The History Stigma: Diminished Value Claims in 2026

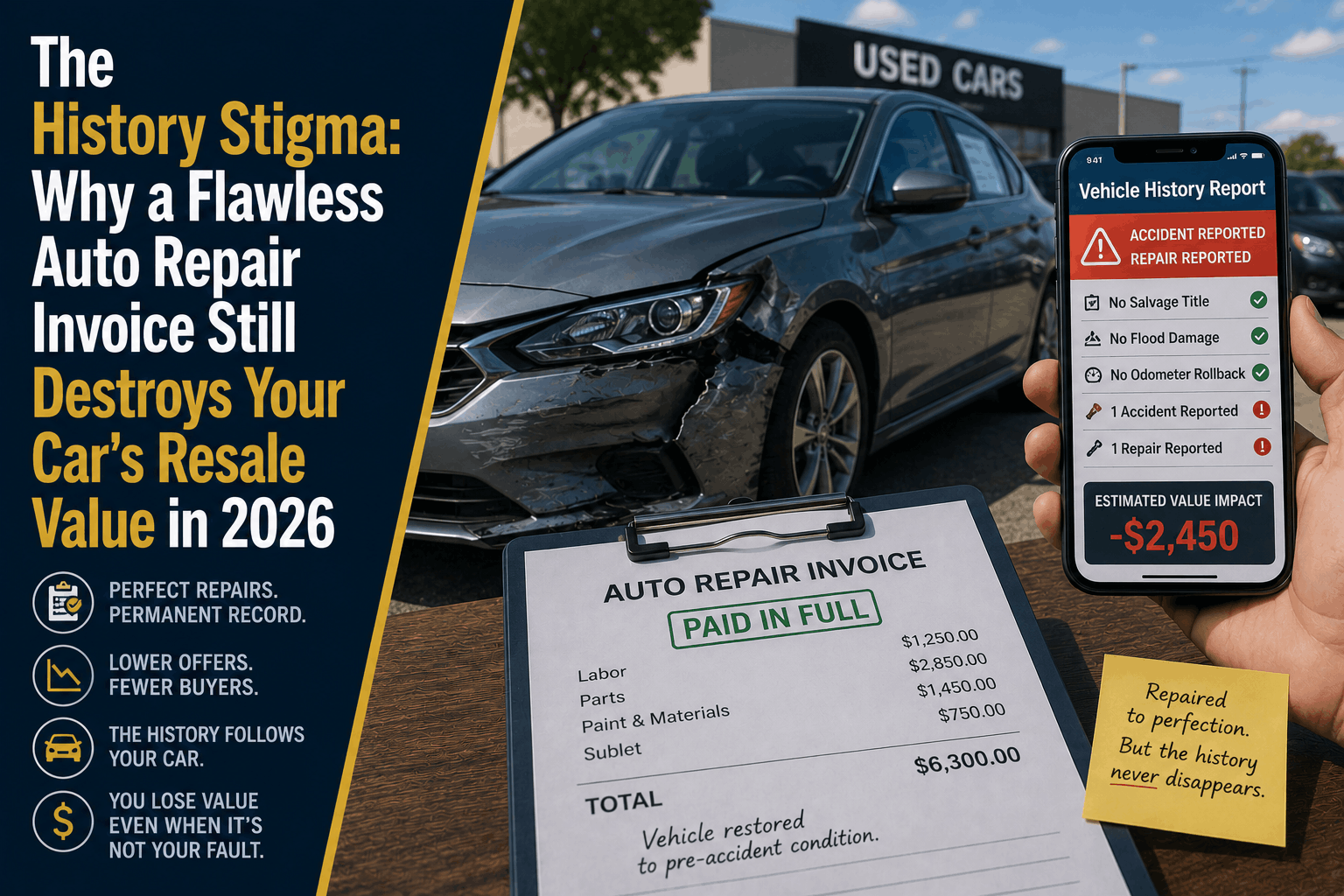

The History Stigma: Why a Flawless Auto Repair Invoice Still Destroys Your Car’s Resale Value in 2026

The Direct Answer: The "History Stigma" is the immediate, permanent drop in a vehicle's market value that occurs the exact second an accident is logged against its Vehicle Identification Number (VIN). It does not matter if the repair was performed by a certified master technician, used 100% original manufacturer (OEM) parts, and left the car looking completely flawless. To the automotive market, a repaired car is damaged goods.

In 2026, this financial loss is sharper than ever. Because vehicle history reporting databases like CARFAX and AutoCheck are now tightly integrated with automated dealer appraisal algorithms, an accident record instantly triggers an unnegotiable 10% to 30% reduction in your car’s trade-in value.

To achieve total visibility over your automotive wealth, you must realize that standard physical damage insurance only fixes the metal—it leaves you entirely exposed to an uncompensated financial loss known as Inherent Diminished Value.

1. The Algorithm Penalty: The Digital Scarlet Letter

A decade ago, you could hide a minor dent repair by showing a prospective buyer a stack of clean, professional garage invoices. In 2026, the human element has been completely stripped out of the vehicle valuation process.

[Minor Rear-End Accident] ──> [Logged to CARFAX via Body Shop Software]

│

[Dealer Trade-In Appraisal AI] <─────────────┘

│

└──> Automated "Accident History" Deduction Applied ──> $3,000 to $7,000 Loss

The Transparency Trap: Modern collision center management software is digitally linked to history aggregators. The moment a shop generates an insurance estimate or orders a replacement quarter panel, the event is automatically stamped onto your vehicle's public history file. When you attempt to trade the vehicle in, the dealership’s appraisal software reads the "Accident Reported" flag and automatically drops the valuation floor—completely ignoring how perfect the physical repair looks under the lights.

2. Why the 2026 Market is Brutal on Repaired Cars

The current automotive landscape has amplified the history stigma due to two massive structural shifts:

- The Certified Pre-Owned (CPO) Bottleneck: Dealerships make their highest profit margins by turning used cars into high-tier Certified Pre-Owned vehicles. However, major automotive manufacturers carry strict corporate mandates: any vehicle with a structural or major cosmetic accident history is legally disqualified from the CPO program. Because a dealer cannot certify your repaired car, they will only buy it at a steep wholesale discount to flip it to an off-brand salvage auction.

- The Private Buyer Trust Gap: With vehicle data fully democratized, private used-car buyers have zero incentive to take a gamble on a vehicle with a spotty history report. If two identical 2023 SUVs are listed for $25,000, but one has a "Minor Accident" flag, the buyer will either demand a massive $4,000 price cut or simply click away to a clean alternative.

3. How to Calculate and Recover Your Lost Equity

If you were not at fault for the accident, you do not have to absorb this equity wipeout out of pocket. You have the legal right to file a third-party Diminished Value Claim against the at-fault driver’s insurance company.

To win this negotiation, you must understand the industry-standard valuation framework known as the 17c Formula:

$$\text{Base Loss} = \text{Clean Market Value} \times 10\% \text{ (Maximum Cap Amount)}$$

Once the base loss is established, insurance adjusters apply two modifiers to calculate your final settlement check:

The Damage Severity Modifier

- 1.00: Severe structural/frame damage

- 0.50: Moderate panel and structural damage

- 0.25: Minor cosmetic/bumper damage

- 0.00: No structural or major mechanical damage

The Mileage Modifier

- 1.00: 0 – 19,999 miles

- 0.80: 20,000 – 39,999 miles

- 0.60: 40,000 – 59,999 miles

- 0.40: 60,000 – 79,999 miles

- 0.20: 80,000 – 99,999 miles

- 0.00: 100,000+ miles

Example: If your clean 2024 vehicle is worth $40,000, has 15,000 miles, and suffered moderate panel damage, your calculated diminished value cap is $\$4,000 \times 0.50 \times 1.00 = \mathbf{\$2,000}$.

How to Safely Build an Equity Shield

Allowing an insurance adjuster to close your claim the moment your car rolls out of the body shop ensures you are leaving thousands of dollars of personal wealth on the table.

At Walker Insurance Agency, we advise clients to execute a precise, proactive claims recovery framework:

Step 1: Demand a Copy of the Final Insurance Teardown & Repair Bill

Step 2: Secure an Independent, Certified Diminished Value Appraisal

Step 3: Issue a Formal Demand Letter to the At-Fault Carrier's Adjuster

========================================================================

= Legal Financial Restitution for Your Vehicle's Lost Market Value

Do not rely on the insurance company to volunteer this payout. Adjusters are trained to keep quiet about diminished value. To force their hand, you must hire an independent appraiser to generate a formal report comparing your car's value against un-damaged local market sales, backed by local dealer quotes confirming they would slash your trade-in offer based strictly on the new accident flag.

Why Working with an Independent Agency is Vital

Managing an auto claim through an automated corporate smartphone app leaves your profile completely exposed to hidden post-accident equity losses. At Walker Insurance Agency, we provide the personalized, data-driven visibility you need to defend your garage investments.

The Walker Advantage:

- Claims Advocacy Guidance: We walk you through the precise steps required to compile documentation against third-party carriers to maximize your diminished value payouts.

- Policy Structure Optimization: We review your collision line deductibles and ensure your coverage carries proper Uninsured Motorist property protections to defend your equity if a hit-and-run driver strikes your vehicle.

- Account Portability Management: As the auto insurance market stabilizes, we continuously shop your risk profile across top-tier carriers, ensuring you maintain the highest limits at the absolute lowest available premium floors in Stuart.

FAQ

1. Can I file a diminished value claim if I was the at-fault driver in the accident?

No, in almost all states. First-party diminished value claims (claims filed against your own insurance policy) are contractually banned by the standard language written into personal auto insurance jackets. You can only recover diminished value if another driver hits your vehicle and you file a third-party claim against their active property damage liability coverage.

2. Is there a statute of limitations on filing a diminished value claim?

Yes. The timeline is dictated by individual state laws regarding property damage claims. For example, in Florida, you generally have up to two years from the exact date of the accident to formally file and settle a diminished value recovery claim against the at-fault party's insurer.

3. Does a leased vehicle qualify for a diminished value claim?

No. Because you do not legally own the vehicle's title, you do not suffer the long-term equity loss caused by the history stigma. The leasing company (the financial institution holding the title) absorbs the market value drop when the car is returned at the end of the term, meaning only the registered titleholder has the legal standing to pursue a claim.

Reclaim the True Value of Your Investment Today

Your car is one of the largest moving financial assets you own, but in the modern digital marketplace, an accident history report is a financial weapon that can instantly wipe out thousands of dollars of your hard-earned equity. Protecting your wealth requires shifting away from basic repair coverage and claiming the full economic restitution you are legally owed.

Don't leave your cash in the insurance carrier's pockets. Contact Walker Insurance Agency today for a comprehensive asset and policy evaluation. We provide the visibility you need to navigate the claims process safely, counter unfair adjuster metrics, and protect your lifestyle securely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us safeguard your automotive equity today.

Related Articles

Does Home Insurance Cover Legal Fees & Lost Wages from Identity Theft? (2026)

Learn if standard home insurance covers legal fees and lost wages from identity theft in 2026, how endorsement sub-limits work, and how to get full fraud recovery.

Read More →

The Hidden Cost of Fraud: Does Home Insurance Cover Identity Theft? (2026)

Discover why standard homeowners insurance won't pay to restore a stolen identity in 2026, what hidden fraud costs you face, and how an Identity Theft Endorsement protects you.

Read More →

Does Water Backup Insurance Pay for a Hotel During Basement Sanitization? (2026)

Learn if water backup insurance pays for hotel stays while your basement is sanitized in 2026, how Loss of Use sub-limits work, and how to avoid out-of-pocket costs.

Read More →