What Happens If Your Used Car Is Totaled by Insurance in 2026?

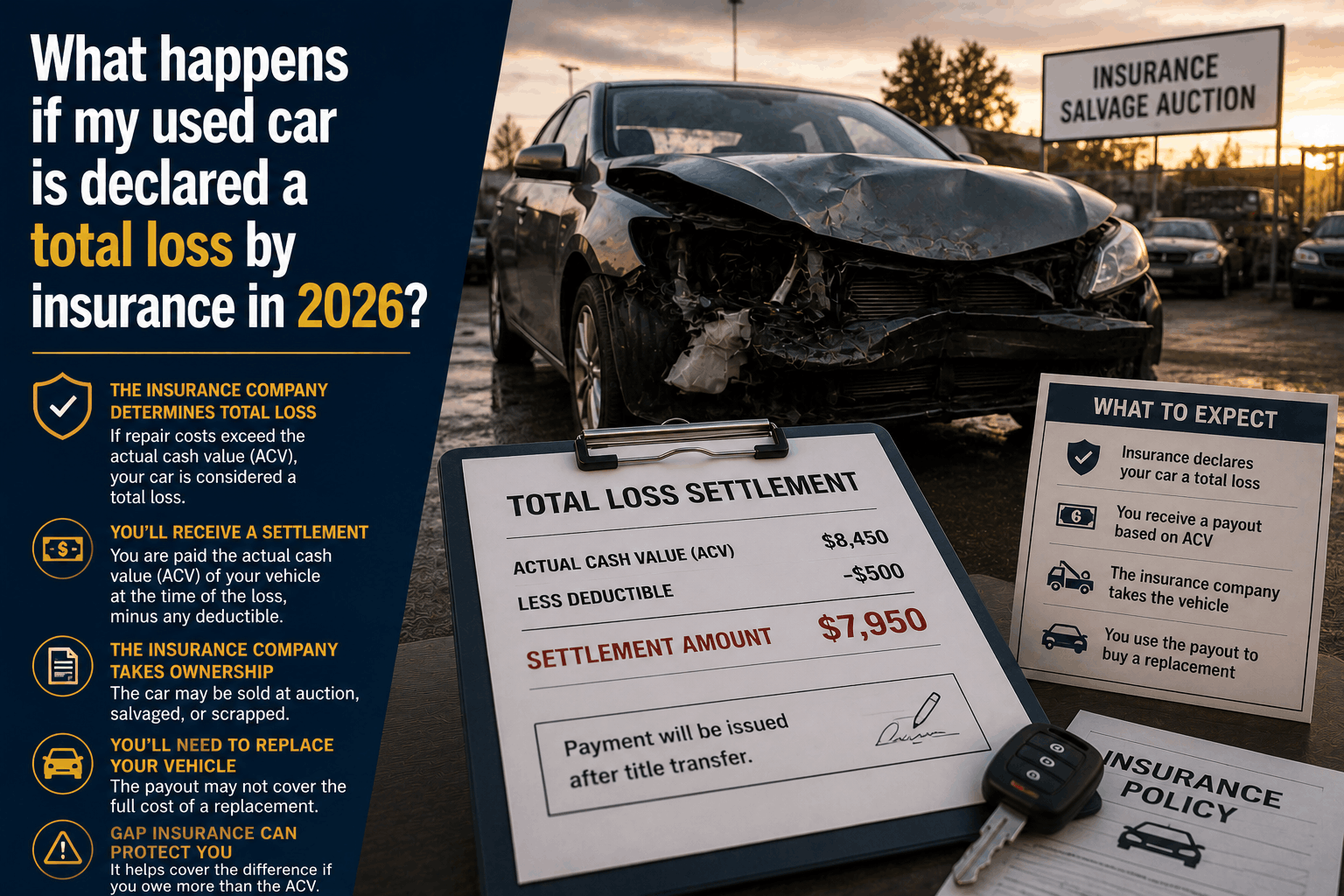

What Happens If My Used Car Is Declared a Total Loss by Insurance in 2026?

The Direct Answer: When an insurance company declares your used car a total loss, it contractually means the carrier has determined that repairing the vehicle is no longer economically viable. Under the hood of this decision is a strict numbers game: the insurer will write a settlement check for your car's pre-crash retail worth—known as its Actual Cash Value (ACV)—minus your comprehensive or collision deductible, and take ownership of the vehicle to sell it at a salvage auction.

Appraisal Engine

In 2026, this scenario is unfolding at an unprecedented rate. According to the 2026 CCC Crash Course Annual Report, total loss frequency has climbed to an all-time industry high of 23.1% of all claims.

CCC Intelligent Solutions

To achieve total visibility over your financial recovery, you must realize that a total loss determination is not a negotiation unless you make it one. If you blindly accept the insurance company’s initial computerized valuation, you are highly likely to leave thousands of dollars on the table.

Appraisal Engine

1. The Step-by-Step Total Loss Process

The moment the collision shop submits a teardown report to your insurer, your claim shifts from a standard repair path into a strict administrative pipeline:

1

The Threshold Calculation

Immediate Execution

**1.The Threshold Calculation:**Immediate Execution.

The adjuster compares the repair estimate against your car’s market value. In states like Florida, if repairs hit 75% of the ACV, the car is legally totaled. In other states, they use the Total Loss Formula: Repair Costs+Salvage Value≥ACV.

2

The CCC Valuation Report

Takes 24–48 Hours

**2.The CCC Valuation Report:**Takes 24–48 Hours.

The insurer uses localized database software (usually CCC Intelligent Solutions) to generate a market valuation report based on recent sales of matching used cars in your exact zip code.

3

Lender Notification

Critical for Financed Cars

**3.Lender Notification:**Critical for Financed Cars.

If you carry a car loan, the insurer legally contacts your lienholder. By law, the insurance settlement check must pay off your remaining bank loan balance first.

4

Vehicle Release & Cleanup

Complete Within 3 Days

**4.Vehicle Release & Cleanup:**Complete Within 3 Days.

You must clean out all personal items, remove the license plates, and sign over the vehicle title. The carrier then schedules a flatbed tow to clear the vehicle out of the body shop to halt daily storage fees.

5

The Final Settlement Disbursal

Final Step

**5.The Final Settlement Disbursal:**Final Step.

The insurer issues the funds. If the check is larger than your loan, you get the net difference. If you own the car outright, the full check (minus your deductible) is sent directly to your bank account.

2. Why Are More Used Cars Being Scrapped This Year?

If your car looks entirely repairable, you might feel blindsided by a total loss letter. In the 2026 automotive climate, two massive structural shifts are forcing insurers to scrap used vehicles early rather than fix them:

- The Calibration Squeeze: Modern vehicles are packed with Advanced Driver Assistance Systems (ADAS). Over 28.3% of all 2026 repair estimates now require mandatory digital software calibrations. Tucked behind ordinary plastic bumpers are complex radar sensors and cameras. Replacing these components requires specialized diagnostic tools that add thousands of dollars to standard body work, easily pushing vehicle claims past total loss thresholds.

S&P Global+ 1 - The Salvage Premium: Because there is an ongoing global shortage of raw automotive materials and affordable used components, third-party recycling operations and salvage yards are paying top dollar for wrecks. If an insurer can cut you an ACV check and immediately claw back a massive chunk of that cash by flipping your vehicle to a salvage buyer, it becomes mathematically cheaper for them to scrap your car than to fund an open-ended repair bill.

3. How to Fight an Undervalued Insurance Offer

The baseline valuation report the insurance company hands you is a starting offer, not a final mandate. Adjusters routinely use inaccurate baseline data to lower their initial payouts. To protect your wealth, use this active stacking framework:

Appraisal Engine

[Audit the Comp Report for Wrong Trim/Options]

\+

[Submit Receipts for Tires & Major Maintenance (<12 months)]

\+

[Provide 3 Local Dealer Quotes for Identical Cars]

============================================================

= Legally Forced Actual Cash Value (ACV) Increase

The Appraisal Clause Weapon: If you and your carrier completely deadlock on what your used car is worth, read your insurance policy jacket. You have the contractual right to invoke the Appraisal Clause. This triggers an independent dispute process where you hire your own appraiser, the insurer hires theirs, and a neutral umpire steps in to establish a final, binding payout figure.

4. The Financed Car Trap: Surviving a Loan Gap

If your used car is totaled while you are still making monthly payments, a severe financial gap can emerge. Because standard physical damage insurance only pays out the depreciated market value of the car right before the crash, you can easily end up in an "underwater" loan scenario:

- The Math: If your vehicle's 2026 market value is determined to be $14,000, but your remaining bank loan statement reads $17,500, the insurance company will send the full $14,000 to your lender and close the file.

- The Bill: You are personally, legally responsible for paying the remaining $3,500 out of pocket to your bank to close out the loan contract. To insulate your family from this disaster, you should always ensure your auto policy carries active Gap Insurance from the day you sign your financing paperwork.

Why Working with an Independent Agency is Vital

When a major collision turns your daily driver into a total loss mathematical equation, handling the claims process through a faceless corporate app leaves thousands of dollars on the table. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to maximize your settlement.

The Walker Advantage:

- Valuation Review Auditing: We review the carrier’s localized market reports line-by-line to ensure they aren't using stripped-down baseline models to undervalue your premium trim package.

- Gap Integration Verification: We ensure your loan gap structures or vehicle replacement endorsements drop into the claims timeline seamlessly, preventing unexpected debt collectors from hitting your credit.

- Post-Total Portability Optimization: Since data shows over 40% of drivers switch companies after a total loss due to poor service, we immediately shop the stabilizing 2026 Florida market to seamlessly move your profile to a higher-rated, lower-cost private carrier in Stuart.

FAQ

1. Can I choose to keep my used car after it is declared a total loss? Yes. This is called Owner-Retained Salvage. If the car is structurally safe and drivable (such as experiencing heavy cosmetic hail dents), you can ask the insurer to let you keep the vehicle. The carrier will calculate your settlement check, subtract your deductible, and subtract the exact dollar amount the salvage yard bid for the wreck. You keep the car, receive a smaller check, and must register the vehicle under a state "rebuilt" title.

2. Does my deductible still apply if the accident wasn't my fault? If you file the total loss claim through your own collision coverage, your insurer will subtract your deductible from your final payout check. However, once your insurance company successfully uses subrogation to claw back the funds from the at-fault driver's carrier, they are legally required to refund that deductible amount back to you.

3. What happens to my auto insurance policy after my car is totaled? Your policy does not automatically vanish. Your independent agent must formally remove the totaled vehicle's identification number (VIN) from your coverage lines. You can choose to pause the policy under a "wavelock" state to preserve your continuous insurance history credits, or seamlessly transfer the active policy lines over to your replacement vehicle.

Don't Let the Insurance Algorithm Minimize Your Payout

A total loss determination can throw your household budget into chaos, but knowing your statutory rights stops an insurance company from treating your asset like an ordinary line-item deduction. In the complex modern auto market, maximizing your settlement requires professional execution.

Expose your true policy protections today. Contact Walker Insurance Agency for a comprehensive coverage and valuation review. We provide the visibility you need to navigate total loss claims safely, secure every available vehicle credit, and lock in the most competitive asset protections available in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us protect your financial recovery today.

Related Articles

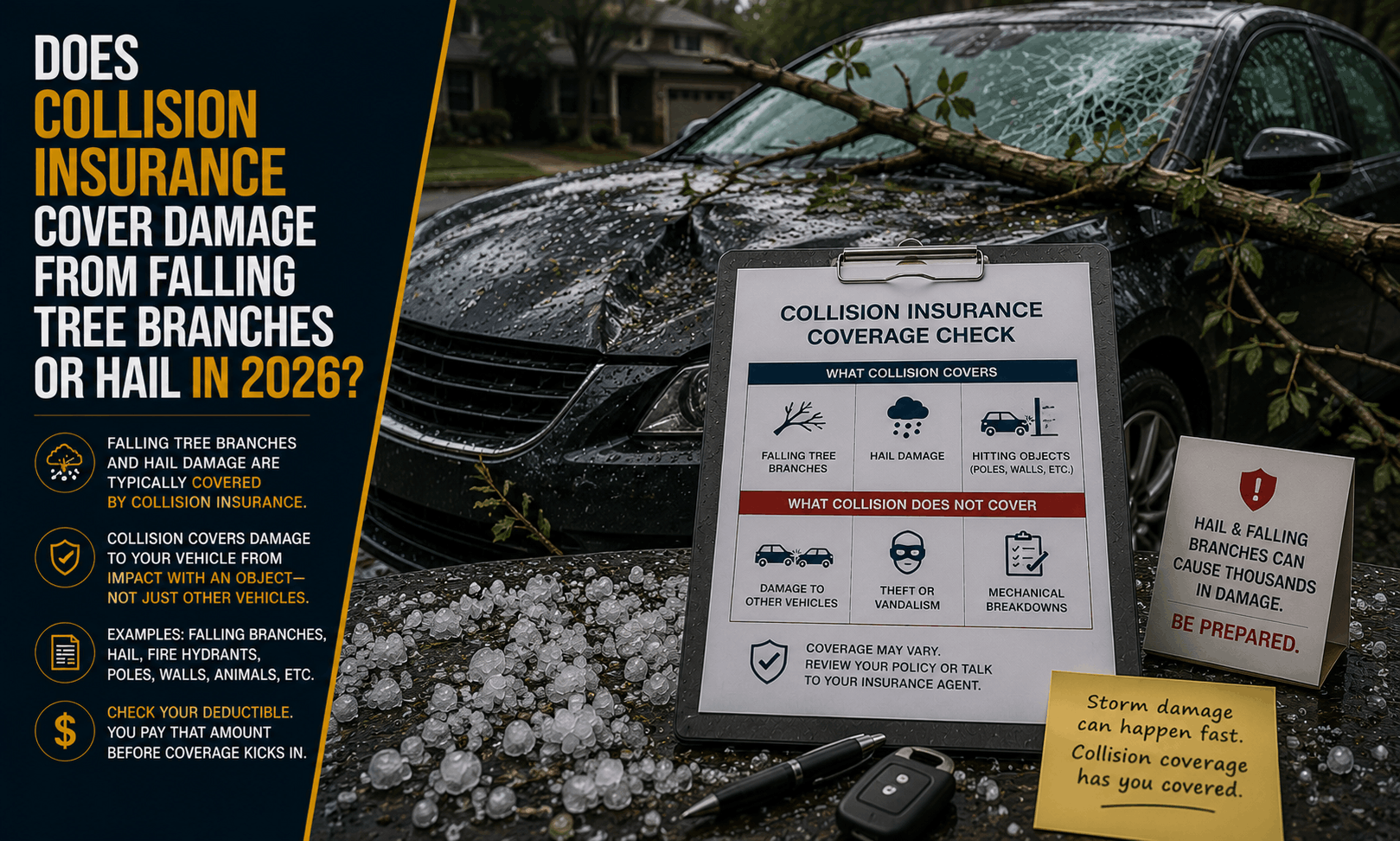

Does Collision Insurance Cover Hail & Tree Damage in 2026?

Did hail or a falling tree branch damage your car? Learn why collision auto insurance won't pay for storm damage and how comprehensive coverage protects you.

Read More →

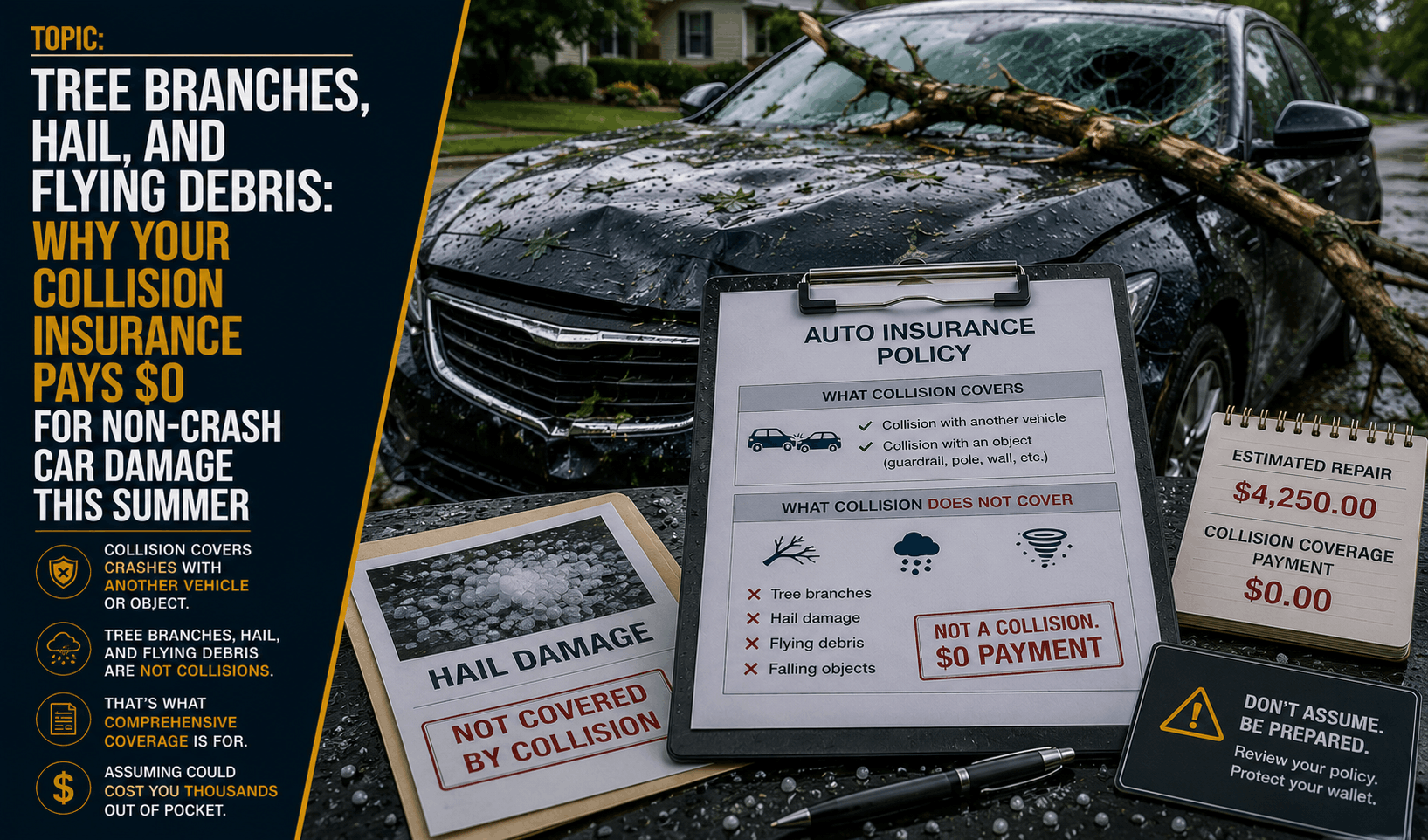

Why Collision Insurance Pays $0 for Non-Crash Summer Damage (2026)

Did a tree branch, hail storm, or flying road debris hit your car this summer? Discover why collision auto insurance pays $0 and how comprehensive coverage protects you.

Read More →

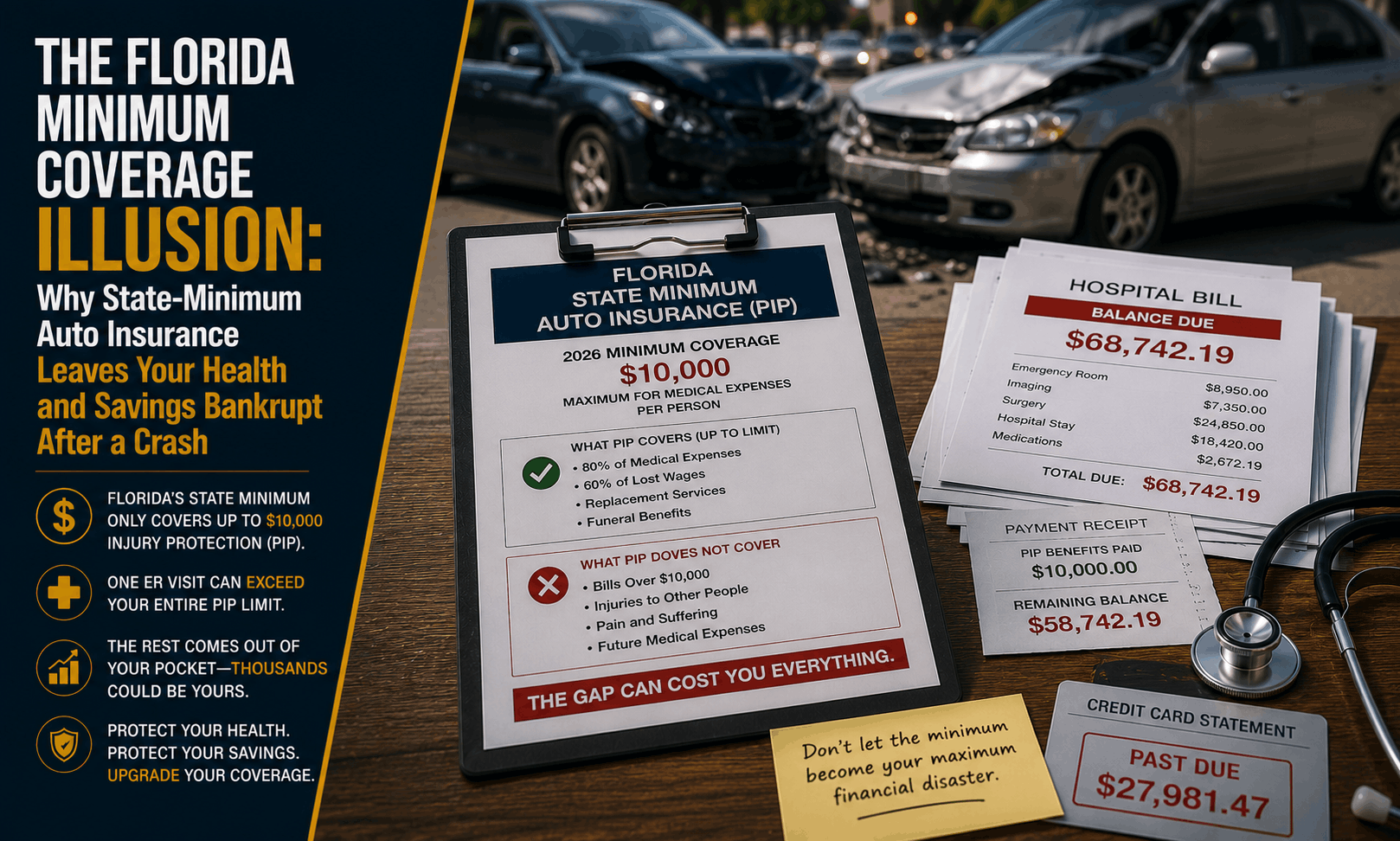

Florida Minimum Auto Insurance Coverage Illusion (2026)

Driving with state-minimum auto insurance in Florida? Learn why carrying only PIP and PDL leaves your health and personal savings vulnerable after a crash.

Read More →