How Much Liability Insurance Do I Need in Florida? (2026 Guide)

How Much Liability Insurance Do I Really Need in Florida?

The Direct Answer: While Florida law only requires a minimum of $10,000 in Property Damage Liability (PDL) and $10,000 in PIP, this is rarely enough to protect your assets. For the average Florida resident, insurance experts recommend a minimum of $100,000/$300,000 in Bodily Injury Liability and $50,000 in Property Damage. If you own a home or have significant savings, you should increase these limits to $250,000/$500,000 or supplement them with a $1 million Umbrella policy to ensure total financial visibility and protection against lawsuits.

In 2026, the cost of a single multi-vehicle accident or a serious injury claim in Florida frequently exceeds $100,000. Relying on state minimums leaves your house, bank accounts, and future wages directly exposed to legal judgments.

Why Florida's Legal Minimum is a Financial Trap

Florida is unique because Bodily Injury Liability (BIL)—the coverage that pays for others' medical bills—is not mandatory for most drivers to register a vehicle. This creates a dangerous "coverage gap."

The Risks of Minimum Coverage:

- Property Damage Reality: The average price of a new car in 2026 often exceeds $45,000. If you total a modern SUV with only a $10,000 limit, you are personally on the hook for the $35,000 difference.

- The Litigation Gap: Without BIL coverage, if you cause a serious injury, the victim's attorney can sue you directly for their medical debt and "pain and suffering."

- The "Target" Factor: If you own property in Stuart or have a visible business, you are a prime candidate for a lawsuit if your insurance limits are too low to cover the damages.

Data-Driven Recommendations Based on Your Assets

Choosing your liability limits should be based on what you have to lose, not just the monthly premium. Use this data-driven guide to find your bracket:

- Renters with Minimal Savings: 50/100/50 ($50k per person / $100k per accident / $50k property damage). This covers most moderate accidents.

- Homeowners & Families: 100/300/100. This is the "gold standard" for middle-class protection in Florida.

- High Net Worth (Assets over $500k): 250/500/100 + a $1M Umbrella Policy. This provides a total shield for your legacy.

Factors That Increase Your Liability Needs in 2026

Not all drivers face the same level of risk. You should consider higher limits if the following apply:

- Your Daily Commute: Driving on high-speed Florida arteries like I-95 or the Turnpike increases the likelihood of high-impact, high-cost collisions.

- Teenage Drivers on Policy: Statistically, households with young drivers face a higher frequency of at-fault claims.

- Business Use of Vehicle: If you use your car for work-related tasks, your personal liability exposure increases significantly.

The Role of Uninsured Motorist (UM) Coverage

In Florida, nearly 1 in 5 drivers is uninsured. A misunderstood part of liability planning is that your Uninsured Motorist (UM) coverage is usually capped at the same level as your Bodily Injury limits. To protect yourself from other people's bad decisions, you must carry high liability limits so that you can purchase high UM limits.

Why Working with an Independent Agency is the Smartest Move

At Walker Insurance Agency, we don't just "sell insurance"; we perform a risk audit. A website won't tell you that your liability is too low to protect your home's equity, but we will.

The Walker Advantage:

- Asset-Matching: We align your policy limits with your net worth for true visibility.

- Carrier Comparison: We shop multiple top-rated Florida insurers to find the highest limits at the most competitive price.

- Expert Advocacy: We understand the 2026 Florida statutes and how to structure your policy to avoid the "minimum coverage trap."

FAQ

1. What is the 100/300/100 rule in Florida insurance?

It refers to $100,000 of Bodily Injury per person, $300,000 of Bodily Injury per accident, and $100,000 of Property Damage Liability. It is the most common recommendation for homeowners.

2. Can I be sued if I have the insurance Florida requires?

Yes. Florida’s $10,000 minimum is just to get your tags. If you cause $50,000 in damage, the other driver can sue you for the $40,000 difference.

3. Does my liability insurance cover my own medical bills?

No. Liability insurance pays for others' injuries and property. Your own medical bills are covered by your PIP and MedPay.

4. Is an Umbrella policy expensive?

Surprisingly, no. A $1 million Umbrella policy usually costs between $200 and $500 per year, making it the most cost-effective way to protect large assets.

Local Business Schema

Protect Your Life’s Work Today

In Florida, "cheap" insurance can be the most expensive mistake you ever make. Don't let a single second on the road erase years of hard work.

Get the clarity you need. Contact Walker Insurance Agency for a professional liability audit. We will help you find the right limits to keep your assets safe and provide the visibility you need to sleep soundly.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. We’re here to protect your future, not just your car.

Related Articles

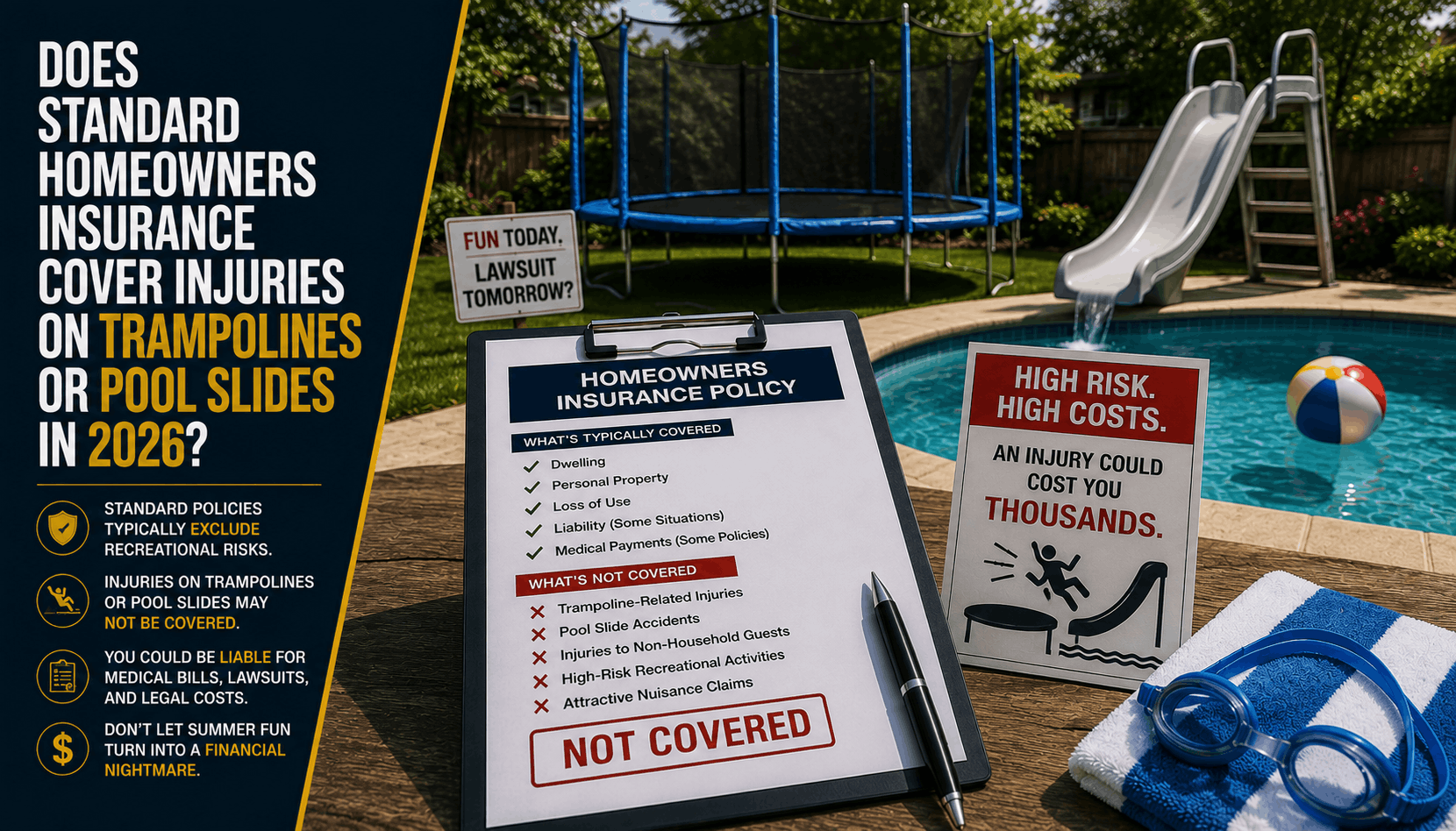

Does Homeowners Insurance Cover Trampolines or Pool Slides? (2026)

Planning summer fun in Stuart, FL? Discover why trampolines and pool slides are major homeowners insurance liability traps that can lead to dropped coverage.

Read More →

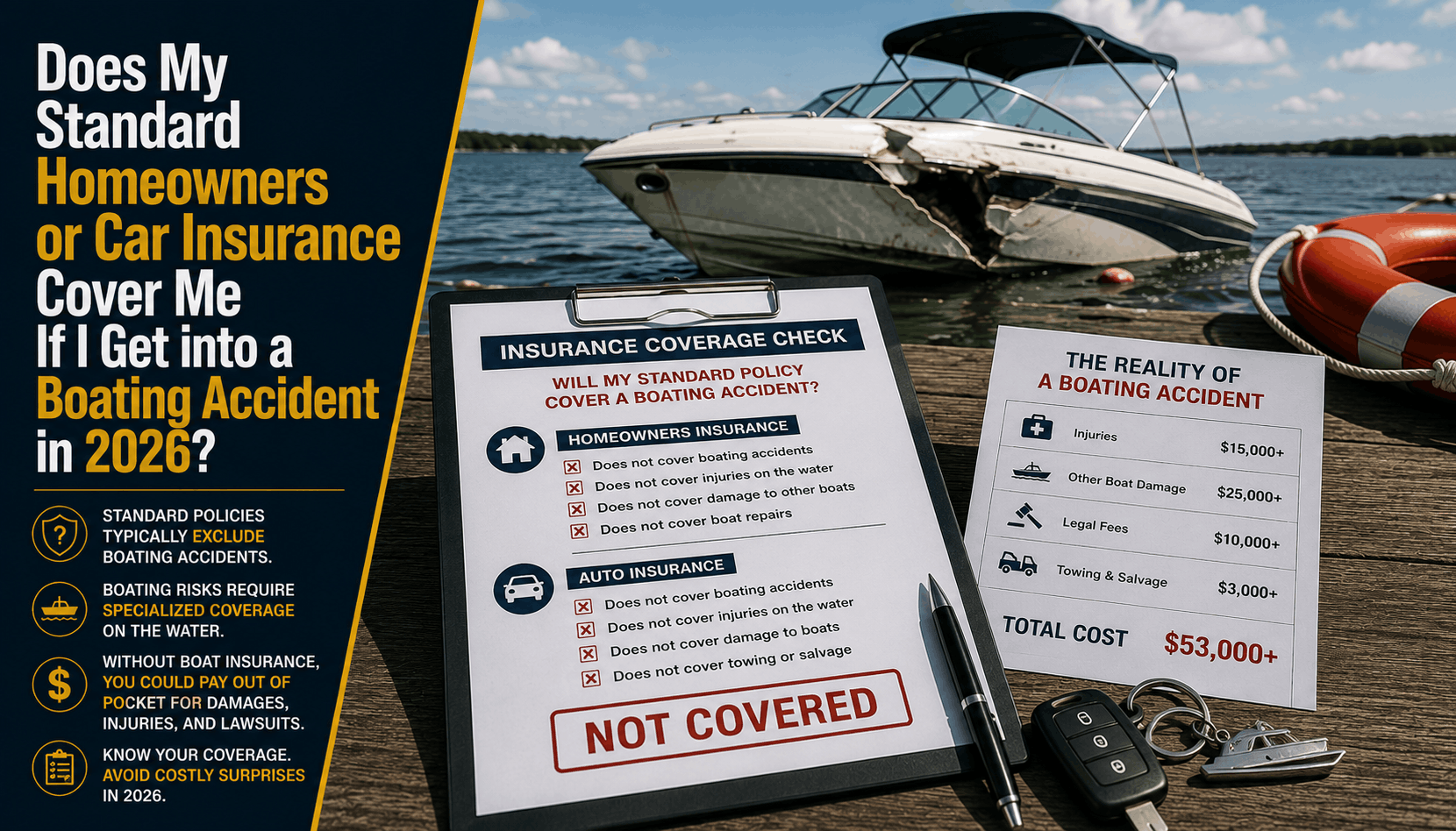

Does Home or Auto Insurance Cover Boating Accidents? (2026)

Planning a boat day in Stuart? Learn why relying on your home or auto insurance policies for watercraft liability is a dangerous financial gap.

Read More →

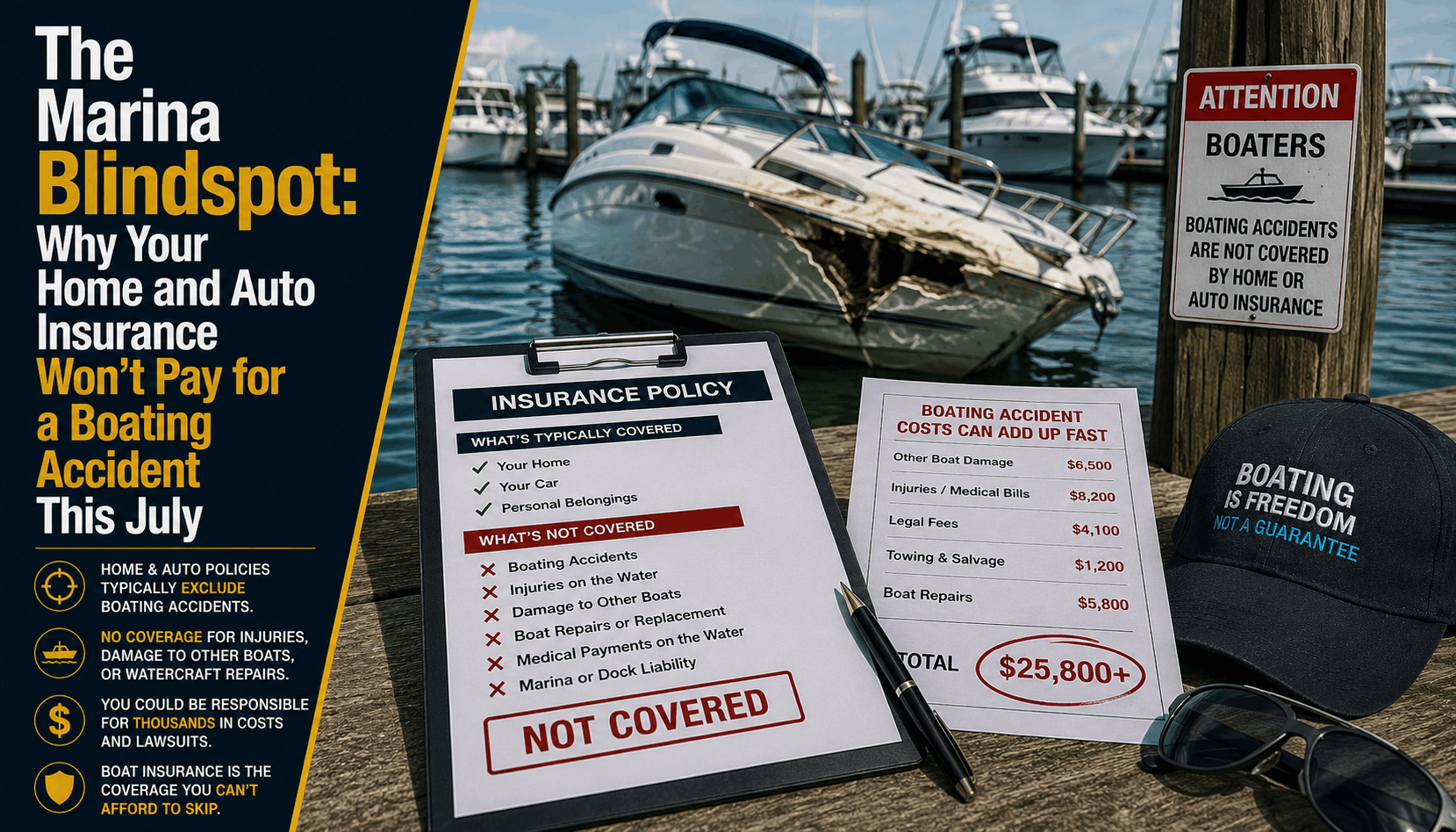

Why Home and Auto Insurance Won't Cover Boat Accidents (2026)

Planning a July boat day in Stuart, FL? Discover why relying on your home or auto insurance policies for watercraft liability is a dangerous financial blindspot.

Read More →