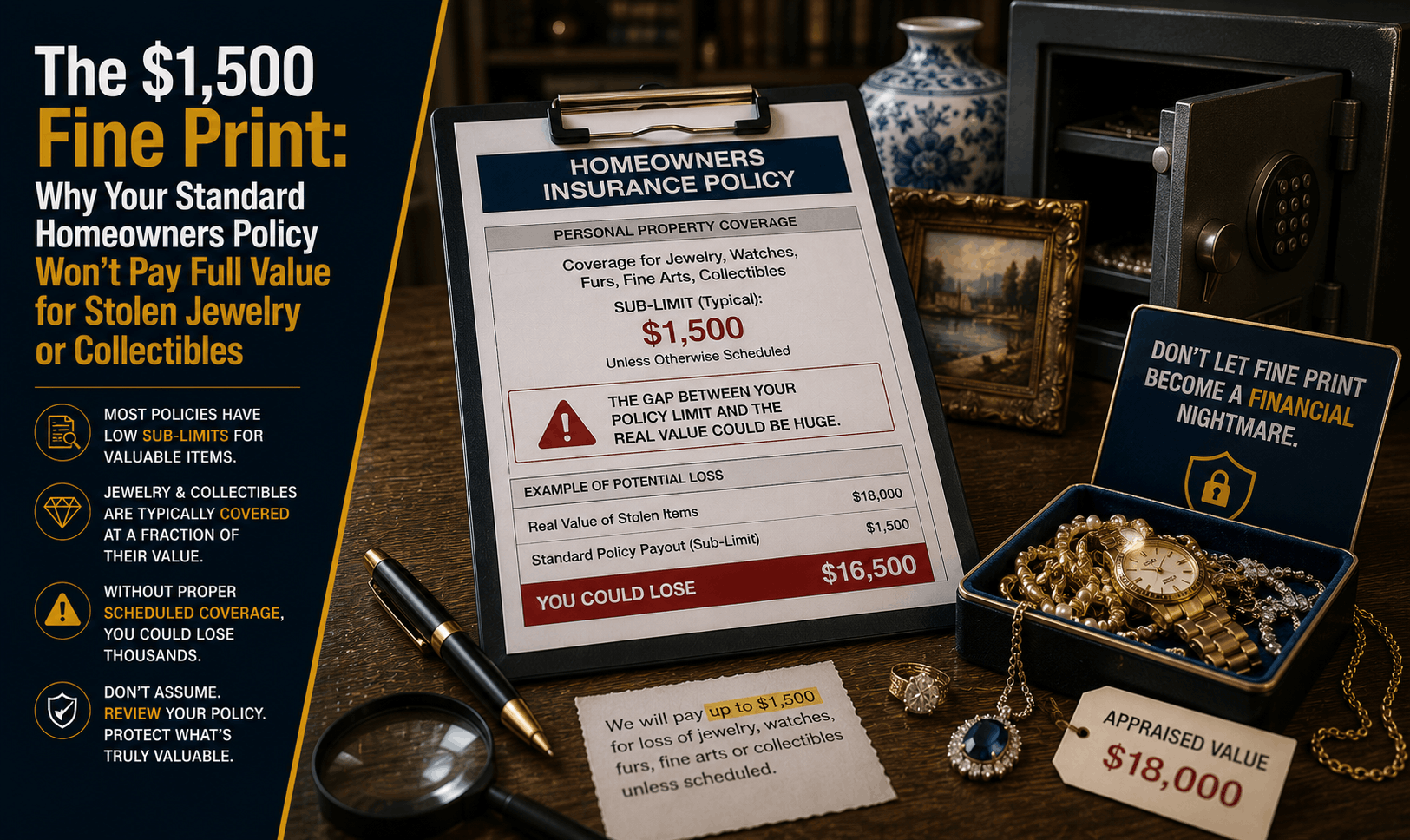

Does Home Insurance Cover Stolen Jewelry & Collectibles? (2026)

Had jewelry or valuables stolen? Discover why standard homeowners insurance limits theft payouts to $1,500 and how to fully insure your high-value items.

Read More →

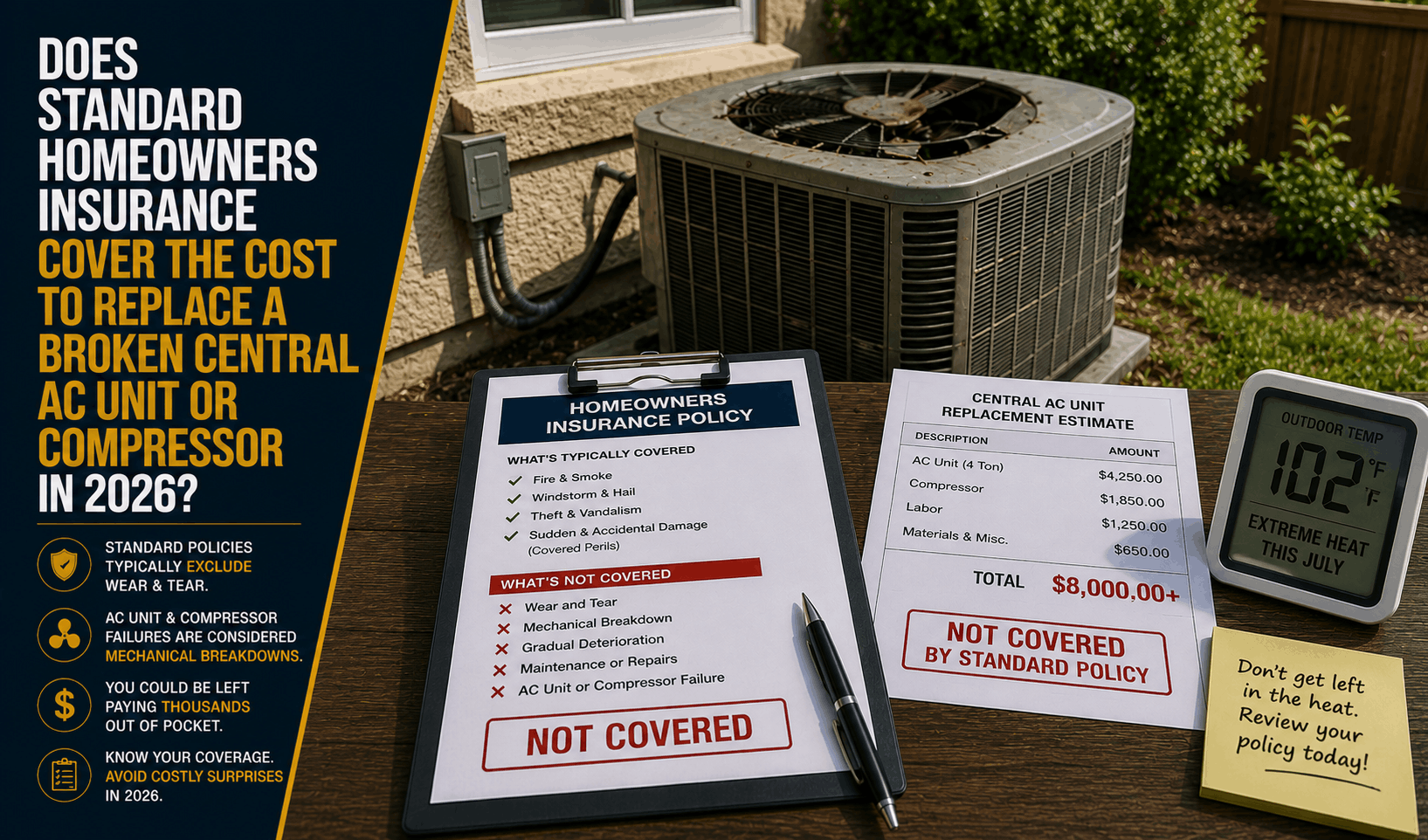

Does Homeowners Insurance Cover Broken AC Units? (2026)

AC broken in the summer heat? Learn why standard homeowners insurance won't pay to replace a broken central AC unit or compressor due to mechanical wear.

Read More →