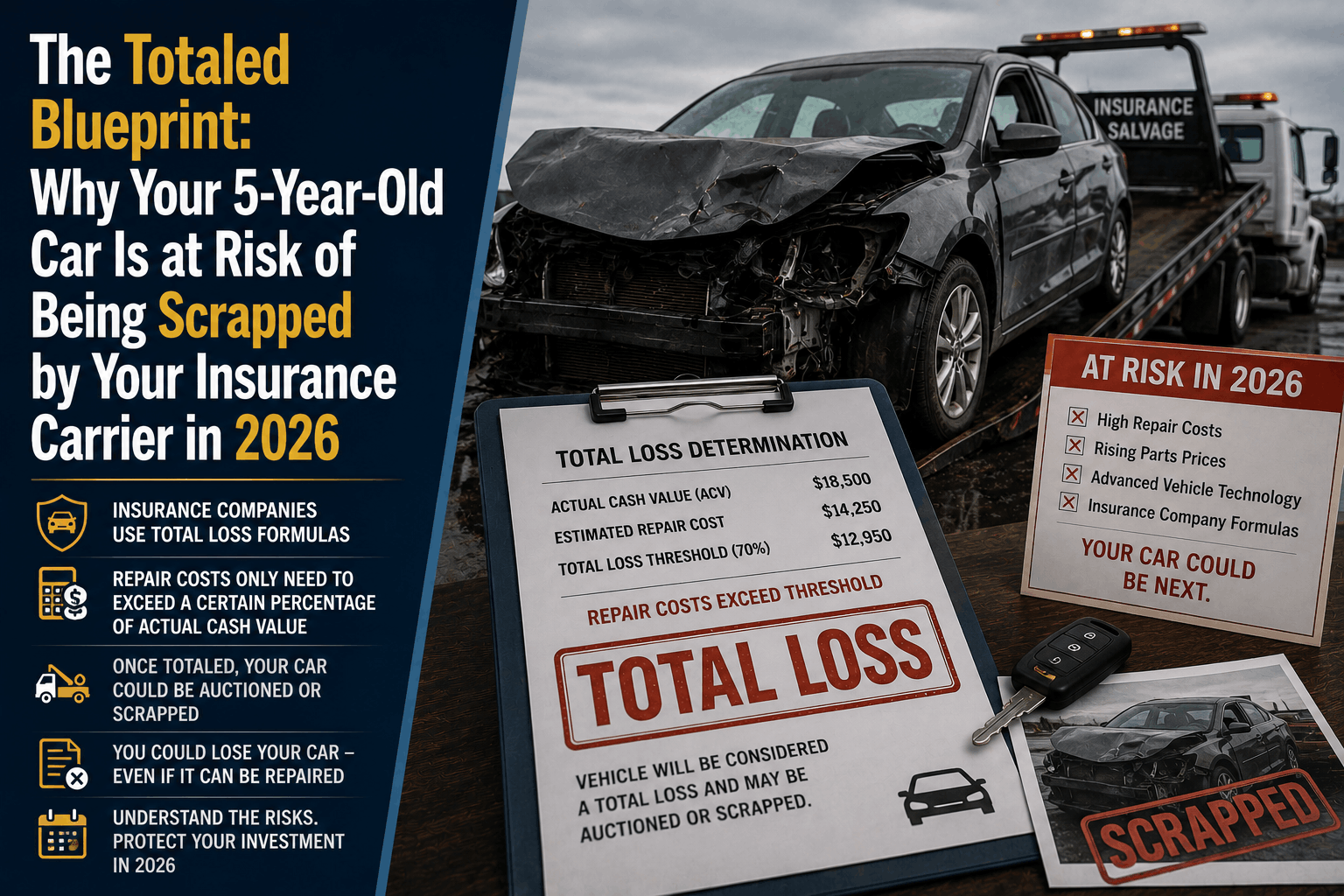

The Totaled Blueprint: Why Insurers Are Scrapping 5-Year-Old Cars in 2026

The Totaled Blueprint: Why Your 5-Year-Old Car Is at Risk of Being Scrapped by Your Insurance Carrier in 2026

The Direct Answer: Your visually "fixable" 5-year-old vehicle is at a higher risk of being written off and sent to a salvage yard today than at any other point in automotive history. According to the 2026 CCC Crash Course Annual Report, auto insurance total loss frequency has climbed to a record-breaking 23.1% of all claims. This means nearly one out of every four accidents now results in a vehicle being scrapped.

The "Totaled Blueprint" is a structural shift where insurance carriers choose to write off borderline vehicles early rather than pay for hyper-inflated, tech-heavy repairs.

For a typical 2021 model-year vehicle, standard chronological depreciation has naturally lowered its market valuation, yet the cost of the replacement parts and safety calibrations needed to fix it remain at peak retail pricing. If you experience a moderate fender bender, your insurer's automated mathematical formula will likely declare your car a total loss—even if the engine runs perfectly and the airbags never deployed.

1. The Tech Trap: Why a Bumper Is No Longer Just a Bumper

Five years ago, a minor rear-end collision required a basic plastic bumper replacement and a fresh coat of paint. Today, that exact same impact destroys an intricate web of hidden digital infrastructure.

According to 2026 collision industry data, over 28% of all repair estimates now explicitly require complex digital safety calibrations.

Modern 5-year-old vehicles are packed with Advanced Driver Assistance Systems (ADAS). Tucked directly behind your car's body panels are delicate ultrasonic sensors, blind-spot radar modules, rear-view cameras, and proximity glass.

[Minor Rear-End Collision]

│

├──\> Physical Bumper & Paint: $1,200

├──\> Replace 2 Blind-Spot Radar Sensors: $1,800

└──\> Mandatory OEM Software Calibration: $950

\==============================================

\= Total 2026 Repair Severity: $3,950 (Borderline Total Loss)

The Calibration Squeeze: A regular body shop cannot simply bolt a new bumper onto a modern chassis. Technicians must use specialized scan tools to recalibrate the vehicle's computer system so the safety features function accurately. These mandatory software setups regularly add thousands of dollars to standard physical repair bills, instantly blowing past insurance thresholds.

2. The Arbitrage Loophole: Healthy Salvage Returns

The second factor driving the 2026 total loss surge has nothing to do with the damage to your car, and everything to do with what your damaged car is worth to international scrap buyers.

Automotive data providers like Mitchell confirm that global salvage returns for the insurance industry are extremely healthy. Because there is an ongoing shortage of raw materials and affordable used vehicle components, salvage yards and overseas recycling operations are paying top dollar for wrecked vehicles.

- The Total Loss Formula (TLF): In states like California, Arizona, and Georgia, insurers do not wait for repair bills to equal the car's full value. They use a strict algebraic formula:

$$\text{Estimated Repair Costs} + \text{Actual Salvage Value} \ge \text{Actual Cash Value (ACV)}$$

If your 5-year-old crossover has an ACV of $18,000, requires $10,000 in advanced repairs, and a salvage yard bids $8,500 for the wreck, your vehicle is mathematically totaled. Because $\$10,000 + \$8,500 = \$18,500$ (which exceeds the car's $18,000$ value), the carrier will immediately scrap the vehicle, cut you a check, and flip the chassis to a salvage yard to recoup their cash.

3. How the "Total Loss Threshold" Varies Across State Lines

If you do not live in a state that utilizes the Total Loss Formula, your carrier must follow a rigid, state-mandated percentage threshold. The map is heavily divided, meaning an identical accident can lead to a repair in one town and a total write-off just across the state line:

| State Regulatory Framework | Statutory Total Loss Threshold | What Happens to a $20,000 Vehicle |

|---|---|---|

| Oklahoma | 60% of ACV | Totaled automatically at $12,000 in estimated damage. |

| Arkansas / Iowa | 70% of ACV | Totaled automatically at $14,000 in estimated damage. |

| Florida / Alabama | 75% of ACV | Totaled automatically at $15,000 in estimated damage. |

| Nevada / Kentucky | 80% of ACV | Totaled automatically at $16,000 in estimated damage. |

| Texas / Colorado | 100% of ACV | Repaired up to the full value; Totaled only at $20,000+. |

How to Insulate Your Wallet from a Forced Write-Off

If you are driving a paid-off 5-year-old vehicle to avoid a monthly car payment, a sudden total loss determination can disrupt your household budget. At Walker Insurance Agency, we advise clients to manage this underwriting trend using a three-tier protection framework:

- Secure New Car Replacement / Vehicle Value Riders: If you purchase a high-quality used vehicle that is a few years old, ask your independent agent about adding specialized valuation endorsements that pay out a fixed percentage above standard book depreciation if the vehicle is written off.

- Maintain Comprehensive Up-to-Date Records: If your vehicle is involved in an accident, do not let the insurance adjuster rely strictly on localized baseline software to determine your Actual Cash Value. Provide a clean portfolio of recent tire receipts, major mechanical service records, and high-resolution photos to force a higher valuation floor.

- The Owner-Retained Salvage Option: If your car is declared a total loss but remains structurally safe and drivable (such as a hail damage claim or cosmetic panel scrapes), you can request an "owner-retained" settlement. The carrier will cut you a check for your vehicle's value minus its estimated scrap value, allowing you to keep the car and drive it on a rebuilt title.

Why Working with an Independent Agency is Vital

Managing an auto claim through an automated smartphone application ensures your vehicle will be evaluated by an algorithm designed to minimize corporate risk. At Walker Insurance Agency, we provide the personalized visibility you need to navigate complex total loss evaluations.

The Walker Advantage:

- Independent Valuation Auditing: We review the carrier’s initial valuation reports line-by-line to ensure they are using accurate, high-tier comparable vehicles in your exact zip code.

- Deductible Structure Balancing: We help you structure your comprehensive and collision deductibles to ensure you receive a maximum net settlement check if your vehicle hits a total loss threshold.

- Cross-Market Portability: As baseline auto premium rates stabilize across Florida, we continuously shop your profile to place your vehicles with carriers known for transparent, consumer-first claims processing in Stuart.

FAQ

1. What happens if my car is totaled but I owe more on my auto loan than the insurance check provides?

This is a common financial trap known as being "underwater" on a loan. Because standard full-coverage policies only pay out the vehicle's depreciated Actual Cash Value right before the crash, you are personally responsible for paying off the remaining loan balance to your bank. To avoid this out-of-pocket disaster, you should always verify that you have active Gap Insurance tied to your financed vehicles.

2. Can I dispute an insurance adjuster's decision to total my car?

Yes. You have the legal right to challenge a total loss determination. You can accomplish this by submitting independent repair estimates from an authorized specialist shop, providing verified maintenance records, or invoking the "Appraisal Clause" inside your policy contract, which permits a neutral third-party umpire to establish a final binding valuation.

3. Why do insurers total cars even if the estimated repair cost is slightly below the state threshold?

Insurers apply an internal buffer because they recognize that visual field inspections are inherently superficial. Once a collision technician tears down a vehicle's body panels, hidden structural framework cracks or secondary electrical wire harness damages are almost always uncovered, driving up the final bill.

Take Control of Your Asset Protection Today

Your 5-year-old vehicle is a valuable piece of personal property, but in the modern high-tech collision environment, your insurance company views it strictly as a line-item math equation. Protecting your household wealth requires shifting away from autopilot renewals and understanding the true mechanics of your coverage.

Get an expert policy analysis today. Contact Walker Insurance Agency for a comprehensive 2026 coverage audit. We provide the visibility you need to eliminate hidden valuation gaps, align your deductibles safely, and lock in the most secure premium protections available in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your asset today.

Related Articles

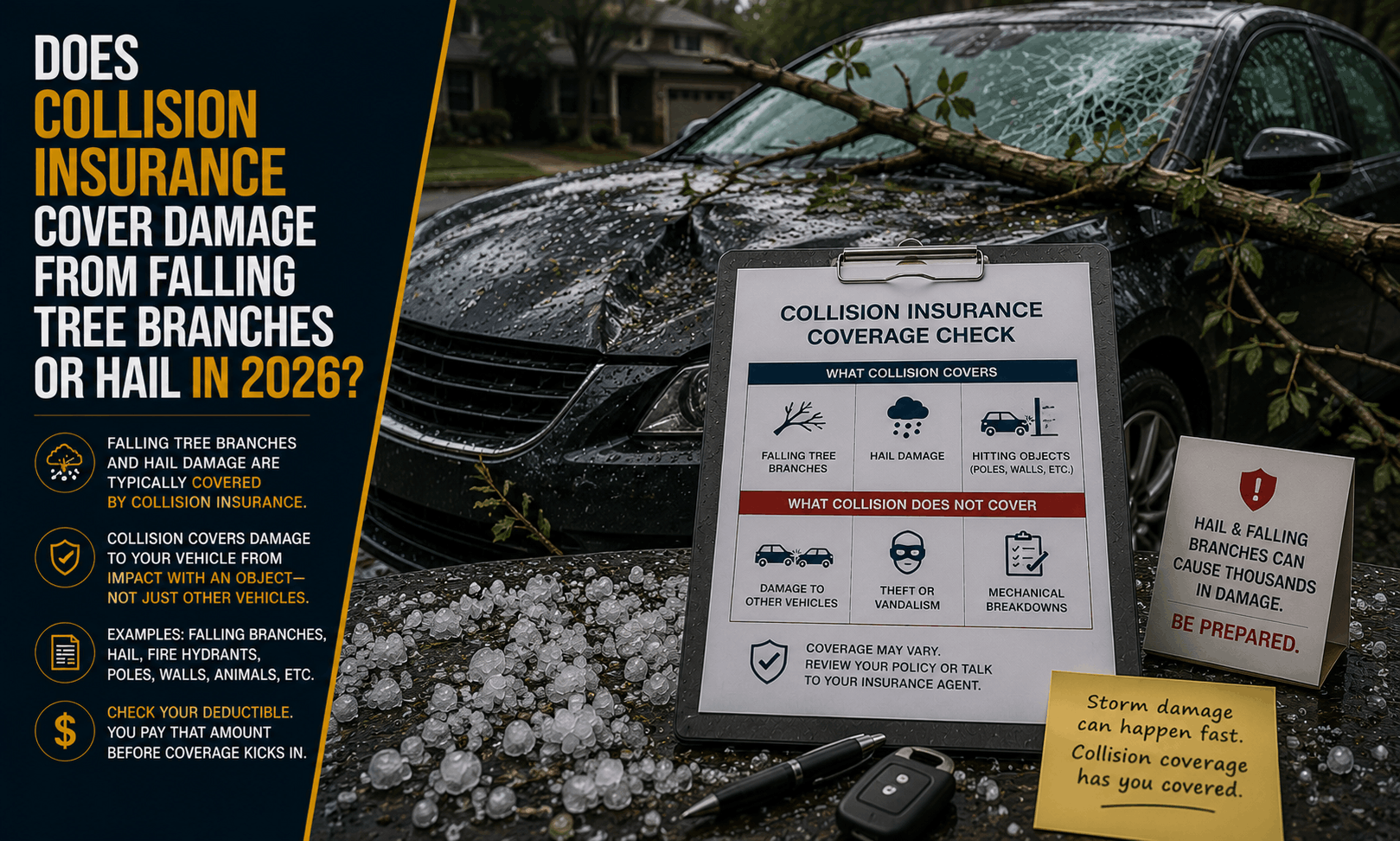

Does Collision Insurance Cover Hail & Tree Damage in 2026?

Did hail or a falling tree branch damage your car? Learn why collision auto insurance won't pay for storm damage and how comprehensive coverage protects you.

Read More →

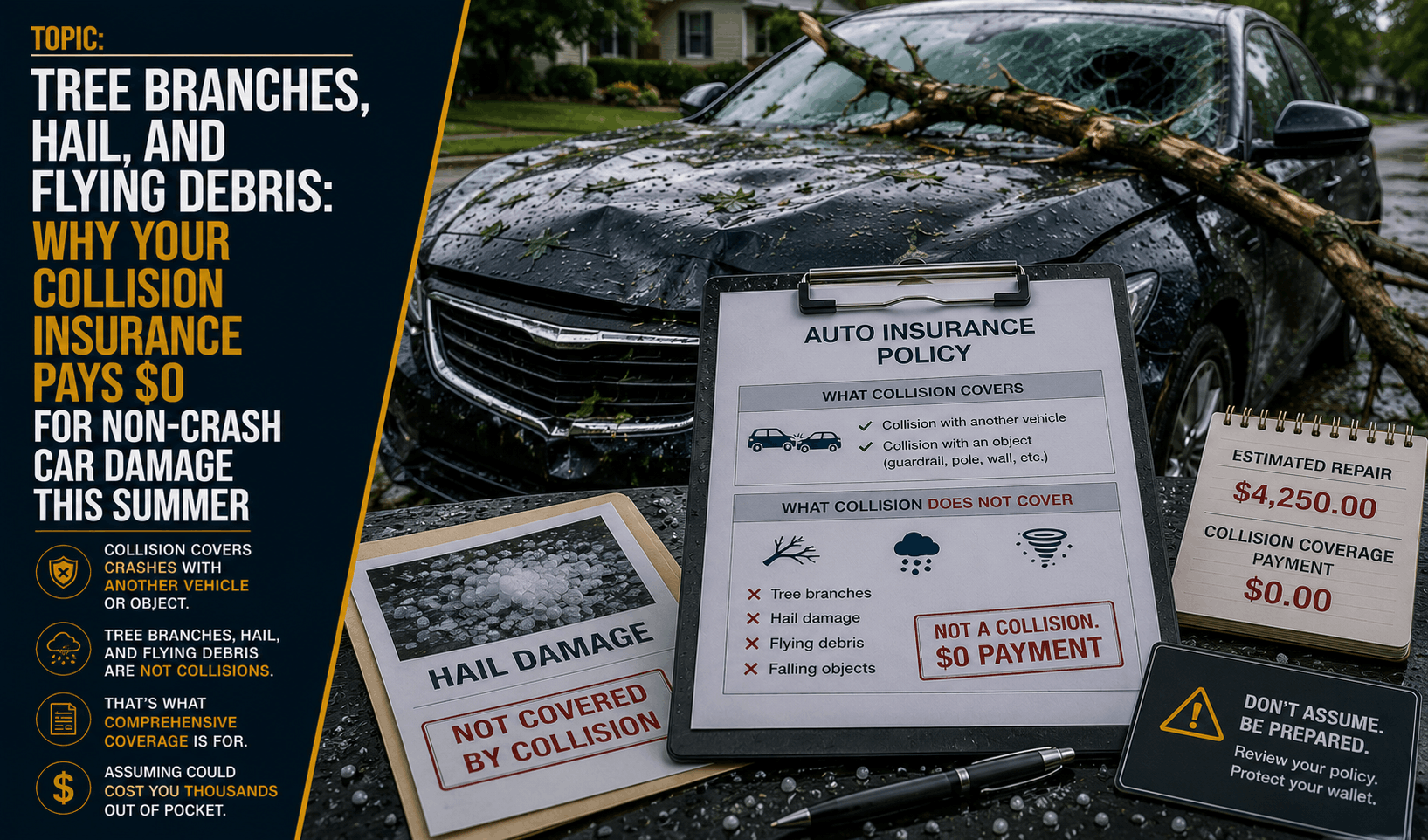

Why Collision Insurance Pays $0 for Non-Crash Summer Damage (2026)

Did a tree branch, hail storm, or flying road debris hit your car this summer? Discover why collision auto insurance pays $0 and how comprehensive coverage protects you.

Read More →

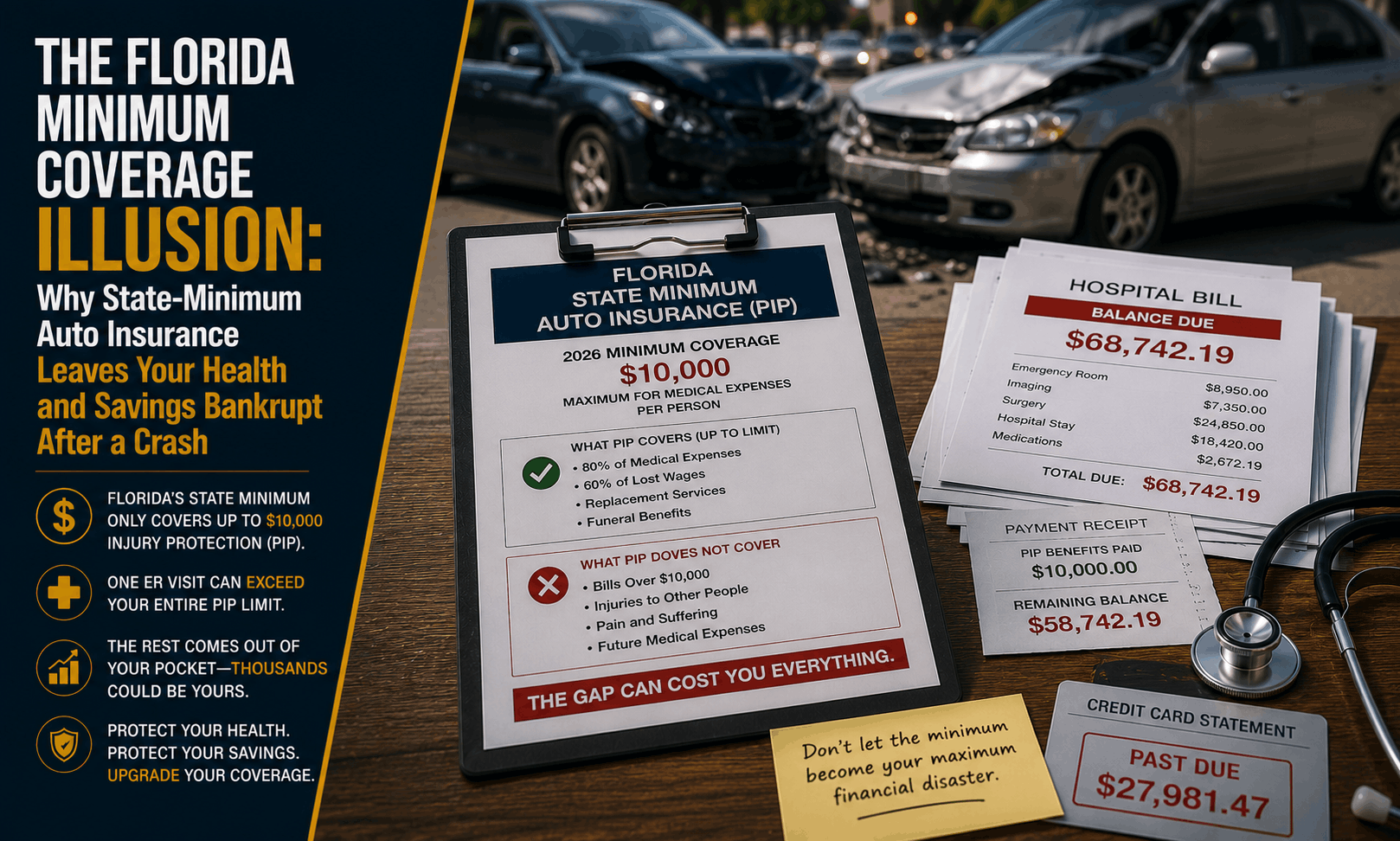

Florida Minimum Auto Insurance Coverage Illusion (2026)

Driving with state-minimum auto insurance in Florida? Learn why carrying only PIP and PDL leaves your health and personal savings vulnerable after a crash.

Read More →