The Red Line: Why Waiting for the Weather Forecast Leaves You Uninsured

The Red Line: Why Waiting for the Weather Forecast Will Leave Your Home Uninsured in 2026

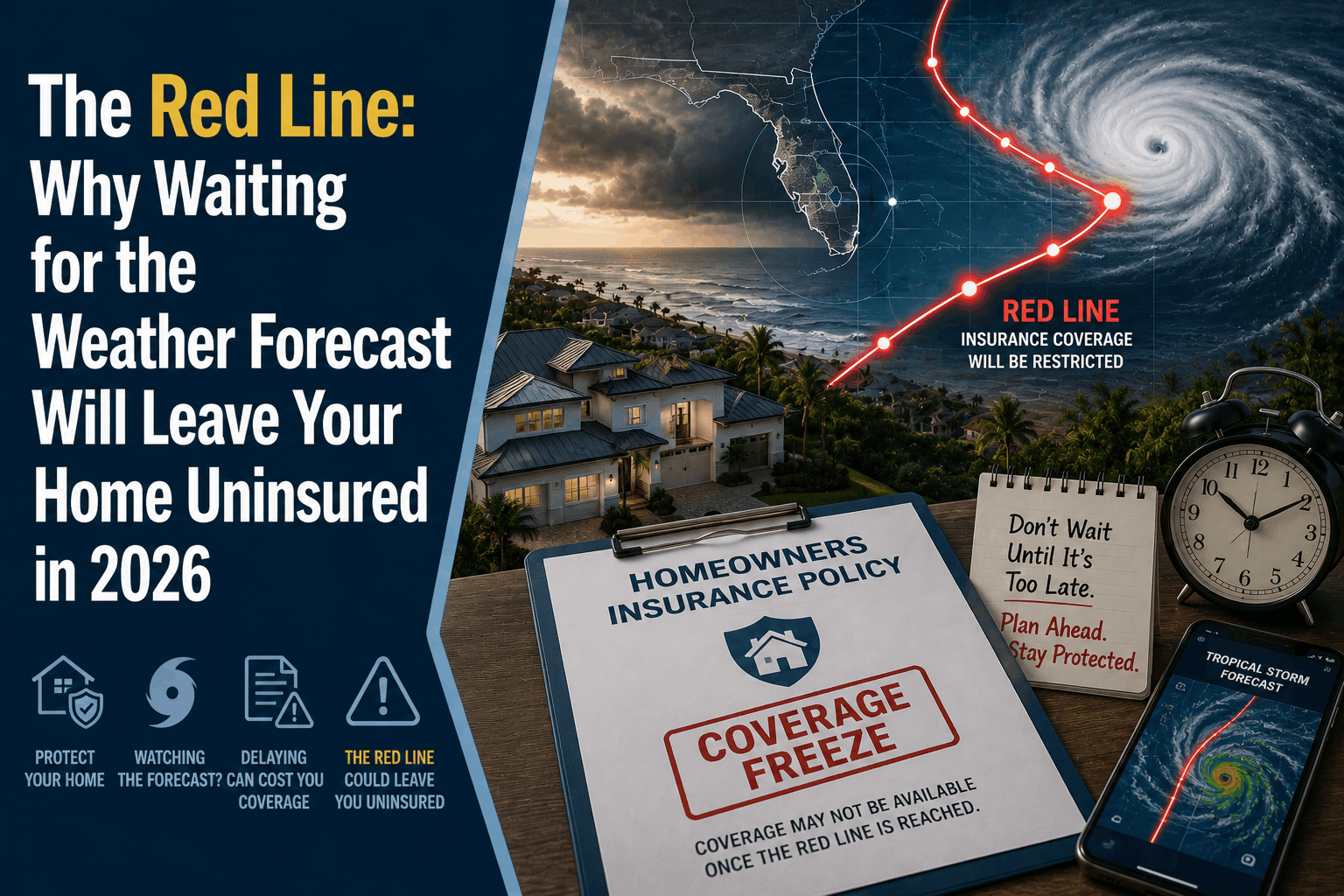

The Direct Answer: The "Red Line" represents the absolute point of no return for your home's safety in Florida. If you are tracking a tropical disturbance on the news and waiting for the local weather forecast to confirm a direct hit before purchasing or updating your property protection, you are already too late. The moment the National Hurricane Center (NHC) draws a formal tropical storm or hurricane watch or warning cone over any portion of the state, insurance carriers draw a regulatory line in the sand.

They instantly activate a binding moratorium, which completely locks down their computer networks. No insurance agent can legally issue a new policy, add windstorm coverage, or lower a deductible until the threat has completely cleared the state.

To achieve total visibility over your property's safety, you must realize that using weather forecasts as a financial planning tool is a catastrophic gamble. In the 2026 Florida insurance market, policies must be fully bound during blue skies—not when the outer bands of a storm are already swirling in the Atlantic or the Gulf.

1. The Real-Time Underwriting Lockout

When a storm approaches, property owners often panic-shop for coverage. To prevent this "imminent loss" surge, insurance carriers utilize the state-sanctioned moratorium mechanism.

- Instant Electronic Shutdown: The moratorium trigger is entirely automated. The second a county is placed under a watch or warning box, underwriting algorithms instantly freeze new business entries for that zone—and often statewide due to the unpredictable tracking nature of major storms.

- The 72-Hour Post-Storm Freeze: The lockout does not lift the moment the sun comes out. Moratoriums typically remain strictly enforced until 72 hours after all storm warnings are officially dropped by the state, giving field adjusters a window to evaluate widespread structural damage before the company assumes any new liabilities.

- The Claim Filing Countdown: Under updated 2026 property insurance rules, homeowners now have one year to file a windstorm claim (down from two years), while carriers are mandated to respond within 60 days. Because insurers are under tight, statutory timelines to pay out claims quickly, they are incredibly strict about locking out any unverified, last-minute risks before a storm hits.

2. The Collateral Damage: Real Estate Closings Interrupted

The "Red Line" doesn’t just affect homeowners trying to upgrade their current policies; it regularly destroys pending real estate transactions.

If you are buying a home in Stuart or anywhere along the Florida coast, your mortgage lender cannot legally fund your loan package without a fully verified, active hazard insurance binder on the closing table.

[Forecast Shows System] ──> [Moratorium Instantly Triggers] ──> [Insurance Binder Frozen] ──> [Mortgage Funding Pulled] ──> [Closing Contract Collapses]

The Lender Trap: If a storm forces a binding moratorium 24 hours before you sign your closing documents, your loan is frozen mid-air. This forced delay can push your closing past your contract's expiration date or blow right through a favorable interest rate lock, costing you thousands of dollars or costing you the house entirely.

3. The Deceptive "No-Fault" and Flood Delusions

Waiting for the forecast also leaves homeowners exposed to massive gaps between standard property policies and the realities of a tropical system:

- The 30-Day Flood Insurance Deadline: Standard homeowners insurance never covers flood damage or rising storm surge. If you scramble to buy a private or National Flood Insurance Program (NFIP) policy right before a storm hits, you are completely unprotected. Flood policies carry a mandatory 30-day waiting period before the coverage goes live.

- The Hurricane Deductible Shock: Even if your property coverage is active, a tropical storm is handled differently than a hurricane. Your massive 2% to 5% Hurricane Deductible only triggers if the NHC issues an official hurricane warning. If a storm hits your home as a severe tropical storm, your standard, lower "All Other Perils" (AOP) deductible applies, shifting the financial math dramatically.

4. Exploiting the Stabilizing 2026 Private Market

The tragedy of waiting for a storm forecast is that Florida's insurance market is currently in its healthiest, most competitive state in over a decade. Following successful lawsuit abuse reforms, capital has flooded back into the state.

At Walker Insurance Agency, we help homeowners step across the red line safely by utilizing the state's resurgent financial climate:

- The 20-Carrier Influx: With 20 brand-new private insurance companies approved to write property lines in Florida, there is zero reason to remain uninsured or underinsured. These new competitors are actively undercutting old rates to win clean profiles.

- The Citizens Rate Relief: The state's insurer of last resort, Citizens Property Insurance, introduced a statewide average 8.7% premium reduction, with private domestics like Security First (-8%) and Florida Peninsula (-8.2%) following suit. Lower pricing means securing a comprehensive shield before storm season is more affordable than it has been in fifteen years.

Why Working with an Independent Agency is Vital

Relying on an online web browser portal to protect your home when the weather patterns look unstable is incredibly high-risk. Automated corporate systems are built to reject complex risks when a storm is brewing. At Walker Insurance Agency, we track the weather maps and the OIR underwriting desks simultaneously to give you true, predictive visibility.

The Walker Advantage:

- Pre-Cone Binding Execution: We monitor tropical waves long before they ever get a name or a forecast cone. If a system shows development potential, we fast-track our clients' pending applications to bind coverage days before a moratorium can freeze the system.

- MSFH Credit Integration: We match your home's structural components with active My Safe Florida Home (MSFH) wind-mitigation credits, ensuring your new roof-to-wall attachments or impact openings legally force your carrier to slash your premium by an average of $981 per year.

- Private Flood Alignment: We build a dual-layer defensive wall, ensuring your baseline homeowners coverage and your separate flood insurance timelines are perfectly synchronized to avoid seasonal traps.

FAQ

1. Can my insurance company cancel my active policy while a storm is spinning in the Atlantic?

No. Under Florida Office of Insurance Regulation emergency mandates, insurance companies are completely prohibited from canceling or non-renewing active property policies during a state-declared emergency or while a tropical storm threat is active. Your current coverage is legally extended until the danger passes.

2. What parts of my policy are frozen during a tropical storm moratorium?

A moratorium blocks all changes to your risk profile. You cannot purchase a new policy, you cannot add optional comprehensive endorsements, you cannot increase your Coverage A (Dwelling) replacement limits, and you cannot lower your personal deductibles.

3. Does the new 2026 roof law protect me during a storm?

Under HB 815, Florida insurers can no longer refuse to renew your policy solely because of the chronological age of your roof without looking at its actual physical condition. However, this consumer protection only helps you during standard renewal cycles—it will not help you get a new policy if a storm moratorium is already active.

Beat the Radar and Lock in Your Protection Today

The 2026 tropical tracking season is underway, and gambling your life savings on a shifting weather forecast is an unnecessary risk. With Florida's property market finally dropping prices and introducing real private competition, the time to secure your financial safety net is right now under blue skies.

Step across the red line safely. Contact Walker Insurance Agency today for a comprehensive property rate audit. We provide the visibility you need to lock in competitive premiums with Florida's newest carriers, protect your real estate closings, and shield your family from seasonal storm traps in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your home today.

Related Articles

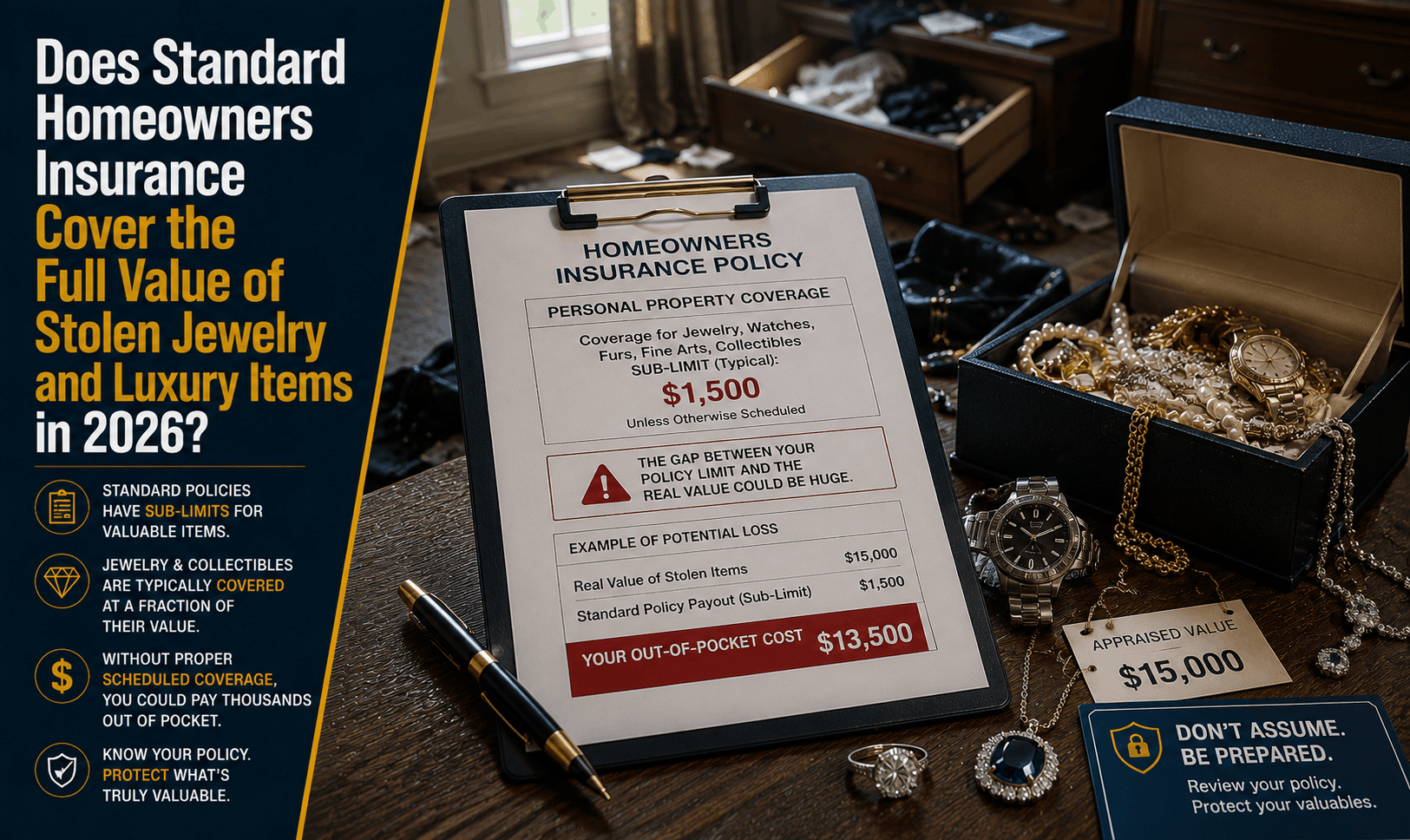

Does Homeowners Insurance Cover Stolen Jewelry & Luxury Goods? (2026)

Had luxury watches or jewelry stolen? Learn why standard homeowners insurance caps theft payouts at $1,500 and how to fully insure your high-value items.

Read More →

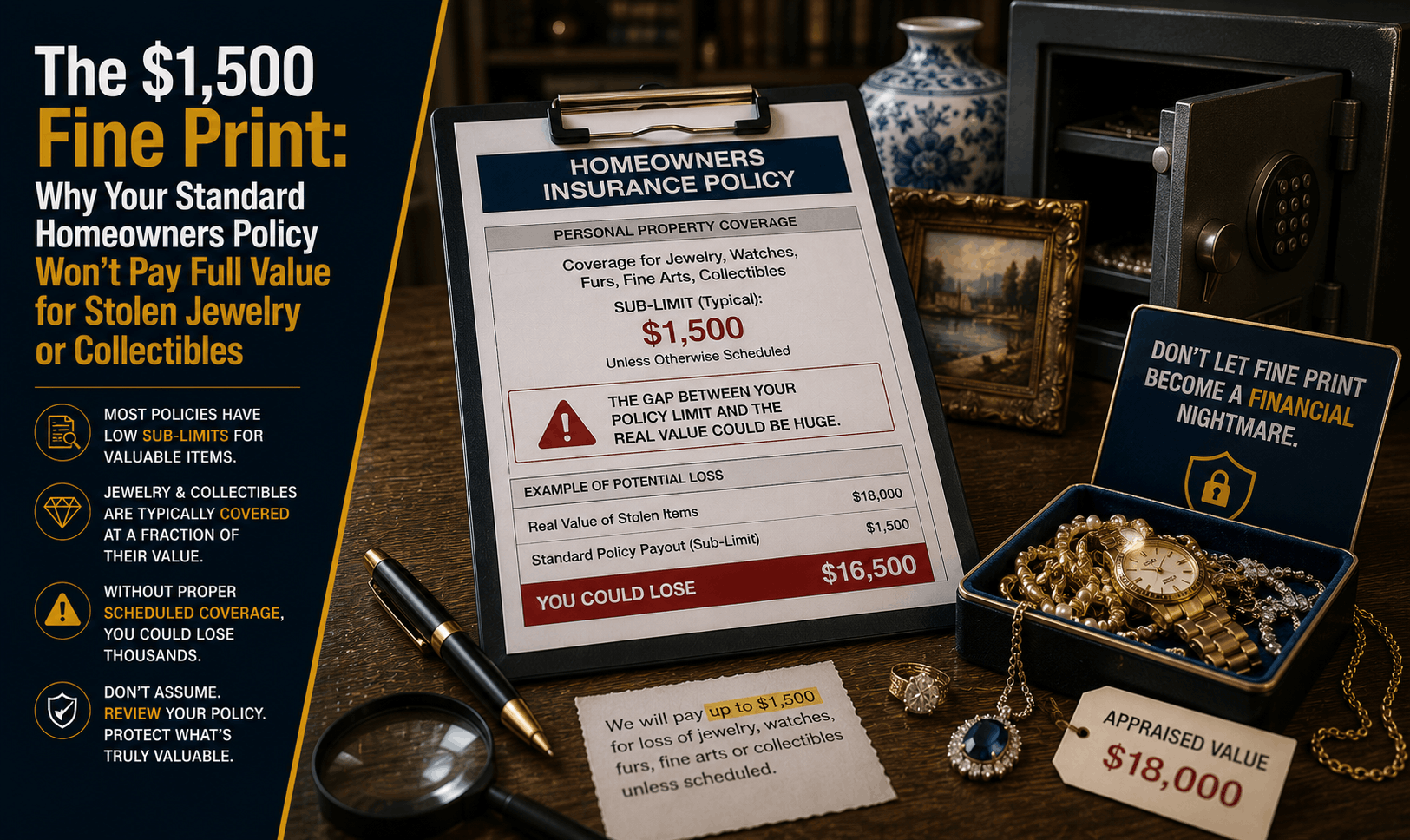

Does Home Insurance Cover Stolen Jewelry & Collectibles? (2026)

Had jewelry or valuables stolen? Discover why standard homeowners insurance limits theft payouts to $1,500 and how to fully insure your high-value items.

Read More →

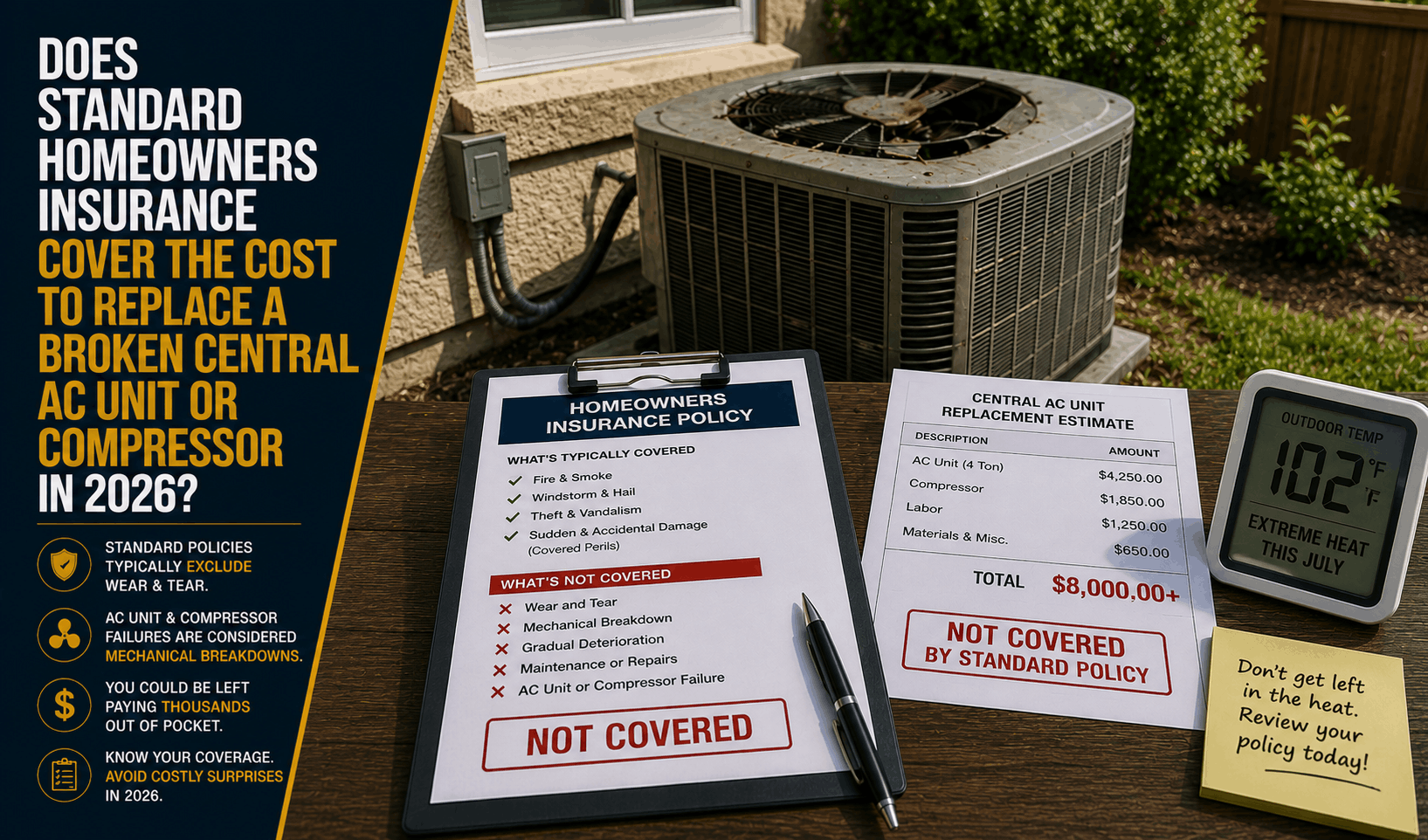

Does Homeowners Insurance Cover Broken AC Units? (2026)

AC broken in the summer heat? Learn why standard homeowners insurance won't pay to replace a broken central AC unit or compressor due to mechanical wear.

Read More →