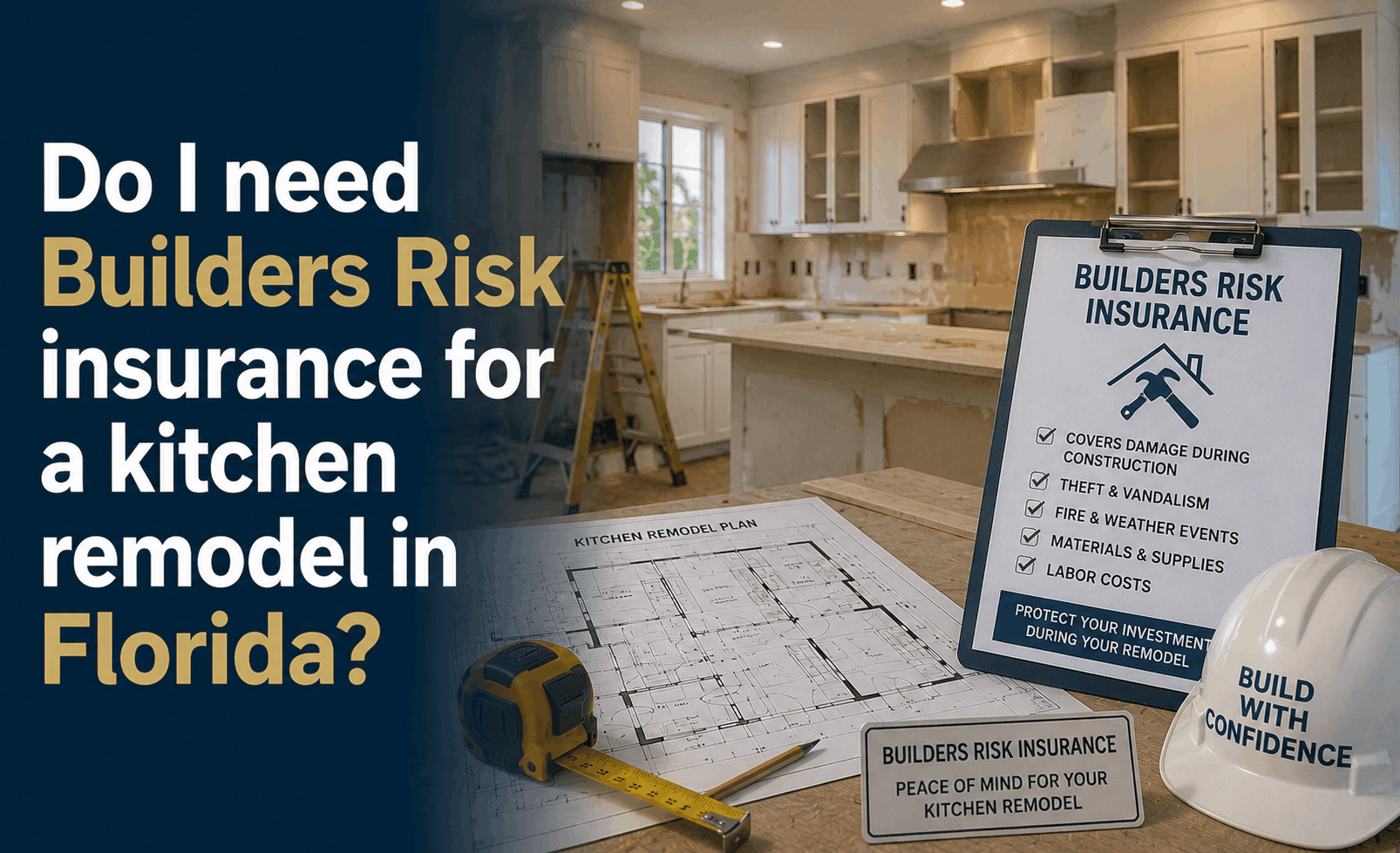

Do I Need Builder’s Risk Insurance for a Florida Kitchen Remodel? (2026)

Do I Need Builder’s Risk Insurance for a Kitchen Remodel in Florida?

The Direct Answer: For a minor cosmetic kitchen "refresh" in 2026, your standard Florida homeowners policy (HO-3) might be sufficient. However, if your remodel is a major overhaul—involving structural changes, moving plumbing/electrical, or costs exceeding $25,000—the answer is almost always yes. In 2026, Florida insurers have tightened "Renovation Clauses," often excluding theft of uninstalled materials (like those $15,000 custom cabinets sitting in your garage) and damage to the structure while it is "open" and vulnerable to Florida’s unpredictable weather.

To achieve total visibility over your project, you must distinguish between your contractor’s liability and your own property protection. A kitchen remodel is one of the most high-risk renovations due to the combined threat of water, fire, and expensive material theft.

1. The 2026 Cost Reality

In early 2026, a "medium" kitchen remodel in Florida averages between $30,000 and $65,000, with high-end projects easily exceeding $100,000.

- The Materials Risk: Luxury countertops and appliances are often delivered days or weeks before installation. Standard homeowners insurance typically does not cover building materials that are not yet "part of the structure."

- The "Open Structure" Hazard: If a wall is removed or the home is partially exposed during a 2026 storm, your HO-3 policy may deny water damage claims, citing that the home was not a "fully enclosed structure."

2. Builder’s Risk vs. Homeowners Insurance

While your HO-3 policy protects your finished home, Builder's Risk (also called Course of Construction insurance) is a temporary shield designed specifically for the chaos of a job site.

| Feature | Standard Homeowners (HO-3) | Builder’s Risk (COC) |

|---|---|---|

| Uninstalled Cabinets/Stone | Usually Excluded | Covered |

| Theft of Tools/Equipment | Excluded | Covered |

| Vandalism on Job Site | Often Excluded | Covered |

| Partial Structure Collapse | Excluded | Covered |

| Debris Removal | Limited (5%) | Higher Limits (Up to $50k) |

3. When is it "Non-Negotiable"?

At Walker Insurance Agency, we recommend a Builder’s Risk policy for your kitchen remodel if:

- You Move Out: If the kitchen is gutted and you are living elsewhere for more than 30 days, your home may be flagged as "Vacant," which can trigger a total loss of standard coverage.

- Structural Changes: If you are tearing down walls or expanding the footprint of the kitchen.

- The Project Value is High: If the remodel cost represents more than 10-15% of your home's total value, your current "Replacement Cost" is no longer accurate, creating a massive coverage gap.

4. The Contractor Liability Trap

Don't assume your contractor’s insurance protects your house.

- General Liability: Only covers damage the contractor causes (like if they drop a hammer on your floor).

- Builder's Risk: Covers damage caused by external forces (like a fire, windstorm, or a thief stealing your new fridge).

- 2026 Tip: Always verify your contractor has active Workers' Comp. In Florida’s 2026 legal environment, an injured worker without coverage can sue the homeowner directly.

Why Working with an Independent Agency is Vital

A kitchen remodel should increase your home's value, not your financial risk. At Walker Insurance Agency, we provide the visibility you need to ensure your 2026 project is protected from demolition to the first meal.

The Walker Advantage:

- Gap Analysis: We review your current HO-3 policy to see exactly where it stops and where a temporary Builder’s Risk policy needs to start.

- Certificate of Insurance (COI) Review: We review your contractor's paperwork to ensure they are actually covered for 2026 Florida standards.

- Post-Remodel Revaluation: Once finished, we update your "Replacement Cost" so your new $50,000 kitchen is actually included in your total home value.

FAQ

1. Is Builder's Risk insurance expensive for a kitchen?

In 2026, a policy for a $50,000 kitchen remodel typically costs between $500 and $1,200 for a 6-month term. This is a small price to pay to protect a $50,000 investment.

2. Can I just add an "Endorsement" to my home insurance instead?

Some 2026 Florida carriers allow a "Renovation Endorsement," but these often have lower limits and more exclusions than a standalone Builder's Risk policy.

3. Does Builder's Risk cover "faulty workmanship"?

No. If the contractor installs the cabinets crookedly, that is a matter for the contractor's bond or your contract—not an insurance claim. Builder’s Risk covers accidental damage and theft.

4. What happens if I don't tell my insurance company about the remodel?

This is the most dangerous move. If a fire occurs during construction and the insurer discovers an un-permitted or un-reported major renovation, they can deny the entire claim for "material change in risk."

Protect Your Recipe for Success

Your new kitchen is an investment in your home and your lifestyle. Don't let a theft or an accident during construction turn your dream into a legal battle.

Get a Renovation Review today. Contact Walker Insurance Agency before your contractor starts the demo. We provide the visibility you need to ensure your kitchen is protected from the first swing of the sledgehammer to the final inspection.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us help you build with peace of mind.

Related Articles

Does Homeowners Insurance Cover Trampolines or Pool Slides? (2026)

Planning summer fun in Stuart, FL? Discover why trampolines and pool slides are major homeowners insurance liability traps that can lead to dropped coverage.

Read More →

Does Home or Auto Insurance Cover Boating Accidents? (2026)

Planning a boat day in Stuart? Learn why relying on your home or auto insurance policies for watercraft liability is a dangerous financial gap.

Read More →

Why Home and Auto Insurance Won't Cover Boat Accidents (2026)

Planning a July boat day in Stuart, FL? Discover why relying on your home or auto insurance policies for watercraft liability is a dangerous financial blindspot.

Read More →