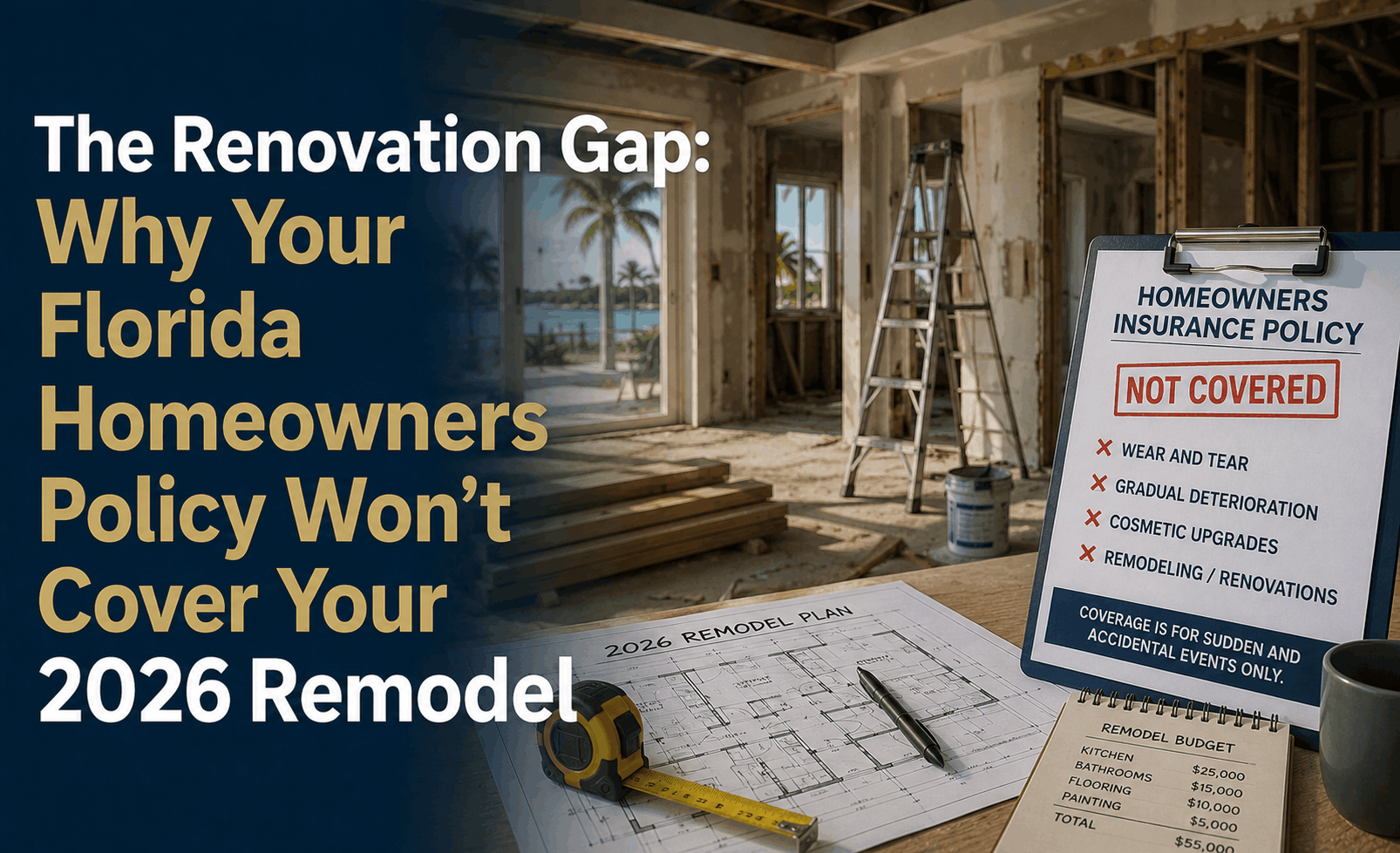

The Renovation Gap: Why Florida Home Insurance Won’t Cover Your 2026 Remodel

The Renovation Gap: Why Your Florida Homeowners Policy Won’t Cover Your 2026 Remodel

The Direct Answer: A standard Florida homeowners policy (HO-3) is designed for a finished, occupied home—not an active construction site. The moment you begin a major renovation in 2026, you enter the "Renovation Gap." During this time, your insurer may exclude coverage for theft of building materials, damage to the structure while partially exposed, or liability for worker injuries. In 2026, where Florida’s rebuild costs have risen to over $280 per square foot, relying on a standard policy during a remodel is a high-stakes gamble that can lead to a total loss denial.

To achieve total visibility over your investment, you must understand that "remodeling" changes your risk profile. In the eyes of a 2026 Florida insurer, a house with a missing roof or a gutted interior is no longer a "home"—it is a high-risk liability.

1. The Three "Deal-Breakers" for Florida Insurers

In 2026, Florida insurance carriers have tightened their guidelines due to rising material costs and litigation. Most policies now trigger automatic exclusions when:

- The "V-Clause" (Vacancy): If you move out for more than 30 or 60 days during construction, your policy may become "suspended" or exclude theft and vandalism.

- The Soft-Structure Risk: If your home is "opened up" (roof removed or walls down) and a 2026 tropical storm causes water damage, your insurer will likely deny the claim, citing a failure to maintain a protective envelope.

- Material Theft: Standard policies cover your belongings, but they rarely cover uninstalled building materials like $15,000 worth of uninstalled Italian marble or high-end appliances sitting in your garage.

2. Builder’s Risk: The 2026 Mandatory Shield

If your project exceeds a specific dollar threshold (often $25,000 to $50,000 in 2026), you likely need a Builder’s Risk Policy (also known as "Course of Construction" insurance).

What Builder's Risk covers that your HO-3 won't:

- Theft of Materials: Covers copper wiring, lumber, and appliances before they are installed.

- Partial Structure Collapse: Protects the home if a temporary support fails during a structural remodel.

- Soft Costs: Reimburses you for permit fees and additional interest on construction loans if a covered loss delays the project.

3. The Liability Trap: Who Pays if Someone is Hurt?

In 2026, Florida’s at-fault laws have placed a premium on liability. If a subcontractor is injured on your property and your general contractor's Workers' Comp is lapsed or insufficient, the lawsuit will target you.

- Standard Liability Limits: Most HO-3 policies cap at $300,000. In 2026, a serious construction injury lawsuit can easily exceed $1 million.

- Contractor Verification: You must require a Certificate of Insurance (COI) naming you as an "Additional Insured" before the first hammer swings.

4. 2026 Post-Renovation: The Revaluation Rule

Once the dust settles, your "Renovation Gap" risk isn't over until you update your Replacement Cost.

- Underinsurance Risk: If you spend $100,000 on a new kitchen and addition but don't notify your agent, you are "coinsuring" the risk. If a fire occurs, the insurer may only pay a fraction of the claim because the home was undervalued on the 2026 market.

- Wind Mitigation Credits: Many 2026 remodels include impact windows or secondary water barriers. These can trigger massive discounts, but only if you submit a new 2026 Wind Mitigation Inspection.

Why Working with an Independent Agency is Vital

Remodeling in Florida is stressful enough without an insurance denial. At Walker Insurance Agency, we provide the visibility you need to bridge the gap between "Under Construction" and "Fully Protected."

The Walker Advantage:

- Builder’s Risk Sourcing: We shop specialized 2026 Florida markets to find temporary coverage that fits your project's timeline.

- Permit Monitoring: We help you understand how your specific county permits in Stuart or across Florida impact your policy requirements.

- Replacement Cost Valuation: We use 2026-accurate construction data to ensure your new luxury finishes are actually covered at today's prices.

FAQ

1. Does my homeowners insurance cover my DIY remodel? Generally, yes, for minor cosmetic work (paint, flooring). However, if you do your own electrical or plumbing and cause a fire or flood, your insurer may investigate if the work was permitted and up to 2026 Florida code.

2. Is Builder's Risk expensive in 2026? In Florida, Builder's Risk typically costs between $1.20 and $4.50 per $100 of construction value. For a $100,000 remodel, expect to pay between $1,200 and $4,500 for the duration of the project.

3. What happens if I move out during the remodel? You must notify your agent. You may need a Vacancy Permit or a specific endorsement to ensure your home remains covered while it is unoccupied.

4. Will my premium go up after I renovate? Usually, yes. Since your home is now worth more and would cost more to rebuild, your Coverage A (Dwelling) limit must increase, which raises the premium. However, new impact windows can help offset this increase.

Don’t Let Your Dream Remodel Become a Financial Nightmare

You’ve saved for the perfect home; don't lose it because of an insurance technicality. The "Renovation Gap" is real, and in 2026, Florida insurers are checking the fine print more than ever.

Get a Project Review today. Contact Walker Insurance Agency before you sign that construction contract. We provide the visibility you need to ensure your home is protected from the first day of demolition to the final inspection.

[GET A FREE QUOTE TODAY] Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us help you build with confidence.

Related Articles

Does Homeowners Insurance Cover Trampolines or Pool Slides? (2026)

Planning summer fun in Stuart, FL? Discover why trampolines and pool slides are major homeowners insurance liability traps that can lead to dropped coverage.

Read More →

Does Home or Auto Insurance Cover Boating Accidents? (2026)

Planning a boat day in Stuart? Learn why relying on your home or auto insurance policies for watercraft liability is a dangerous financial gap.

Read More →

Why Home and Auto Insurance Won't Cover Boat Accidents (2026)

Planning a July boat day in Stuart, FL? Discover why relying on your home or auto insurance policies for watercraft liability is a dangerous financial blindspot.

Read More →