New 2026 My Safe Florida Home Grant Requirements | Expert Guide

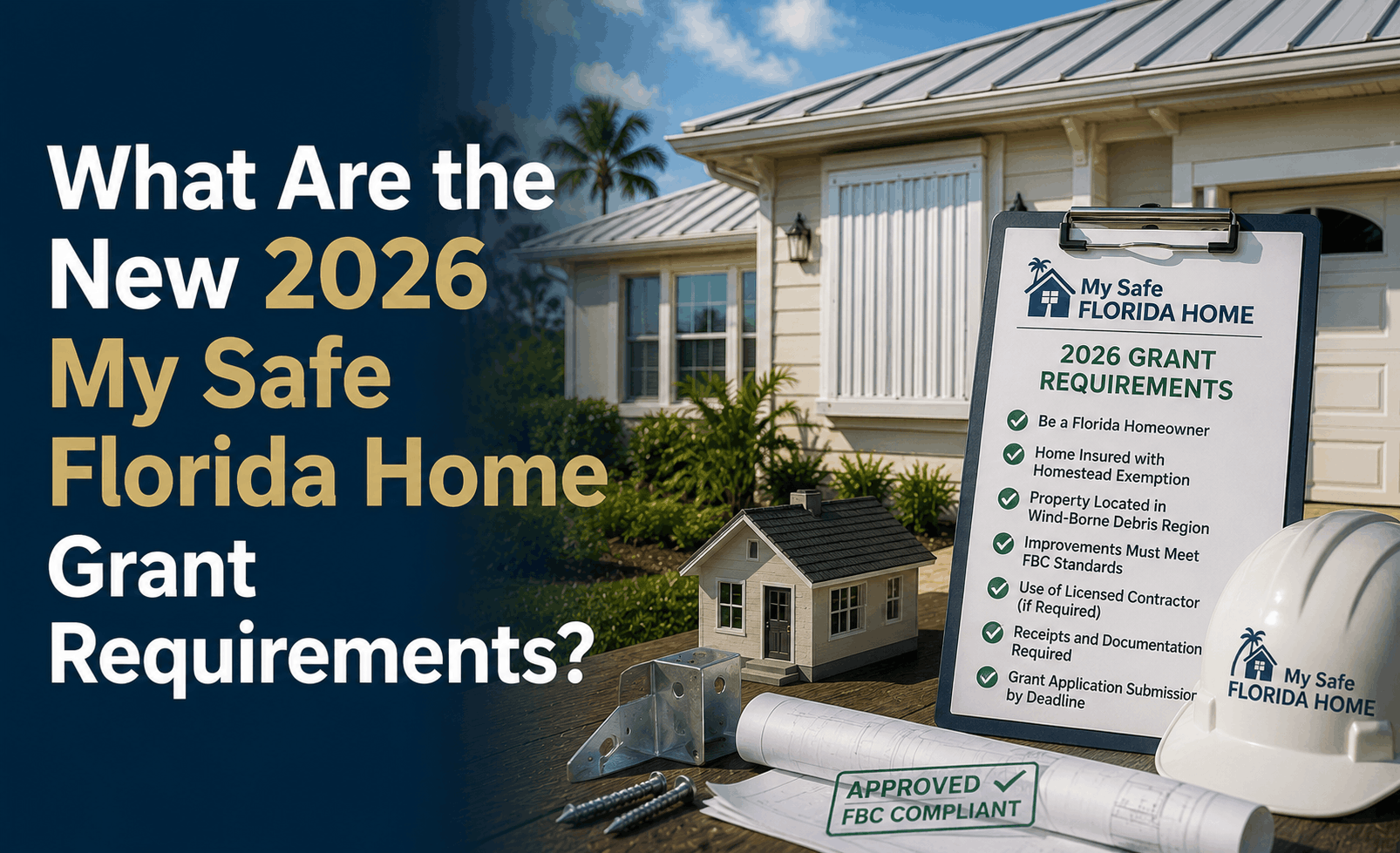

What Are the New 2026 My Safe Florida Home Grant Requirements?

The Direct Answer: For the 2025–2026 cycle, the My Safe Florida Home (MSFH) program has transitioned to a strict priority-based system focusing on vulnerability and income. To qualify for the $10,000 grant, your home must be a site-built, single-family detached house or townhouse with a homestead exemption, and the initial building permit must date before January 1, 2008. In 2026, the program enforces an insured value cap of $700,000 (Coverage A) for standard applicants, while low-income homeowners remain exempt from this limit.

To achieve total visibility over your application, you must apply within your designated "priority window." Missing your window based on your age or income tier could mean losing out on the $600+ million in funding allocated for this year.

1. The 2026 Prioritization Schedule

In 2026, the Florida Department of Financial Services (DFS) manages demand through staggered application windows. You must wait for your group to open:

| Priority Group | Household Status | 2026 Status |

|---|---|---|

| Group 1 | Low-Income (≤80% AMI) + Age 60+ | First Window |

| Group 2 | Low-Income (≤80% AMI) + Any Age | Second Window |

| Group 3 | Moderate-Income (80-120% AMI) + Age 60+ | Third Window |

| Group 4 | Moderate-Income (80-120% AMI) + Any Age | Fourth Window |

Critical Update: In 2026, high-income households (earning over 120% of the county median) are generally ineligible for grants, though they may still apply for the free inspection.

2. Core Eligibility Requirements (The "Big Five")

To secure approval in 2026, you must provide documentation for the following:

- Homestead Exemption: The home must be your primary residence. Rentals, second homes, and "flipped" properties are strictly excluded.

- Building Permit Date: The initial permit for the home must have been applied for before January 1, 2008. Homes built after this date are considered already compliant with modern wind codes.

- Insured Value Cap: Your home's Coverage A (Dwelling) limit must be $700,000 or less.

- Exception: If you qualify as low-income, this cap does not apply to you.

- Active Insurance: As of 2025-2026, all applicants (including low-income) must show proof of an active homeowners insurance policy.

- The Program Inspection: You cannot use an outside wind mitigation report. You must request and complete a free inspection through the official mysafeflhome.com portal first.

3. How the Grant Money Works: Matching vs. Full

In 2026, the state has simplified the grant structure into two categories:

- Matching Grant (Moderate Income): The state provides a 2-for-1 match. For every $1 you pay, the state contributes $2, up to $10,000. To get the full $10,000, your total project must cost at least $15,000 ($10k state / $5k you).

- Low-Income Grant (No Match): Homeowners earning ≤80% of the Area Median Income (AMI) can receive up to $10,000 for 100% of the project cost. No personal contribution is required.

4. Eligible Improvements for 2026

The grant is restricted to "hardening" the home's envelope. You cannot use it for aesthetics.

- Opening Protection: Impact-rated windows, exterior doors, and garage doors.

- Roof Strengthening: Secondary Water Resistance (SWR), roof-to-wall attachments (clips/straps), and roof deck nailing.

- The "No-Swap" Rule: If you already have compliant hurricane shutters, the program will not fund a switch to impact windows.

Why Working with an Independent Agency is Vital

The goal of home hardening is to lower your insurance premiums. At Walker Insurance Agency, we provide the visibility you need to maximize your ROI:

- Premium Audit: We review your inspection report to identify which upgrades will trigger the largest Wind Mitigation Credits.

- Market Comparison: Once your home is hardened, we shop the 2026 Florida market to see if you qualify for lower-cost private carriers, moving you away from high-priced options like Citizens.

FAQ

1. Is the $700,000 limit based on my home's market value?

No. It is based on the Coverage A (Dwelling) limit found on your homeowners insurance declarations page.

2. Can I use my own contractor for MSFH?

Yes, provided they are a Florida-licensed contractor. You no longer need to choose from a specific "MSFH list," but the state must verify their license before payout.

3. What if I start the work before I get the award letter?

DO NOT start work. Any contract signed or work started before you receive your official Grant Award Letter will be 100% ineligible for reimbursement.

4. Does the grant cover mobile or manufactured homes?

No. The 2026 MSFH program is only for site-built homes and townhouses.

Local Business Schema

Don’t Miss Your 2026 Priority Window

The My Safe Florida Home program is the single best way to lower your insurance costs in 2026, but the funds go fast.

Secure your savings today. Contact Walker Insurance Agency for a complimentary policy review. We provide the visibility you need to ensure your hardening project results in the maximum possible insurance discount in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us help you protect your home.

Related Articles

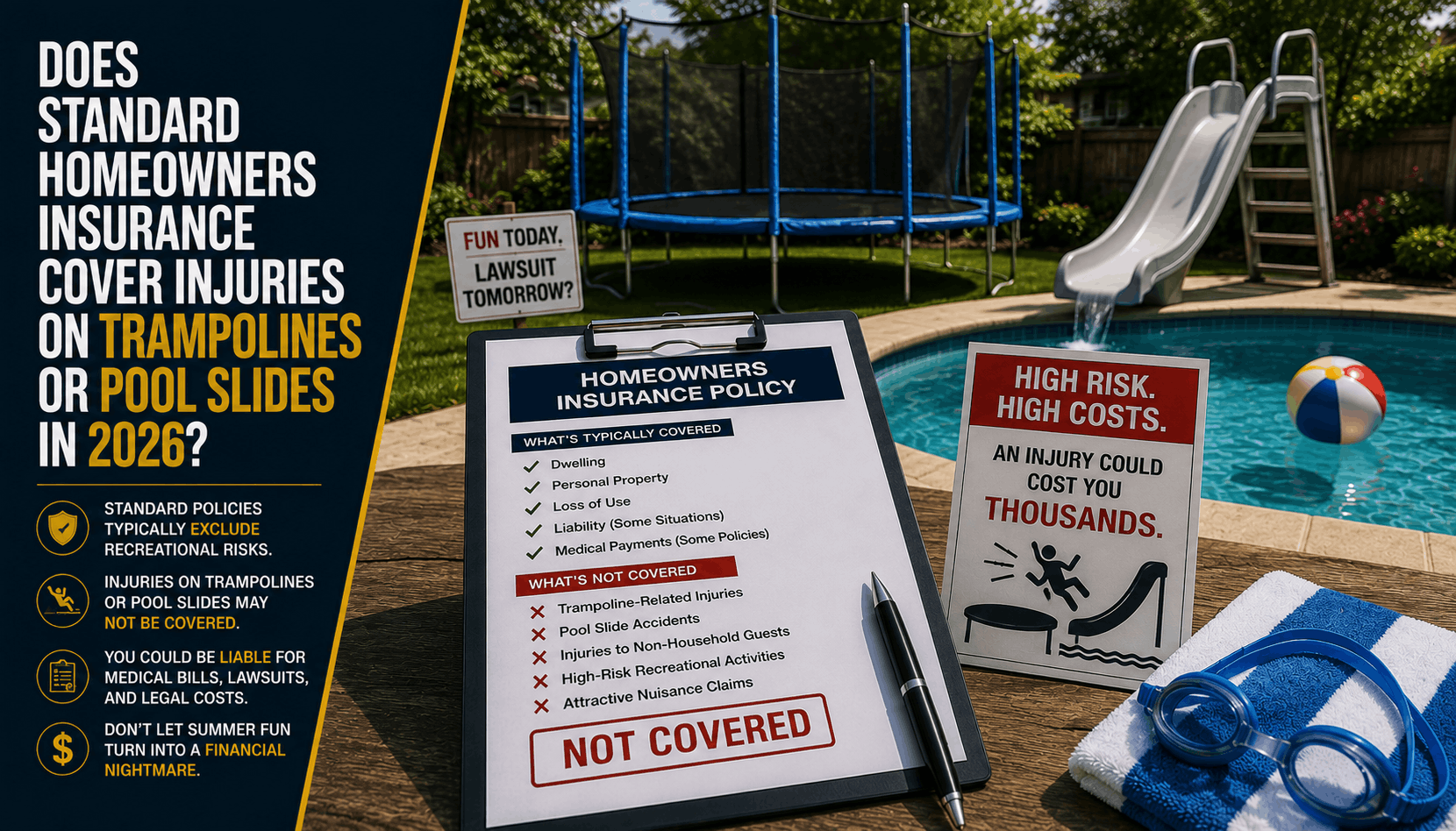

Does Homeowners Insurance Cover Trampolines or Pool Slides? (2026)

Planning summer fun in Stuart, FL? Discover why trampolines and pool slides are major homeowners insurance liability traps that can lead to dropped coverage.

Read More →

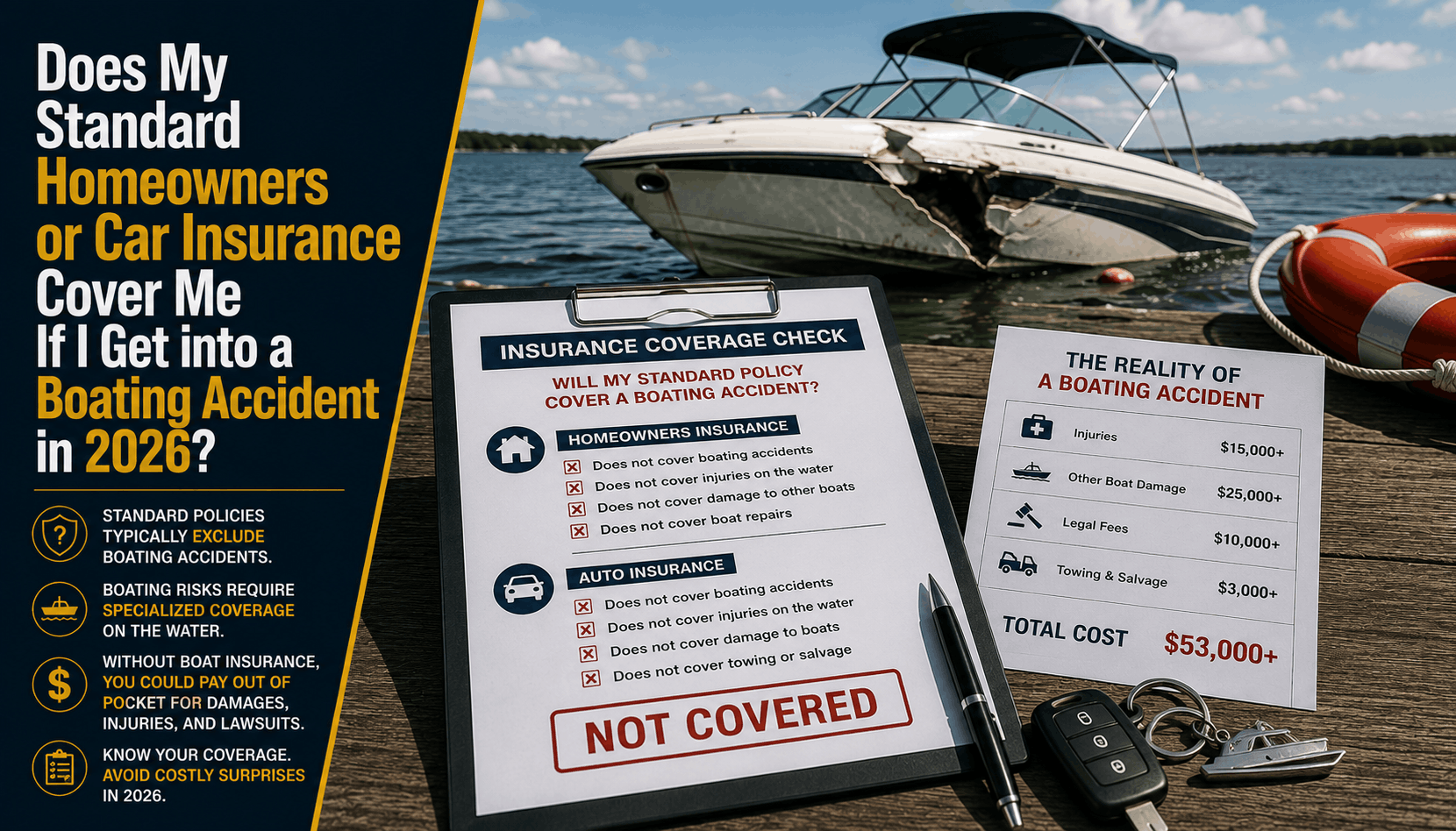

Does Home or Auto Insurance Cover Boating Accidents? (2026)

Planning a boat day in Stuart? Learn why relying on your home or auto insurance policies for watercraft liability is a dangerous financial gap.

Read More →

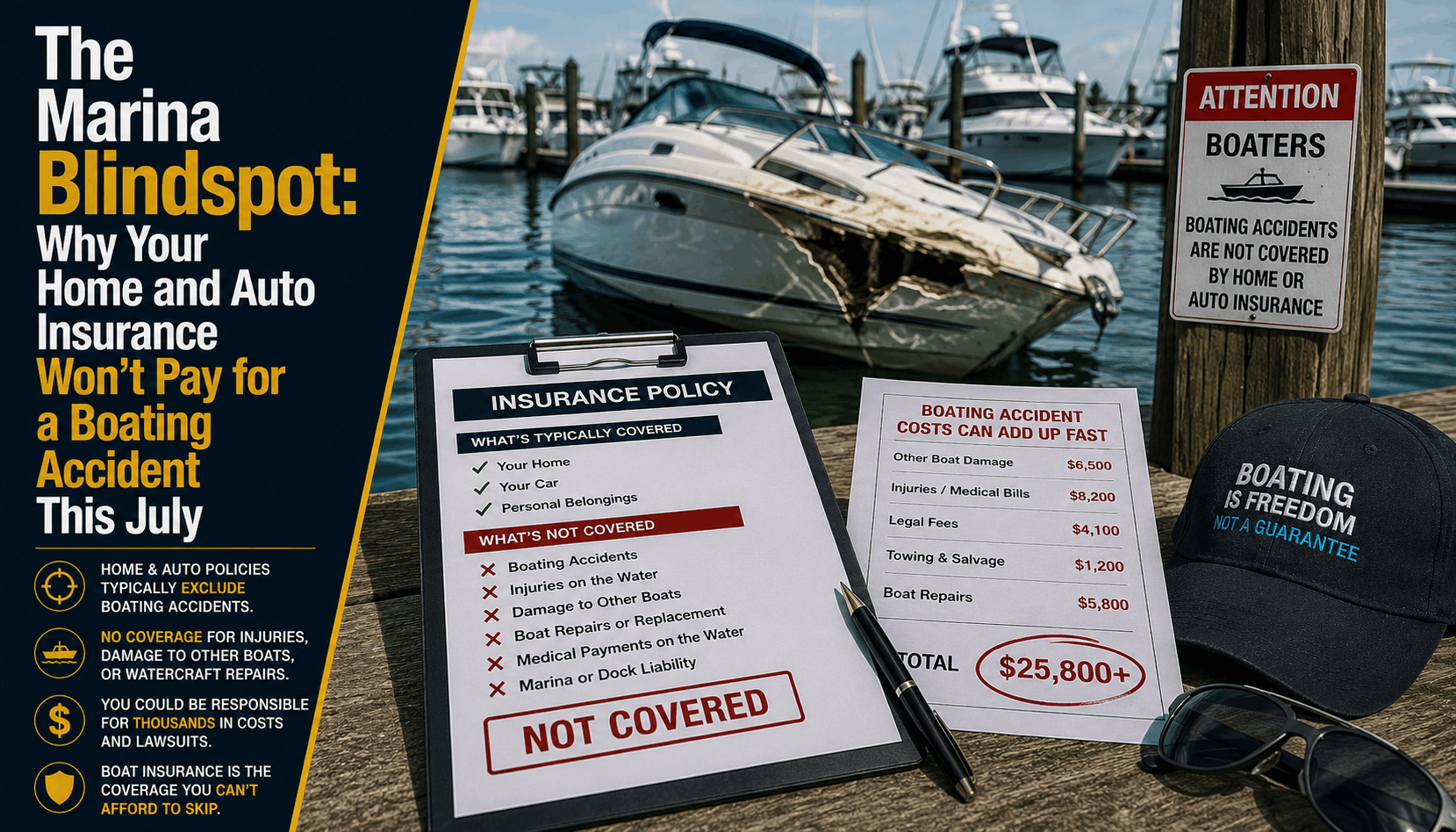

Why Home and Auto Insurance Won't Cover Boat Accidents (2026)

Planning a July boat day in Stuart, FL? Discover why relying on your home or auto insurance policies for watercraft liability is a dangerous financial blindspot.

Read More →