The Depreciation Trap: Regular Auto Insurance vs. Classic Cars (2026)

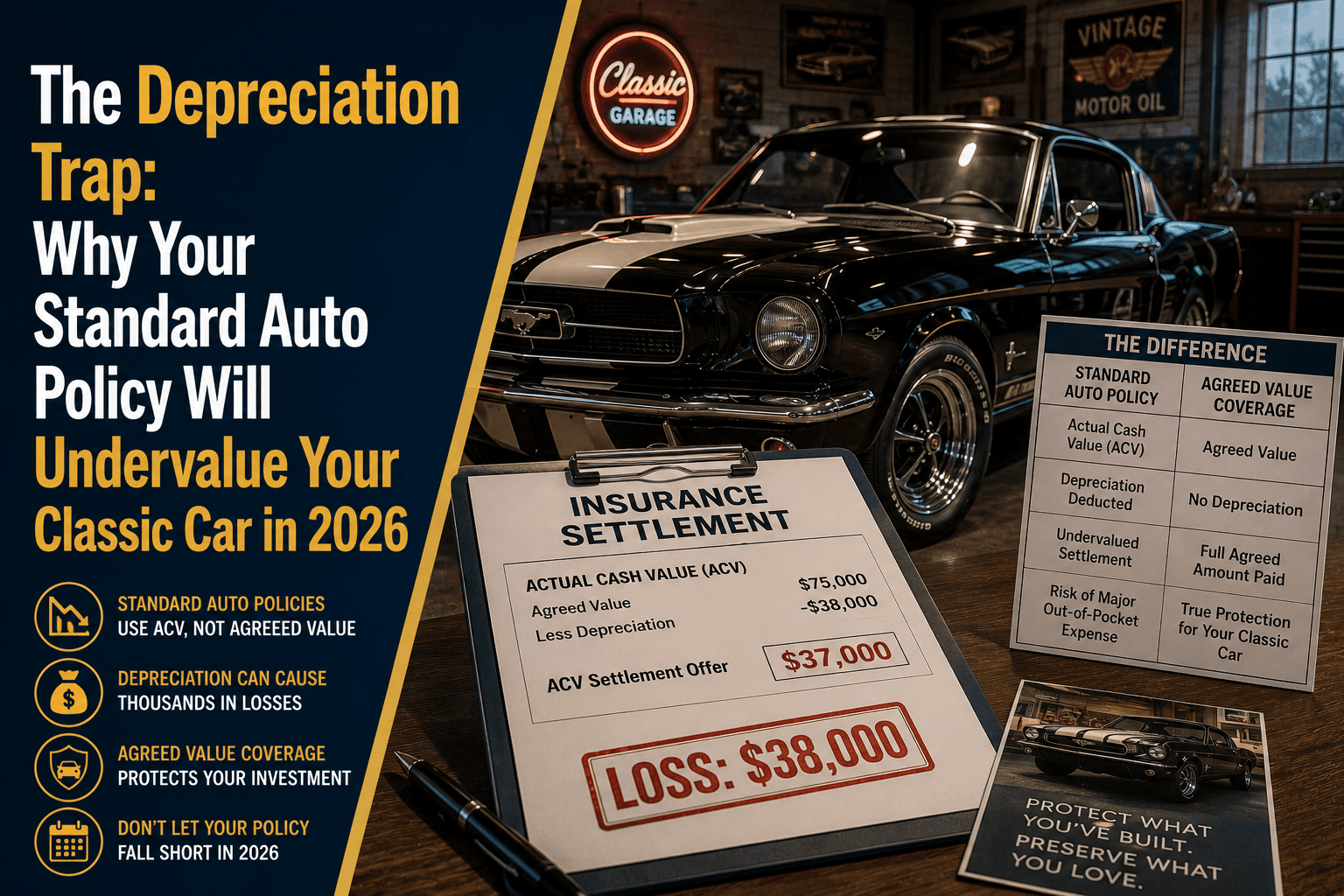

The Depreciation Trap: Why Your Standard Auto Policy Will Undervalue Your Classic Car in 2026

The Direct Answer: The "Depreciation Trap" is the catastrophic financial loss that occurs when you insure a classic, vintage, or highly modified vehicle under a standard personal auto insurance policy. Traditional insurance policies are contractually written to calculate total loss payouts based on Actual Cash Value (ACV), an underwriting metric that automatically factors in severe, ongoing chronological depreciation.

Velocity Restorations

In the complex 2026 collector car market, high-end vintage vehicles and trending 1990s–2000s classics are actually appreciating or holding steady as tangible assets.

If you crash a beautifully preserved classic and rely on a standard daily-driver policy, the carrier's automated valuation software will treat your prize vehicle like an ordinary, worn-out old car. They will strip away thousands of dollars for age and mileage, leaving you with a fraction of what the vehicle is actually worth on the open market.

1. The Mathematical Failure of Actual Cash Value (ACV)

Standard auto policies are designed for vehicles that lose value every time they leave the driveway. When a claim is filed, the insurer's software uses localized data to calculate the replacement cost of a basic used car minus depreciation.

Progressive

For an enthusiast vehicle, this algorithmic approach completely ignores reality:

- The Valuation Gap: ACV software looks strictly at basic data points—make, model, year, and mileage. It has no mechanism to account for a flawless concours restoration, a rare factory option package, or a professional engine build.

Bankrate - The Component Wipeout: If you spent $15,000 upgrading the suspension, transmission, and paint on a resto-mod, a standard policy treats those premium upgrades as invisible. In a total loss event, the payout cap defaults to the baseline book value of a standard, unmodified chassis.

2. 2026 Market Dynamics: The Rising Cost of Restoration

Protecting the true value of an enthusiast vehicle is more critical this year than ever before. Data from the 2026 Hagerty Market Index reveals a starkly divided collector landscape. While mainstream, entry-level classics are flattening out, the top end of the market and modern enthusiast vehicles—such as 1990s Nissan Skylines, C6 Corvette Z06s, and early 2000s BMW M5s—are experiencing strong demand and rising insured valuations.

Simultaneously, the macroeconomy has introduced severe hidden traps for classic owners:

[Rising Labor Costs for Specialty Shops] + [Supply Chain Scarcity for Vintage Parts]

= Soaring Repair Bills ──> Automated "Total Loss" Threshold Triggered Prematurely

The Threshold Danger: Because specialized labor rates and vintage body panels are more expensive than ever, a minor fender bender can easily generate a repair estimate that exceeds 70% or 80% of a standard policy's undervalued ACV calculation. The insurance company will instantly declare the vehicle a total loss, take your car to a salvage yard, and cut you a depreciated, bottom-dollar check.

3. Agreed Value vs. Stated Value vs. ACV

To step across the depreciation red line safely, you must understand the exact contractual terminology used in vehicle valuations:

| Valuation Metric | How It Settles Claims | Is Payout Guaranteed? | Recommended For |

|---|---|---|---|

| Actual Cash Value (ACV) | Replacement cost minus ongoing depreciation at time of crash. | No. Completely managed by adjuster software. | Everyday daily drivers (Commuter cars). |

| Stated Value | You declare a value, but the insurer retains the right to pay the lesser of that stated limit or ACV. | No. Creates a dangerous false sense of security. | Commercial or non-standard utility vehicles. |

| Agreed Value / Guaranteed Value | You and a specialty insurer lock in a fixed dollar amount upfront based on appraisals and photos. | Yes. Insurer pays 100% of the locked figure if totaled. | Classic, vintage, custom, and supercar lines. |

How to Safely Build a Collector Shield

If your classic vehicle is currently bundled on the exact same standard personal policy as your daily commuter SUV, you are actively exposed to the Depreciation Trap.

At Walker Insurance Agency, we unbundle enthusiast vehicles and transition them into specialized standalone programs:

Step 1: Secure a Professional Appraisal & Detailed Build Records

Step 2: Bind an "Agreed Value" Contract with a Specialty Underwriter

=====================================================================

= 100% Depreciation Exemption + Protected Collector Market Status

By placing your prize asset under a true Agreed Value Specialty Policy (through elite collector underwriters like Hagerty or Progressive Classic), you lock your vehicle's financial payout in advance. If a catastrophic total loss occurs, depreciation is legally completely removed from the equation. The exact number written on your declarations page is the exact number written on your settlement check.

Progressive+ 1

Furthermore, these specialized policies are frequently 30% to 50% cheaper than standard auto insurance because underwriters assume the vehicle is stored in a secure garage and driven strictly for pleasure, not a daily highway commute.

Why Working with an Independent Agency is Vital

Insuring a custom or historic vehicle through a automated online app is incredibly dangerous. Algorithms do not understand automotive history, rare production options, or restoration receipts. At Walker Insurance Agency, we provide the personalized visibility you need to defend your investment.

The Walker Advantage:

- Specialty Market Alignment: We evaluate your build sheet against the freshest 2026 price guides to ensure your Agreed Value limit perfectly mirrors current global auction values.

- Usage Tier Synchronization: We help you select flexible, limited-use mileage brackets that protect your weekend cruises without triggering regular-use policy exclusions.

- Unified Asset Bundling: We connect your specialty vehicle protection with your primary lines, keeping your total out-of-pocket overhead as low as possible in Stuart.

FAQ

1. Does a classic car policy allow me to choose my own repair shop? Yes. Unlike standard personal auto policies that use steering mechanisms to push you toward corporate, assembly-line direct repair facilities, top-tier classic car policies explicitly guarantee your right to take the vehicle to any high-end restoration or specialty fabrication shop of your choosing.

2. What qualifies a vehicle for an Agreed Value classic policy in 2026? Requirements vary by carrier, but generally, the vehicle must be stored in a fully enclosed, locked garage or secure facility. Additionally, it cannot be used as your primary daily commuter car, and all licensed drivers in the household must have their own separate, regular daily-use vehicles active on a personal policy.

3. Can I get Agreed Value coverage on a heavily modified "resto-mod" or tuner car? Absolutely. Specialized collector policies are perfectly designed to accommodate modifications. You simply provide a comprehensive build summary, photos of the engine bay and interior, and parts receipts to establish an accurate, mutually accepted valuation before the contract is bound.

Go Compare

Insure Your Passion for What It’s Truly Worth

Your classic car isn't just basic transportation—it's a rolling piece of history and a major financial investment. Leaving its protection tied to an ordinary, depreciation-driven policy is a gamble that will cost you everything when a claims adjuster opens their software after an accident.

Lock in your guaranteed valuation today. Contact Walker Insurance Agency for a comprehensive 2026 Collector Vehicle Valuation Review. We provide the visibility you need to bypass standard depreciation loops, secure a true Agreed Value shield, and preserve your automotive legacy safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us protect your investment today.

Related Articles

Does Collision Insurance Cover Hail & Tree Damage in 2026?

Did hail or a falling tree branch damage your car? Learn why collision auto insurance won't pay for storm damage and how comprehensive coverage protects you.

Read More →

Why Collision Insurance Pays $0 for Non-Crash Summer Damage (2026)

Did a tree branch, hail storm, or flying road debris hit your car this summer? Discover why collision auto insurance pays $0 and how comprehensive coverage protects you.

Read More →

Florida Minimum Auto Insurance Coverage Illusion (2026)

Driving with state-minimum auto insurance in Florida? Learn why carrying only PIP and PDL leaves your health and personal savings vulnerable after a crash.

Read More →