Can I File a Diminished Value Claim in 2026? (Not At-Fault Guide)

Can I File a Diminished Value Claim After a Car Accident That Wasn't My Fault in 2026?

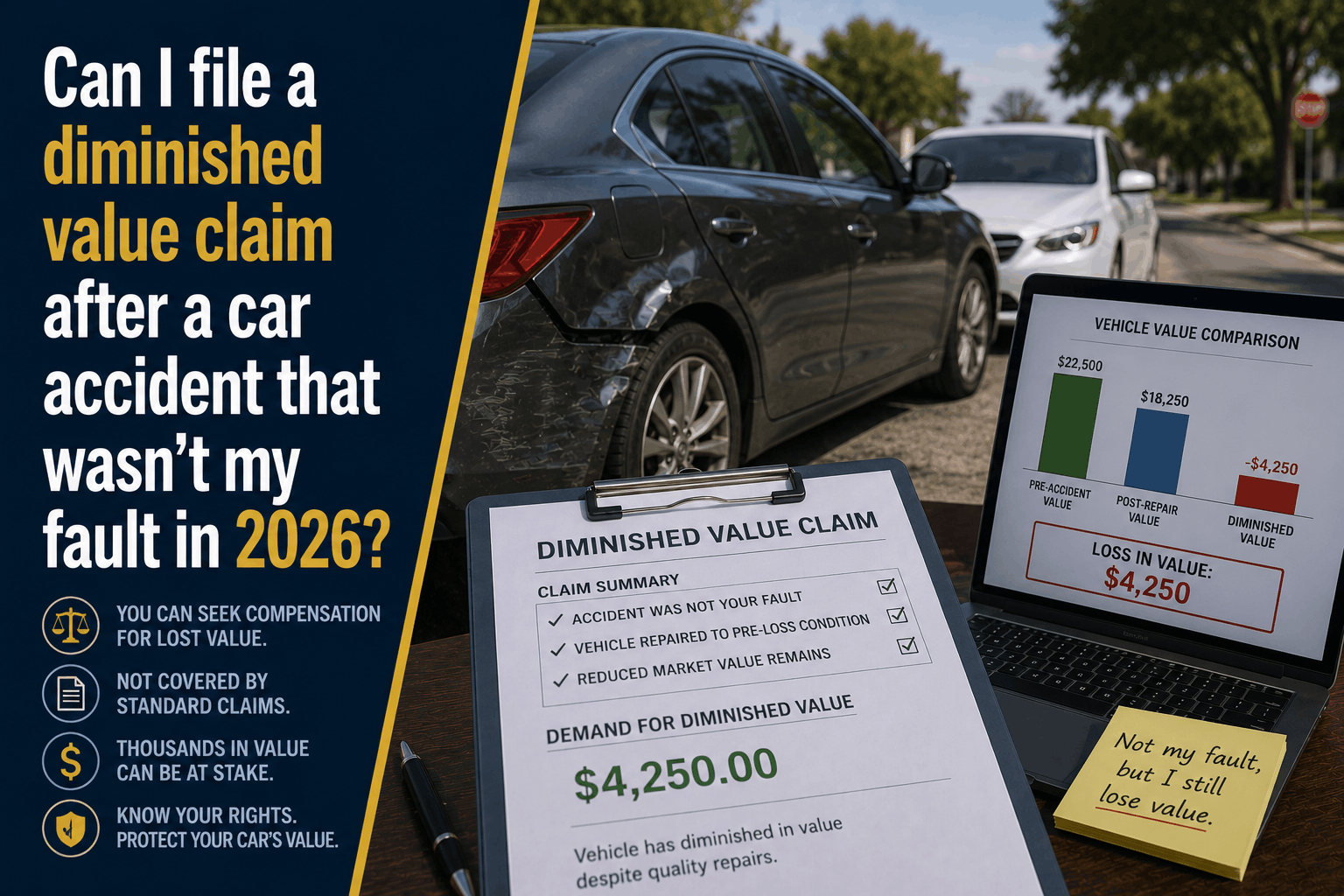

The Direct Answer: Yes, you can absolutely file a diminished value claim if the auto accident was not your fault. Legally, when another driver causes damage to your vehicle, their insurance company is required to make you "whole" again. Under tort law, this doesn't just mean paying the body shop bills to repair the physical sheet metal; it also means compensating you for the permanent loss in your vehicle's market resale value—known as Inherent Diminished Value.

In 2026, capturing this compensation is more critical than ever before. Because vehicle history databases like CARFAX and AutoCheck are now instantly synced with automated dealership appraisal software, an accident record attached to your Vehicle Identification Number (VIN) triggers an unnegotiable 10% to 30% drop in your car's market value.

To achieve total visibility over your automotive wealth, you must realize that even if the repair center does a flawless job using brand-new factory parts, your vehicle is worth thousands of dollars less than an identical model with a clean history.

1. The 3 Types of Diminished Value Claims

Before you contact the at-fault driver's insurance adjuster, you need to understand the precise legal classification of your claim:

- Inherent Diminished Value: This is the most common and widely successful claim type. It represents the loss in market value based strictly on the "history stigma." Buyers in the current used-car market will automatically demand a steep discount for a vehicle with a prior accident history, regardless of how pristine the repairs are under the lights.

- Repair-Related Diminished Value: This occurs if the body shop performs low-quality work—such as mismatched paint textures, uneven panel gaps, or leaving underlying structural frame rails warped. This represents additional financial loss on top of inherent depreciation.

- Immediate Diminished Value: This measures the drop in value directly following the crash before any repairs are actually executed. It is rarely used in standard consumer lines and is typically reserved for specialized commercial legal situations.

2. The Insurance Math: How Adjusters Calculate Your Loss

Insurance carriers do not volunteer this payout information, and when you request it, they will attempt to minimize the settlement check using a highly restrictive industry-standard formula known as Formula 17c.

Understanding how this matrix operates gives you the leverage to counter their initial metrics:

$$\text{Base Loss} = \text{Clean Retail Market Value} \times 10\% \text{ (The Standard Cap)}$$

Once the base loss is established, the adjuster applies two distinct downward fractional multipliers based on physical evidence:

The Damage Severity Modifier

- 1.00: Major structural framework or chassis damage

- 0.50: Moderate panel, air bag, and component damage

- 0.25: Minor cosmetic sheet metal or bumper cover damage

- 0.00: No structural or mechanical damage

The Mileage Modifier

- 1.00: 0 – 19,999 miles

- 0.80: 20,000 – 39,999 miles

- 0.60: 40,000 – 59,999 miles

- 0.40: 60,000 – 79,999 miles

- 0.20: 80,000 – 99,999 miles

- 0.00: 100,000+ miles

The Math in Action: If your clean 2024 commuter vehicle has a market value of $35,000, carries 15,000 miles, and suffered moderate side-impact damage, the base loss cap is $3,500. Applying the modifiers ($\$3,500 \times 0.50 \times 1.00$) yields a calculated diminished value baseline settlement of $1,750.

3. Step-by-Step Blueprint to Prove Your Claim

To win a third-party diminished value negotiation against an adversarial insurance company, you cannot rely on verbal opinions. You must build an ironclad evidentiary profile:

**1.Finalize the Physical Repair Files:**Teardown Records.

Wait until the body shop completely finishes the physical reconstruction. Request a full, itemized copy of the final insurance repair invoice detailing exactly which parts were swapped and whether any structural frame pulling occurred.

**2.Hire an Independent Appraiser:**Certified Appraisals.

Do not use generic online calculators. Pay for a certified, independent auto appraiser to inspect your vehicle post-repair. They will generate a formal Diminished Value Appraisal Report comparing your vehicle against local market historical sales.

**3.Secure Local Trade-In Quotes:**Dealer Evidence.

Take your repaired car to two separate local dealerships. Have them run a formal appraisal check and request a written statement confirming the exact dollar amount they are slashing from your trade-in value based strictly on the new CARFAX accident flag.

**4.Submit the Formal Demand Packet:**Demand Package.

Compile your repair bills, the independent appraisal report, and the dealer trade-in deductions. Submit them as a unified packet to the at-fault driver's insurance adjuster along with a formal demand letter requesting full financial restitution.

Why Working with an Independent Agency is Vital

Navigating an auto claim through a standard corporate smartphone application leaves your long-term equity completely exposed to hidden post-accident depreciation. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to defend your personal balance sheet.

The Walker Advantage:

- Claims Navigation Advocacy: We provide the precise, expert guidance required to gather documentation and structure your files to maximize your leverage against third-party carriers.

- Uninsured Property Alignment: We ensure your policy carries active Uninsured Motorist Property Damage (UMPD) lines, allowing you to file diminished value claims even if you are hit by a driver who carries no insurance or flees the scene.

- Strategic Portfolio Shopping: As the auto insurance market continues to stabilize, we continually shop your profile across top-tier private carriers, ensuring your assets maintain maximum liability thresholds at the lowest available rate floors in Stuart.

FAQ

1. Can I file a diminished value claim if the accident was my fault?

No, in almost all states. First-party diminished value claims (claims filed against your own collision policy) are explicitly barred by the standard contractual language written into personal auto policy jackets. You can only recover diminished value if a third-party driver hits your vehicle, allowing you to file against their active Property Damage Liability Coverage.

2. Is there a strict deadline or statute of limitations to file this claim?

Yes. Diminished value claims fall under state property damage statutes of limitations. For example, in Florida, you generally have up to two years from the exact calendar date of the motor vehicle accident to formally settle or file a lawsuit to recover lost equity from the at-fault party's insurer.

3. Does a leased vehicle qualify for a diminished value settlement?

No. Because you do not legally hold the vehicle's title, you do not absorb the financial loss caused by the history stigma. The leasing company (the bank holding the pink slip) absorbs the market value drop when the car is returned to the lot, meaning only the registered titleholder has the legal standing to pursue a claim.

Reclaim the True Value of Your Investment Today

Your automobile is one of the largest moving investments you own, but in the modern digital ecosystem, an accident history stamp is a financial penalty that can instantly wipe thousands of dollars off your personal balance sheet. Protecting your wealth requires shifting away from basic repair coverage and demanding the full economic restitution you are legally owed.

Don't leave your hard-earned equity in the insurance company's pockets. Contact Walker Insurance Agency today for a comprehensive asset and coverage review. We provide the visibility you need to navigate claims safely, counter unfair adjuster software metrics, and protect your lifestyle securely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your automotive equity today.

Related Articles

Does Home Insurance Cover Legal Fees & Lost Wages from Identity Theft? (2026)

Learn if standard home insurance covers legal fees and lost wages from identity theft in 2026, how endorsement sub-limits work, and how to get full fraud recovery.

Read More →

The Hidden Cost of Fraud: Does Home Insurance Cover Identity Theft? (2026)

Discover why standard homeowners insurance won't pay to restore a stolen identity in 2026, what hidden fraud costs you face, and how an Identity Theft Endorsement protects you.

Read More →

Does Water Backup Insurance Pay for a Hotel During Basement Sanitization? (2026)

Learn if water backup insurance pays for hotel stays while your basement is sanitized in 2026, how Loss of Use sub-limits work, and how to avoid out-of-pocket costs.

Read More →