The Front Lawn Dig: Why You Own the Underground Utility Risk in 2026

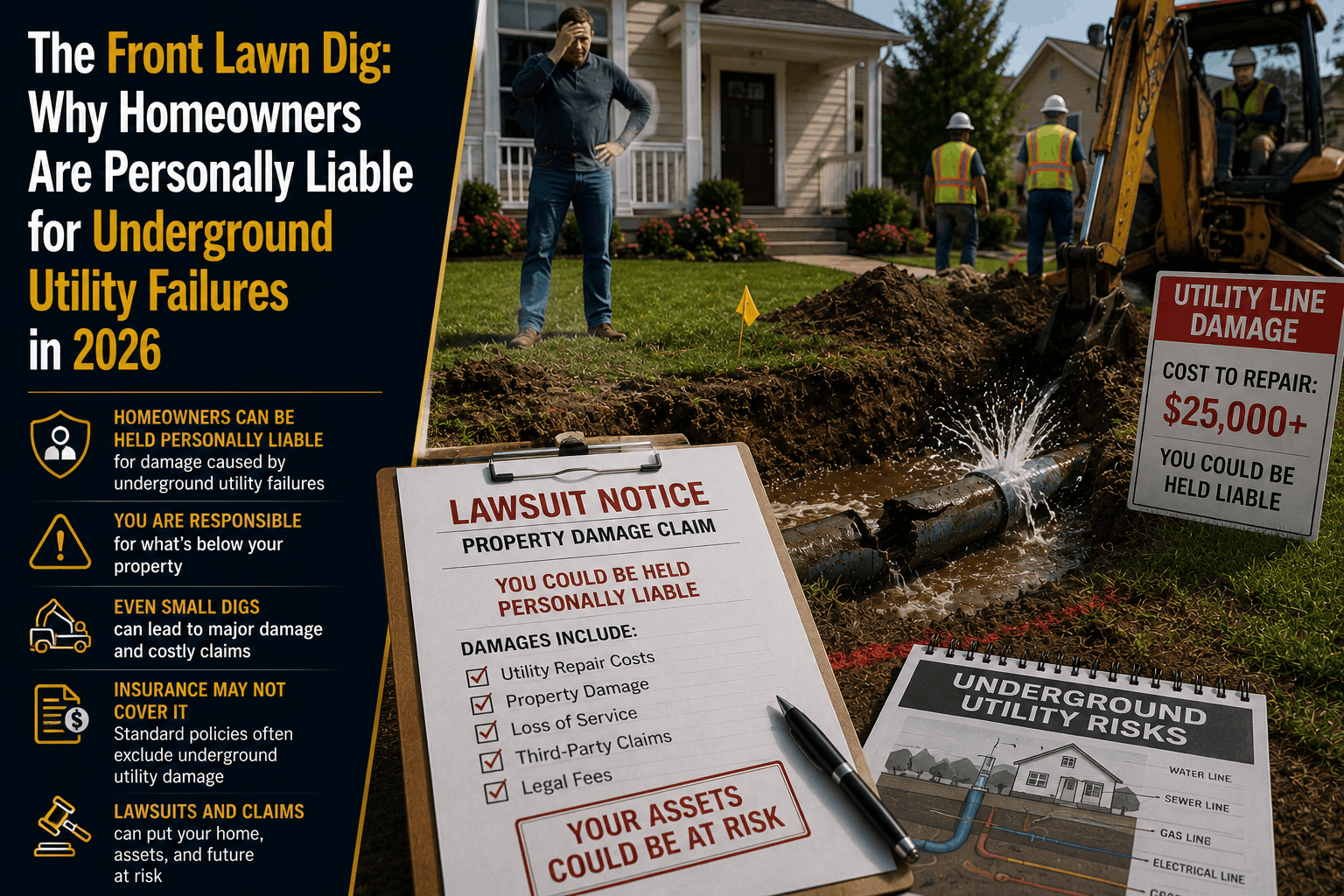

The Front Lawn Dig: Why Homeowners Are Personally Liable for Underground Utility Failures in 2026

The Direct Answer: The expensive reality facing property owners is that you are legally and financially responsible for every foot of utility infrastructure buried under your yard. If the main sewer lateral cracks, an incoming water line ruptures, or the underground electrical line short-circuits beneath your front grass, the city will not pay for it.

Even worse, a standard homeowners insurance policy completely excludes buried utility lines. Standard home insurance is contractually structured to protect the house from the concrete slab upward.

In 2026, as suburban infrastructure naturally reaches its historical expiration date, excavation and repair bills are skyrocketing to an industry average of $7,000 to $12,000 per incident. Unless you have explicitly updated your policy with an optional add-on known as an Underground Service Line Endorsement, you are entirely on your own to fund the dig.

1. The Boundary Line: Where Your Liability Begins

Many homeowners believe their financial responsibility stops at the physical exterior walls of their house. Municipal utility companies utilize a highly strict boundary system that dictates otherwise:

- The Tap Connection: Your personal liability begins the exact millimeter a utility pipe or wire branches off from the city’s central main trunk line—typically located right at the edge of the street curb or property boundary line.

- The Service Lateral: The entire length of the pipe running through your front lawn to your interior plumbing or electrical panel is classified as private property. If a tree root punctures that pipe ten feet out in your yard, it is legally treated no differently than a broken pipe inside your kitchen cabinet.

2. Why Are Buried Infrastructure Failures Spiking?

Underground line collapses have shifted from a rare structural anomaly into a predictable seasonal risk due to three major market factors intersecting all at once:

[Aging Post-War Pipe Materials] + [Accelerated Subterranean Root Systems]

= Advanced Ground Pressure ──> Catastrophic Line Rupture or Pipe Collapse

- The Clay and Orangeburg Crisis: Millions of homes built between the 1950s and 1980s utilize vitrified clay, cast iron, or bituminous fiber (Orangeburg) pipes. These materials have a maximum operational lifespan of 40 to 60 years. Across neighborhoods, these lines are hitting their structural limits and dissolving under the soil.

- The Soil Movement Squeeze: Shifting seasonal moisture levels cause local soils to expand and contract aggressively. This constant subterranean movement exerts thousands of pounds of pressure on rigid, brittle pipes, triggering immediate stress fractures and joint separations.

- The Tech-Heavy Repair Overhead: Fixing a buried utility is no longer a simple matter of a plumber digging a hole with a shovel. In 2026, modern environmental and municipal codes require specialized heavy machinery, utility location permits, structural backfilling, and post-excavation asphalt or concrete restoration—driving baseline labor costs to record highs.

3. The Structural Breakdown: What Is Actually Excluded?

If you suffer a main line collapse under your grass, a claims adjuster operating under a standard, un-endorsed property contract will drop a denial letter into your mailbox citing these three primary exclusions:

| Buried Line Type | Common Cause of Failure | Standard Policy Status | Out-of-Pocket Expense Focus |

|---|---|---|---|

| Sewer Lateral | Tree root intrusion, heavy corrosion, decay. | EXCLUDED | Heavy excavation, hazardous waste extraction. |

| Water Main | Soil shifting, freeze/thaw cracks, high pressure. | EXCLUDED | Trenching, lawn replacement, pipe installation. |

| Electrical / Cable | Rodent chewing, mechanical arcing, rust. | EXCLUDED | Specialized conduit drilling, municipal inspections. |

The Landscaping Trap: Even if a utility company enters your yard to service a city-owned section of the line, their administrative charter rarely requires them to restore your private property. They will fill the trench with basic dirt and gravel, leaving you completely responsible for the thousands of dollars needed to rebuild your ruined concrete driveway, custom walkways, or manicured landscaping.

How to Close the Front Lawn Gap Safely

Allowing your property asset to sit on an unmodified baseline insurance policy means your entire cash reserve is exposed to a single tree root.

At Walker Insurance Agency, we help property owners build an ironclad subterranean shield using a precise, highly cost-effective adjustment:

Step 1: Unearth and Audit Your Policy's Utility Endorsements

Step 2: Bind a Specialty Service Line Rider with a $10,000 - $15,000 Limit

=========================================================================

= Comprehensive Excavation, Pipe Replacement, and Lawn Restoration Protection

Adding a dedicated Underground Service Line Endorsement to your homeowners policy is one of the highest-value moves available, typically costing just $20 to $50 per year.

This specialized rider completely overrides the standard exclusions, paying for the heavy machinery excavation needed to reach the broken line, the brand-new replacement piping or electrical wiring, and the full cosmetic restoration of your grass, shrubs, and hardscaping. Most riders feature a standard, manageable $500 deductible, transforming a potential $10,000 household financial emergency into a simple administrative claim.

Why Working with an Independent Agency is Vital

Attempting to manage your home protection through a generic online application ensures your contract will be completely exposed to these massive infrastructure blindspots. At Walker Insurance Agency, we provide the data-driven visibility you need to defend your land.

The Walker Advantage:

- Rider Scope Optimization: We audit your property's specific age and structural layout to ensure your line endorsement limits accurately match local excavation labor rates.

- Water Backup Integration: We seamlessly align your buried utility coverage with your internal Water Backup Riders, ensuring you have seamless protection from the concrete slab all the way to the city street.

- Private Market Shopping: As the stabilizing Florida market introduces 20 brand-new private insurance carriers, we continually shop your profile to secure the highest-limit property riders at the absolute lowest available premium floors in Stuart.

FAQ

1. Does a service line endorsement cover failures to an on-site septic tank or well system?

While the endorsement will cover the physical buried pipes running to and from your house to a septic tank or private well, it will never cover the structural failure of the septic tank itself, the drain field, or the mechanical well pump machinery. Those items require separate specialty equipment endorsements.

2. Can I purchase this utility coverage if my home is over 50 years old?

Yes. Unlike standard systems that penalize older builds, most top-tier independent carriers do not restrict service line endorsements based strictly on the chronological age of the home, provided there is no pre-existing, active leak or documented ongoing failure at the time you bind the coverage.

3. What should I do immediately if I suspect my main water or sewer line has collapsed?

Do not authorize a contractor to begin heavy trenching work without notifying your agent. Call a licensed technician to perform a non-invasive camera inspection of the line. Request a copy of the video file and a formal diagnostic write-up detailing the exact location and cause of the rupture. This data provides the primary proof required to instantly open a covered claim.

Insulate Your Savings From a Devastating Excavation Bill

An underground utility failure is messy, disruptive, and incredibly expensive. Relying on an ordinary, baseline insurance policy to cover a deep-earth emergency is an administrative gamble that can instantly wipe out your emergency fund the moment an aging pipe collapses under your grass.

Secure your lawn protection before an emergency strikes. Contact Walker Insurance Agency today for a comprehensive property coverage review. We provide the visibility you need to erase hidden utility loopholes, deploy high-limit service line riders, and protect your family's hard-earned wealth safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us secure your property lines today.

Related Articles

Does Collision Cover Hit-and-Run Damage Without a Deductible? (2026)

Had your car struck in a hit-and-run? Learn how collision coverage applies, when deductibles are required, and how UMPD can save you money in 2026.

Read More →

Does Collision Insurance Cover Hail & Tree Damage in 2026?

Did hail or a falling tree branch damage your car? Learn why collision auto insurance won't pay for storm damage and how comprehensive coverage protects you.

Read More →

Why Collision Insurance Pays $0 for Non-Crash Summer Damage (2026)

Did a tree branch, hail storm, or flying road debris hit your car this summer? Discover why collision auto insurance pays $0 and how comprehensive coverage protects you.

Read More →