Does Homeowners Insurance Cover Mold & Slow Wall Leaks? (2026 Rules)

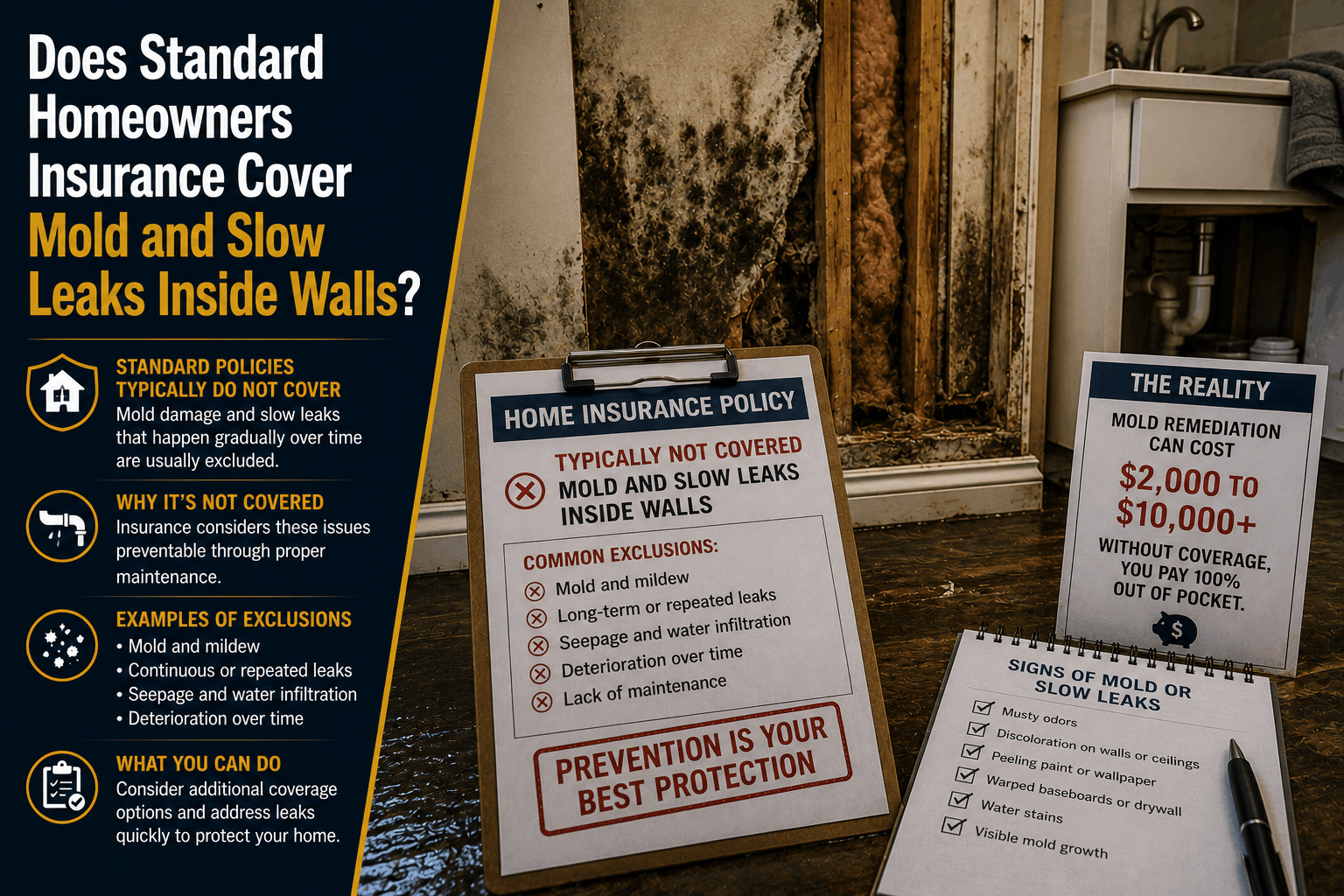

Does Standard Homeowners Insurance Cover Mold and Slow Leaks Inside Walls?

The Direct Answer: Generally, no—standard homeowners insurance does not cover mold or water damage caused by slow, gradual leaks inside your walls. While your policy is contractually bound to cover sudden and accidental water damage (such as a water heater tank bursting completely open), it explicitly excludes damage from wear and tear, neglect, or gradual deterioration.

In 2026, this boundary is aggressively enforced by carrier claims adjusters using a strict contractual clause known as the 14-day constant seepage rule. Under standard policy language, if a pipe behind your drywall drips, seeps, or sweats quietly for 14 calendar days or more, the entire claim is legally voided—even if the leak was entirely hidden and you only discovered it today.

Furthermore, mold is handled strictly as a secondary condition. If the underlying water leak is denied because it was a slow, long-term drip, 100% of the resulting mold remediation will be denied as well.

1. The 14-Day Clock: How Adjusters Calculate Seepage

Many property owners assume that if they file a claim the exact same day they spot a soft, warped, or damp patch on their drywall, their coverage is safe. However, the insurance contract does not care when you discovered the damage; it only cares when the water started escaping.

Modern insurance companies utilize advanced forensic testing and digital moisture mapping during field inspections to establish an exact timeline of the decay:

[Sudden Pipe Fracture: Occurred 2 Days Ago] ──> 100% COVERED under standard guidelines.

[Micro-Drip Pinhole: Seeping for >14 Days] ──> 100% DENIED under the seepage exclusion.

The Forensic Tell-Tales: Claims adjusters do not guess. If the interior of your wall cavity reveals deep structural wood rot, black fungal colonies, rusted framing nails, or completely disintegrated insulation, these physical characteristics mathematically prove that moisture has been trapped for weeks or months. The carrier will immediately classify the issue as a "maintenance failure" and deny the claim.

2. The Florida Mold Cap Trap

If an interior leak is determined to be sudden and accidental (for instance, a pipe unexpectedly cracking due to a sudden water pressure spike), the resulting mold growth may be eligible for coverage. However, you still face a massive financial bottleneck:

- The Statutory Sub-Limit: Standard home insurance policies in Florida carry a rigid, built-in $10,000 cap on mold remediation.

- The Real Cost: Because Florida's hot, humid climate acts as an absolute incubator for fungal spores, mold trapped inside a warm wall cavity can migrate into your central HVAC ductwork in less than 48 hours. Professional hazardous bio-clean teams, air scrubbers, containment barriers, and post-remediation clearance testing routinely cost $20,000 to $40,000, leaving you to fund the massive remaining deficit entirely out of pocket.

3. The Structural Reconstruction Overhead

Fixing the tiny pinhole leak in a copper or PEX pipe is relatively inexpensive. The true financial disaster is the structural tear-down and rebuild required to clear the mold and rotted studs safely.

Because contractor and material inflation remain highly elevated, a full multi-room remediation cycle is a severe budget-killer:

| Repair Phase | Required Operational Work | Average Out-of-Pocket Cost |

|---|---|---|

| Plumbing Repair | Cutting out the corroded section of pipe, soldering/crimping new lines. | $300 – $600 (Never covered by insurance) |

| Hazardous Mitigation | Setting up negative-pressure containment, running HEPA scrubbers, pulling rotted insulation. | $3,500 – $7,000 |

| Structural Rebuild | Replacing structural wall studs, hanging new drywall, matching textures, full paint. | $4,500 – $9,000 |

How to Defeat the Hidden Leak Trap Safely

Leaving your property asset on a basic, off-the-shelf insurance contract without verifying your custom endorsements means your family's savings are entirely exposed to a single hidden droplet of water.

At Walker Insurance Agency, we advise clients to bypass this structural trap using a dual-layer defensive strategy:

Step 1: Install a Smart Smart-Flow Water Shut-Off Valve (Mechanical Shield)

Step 2: Add a Hidden Seepage & Constant Leak Endorsement (Contractual Shield)

================================================================================

= 100% Comprehensive Asset Protection from Invisible Drips and Slow Drywall Rot

- The Mechanical Shield: Deploying a smart leak-detection system (such as a Moen Flo or LeakSmart device) onto your main incoming water line tracks micro-changes in internal pressure. If a microscopic pinhole opens behind your master bathroom drywall and drips even an ounce of water, the system detects the anomaly, sends an urgent alert to your smartphone, and safely shuts off your home's main water valve automatically.

- The Contractual Shield: Ask your independent agent about adding a Hidden Seepage / Continuous Leak Rider and expanding your Mold Coverage Endorsement to $25,000 or $50,000. The hidden seepage rider explicitly overrides the standard 14-day rule, forcing the carrier to pay for leaks that occur entirely out of sight behind architectural walls or underneath concrete slabs, regardless of how long they went undetected.

Why Working with an Independent Agency is Vital

Attempting to manage your primary property asset through a faceless smartphone app means your policy will lack the critical specialty riders required to survive long-term plumbing emergencies. At Walker Insurance Agency, we provide the data-driven visibility you need to secure your home.

The Walker Advantage:

- Endorsement Audit Reviews: We meticulously dissect your policy fine print to spot hidden water damage limitations and fortify your contract with preferred water riders before a drip ever forms.

- Mitigation Discount Integration: We ensure that your smart automatic shut-off valve installation is formally logged with your underwriter, legally triggering mandatory safety premium credits on your account.

- Resurgent Market Shopping: As the private property market stabilizes with 20 brand-new private insurance carriers entering Florida, we continuously shop your profile to locate companies offering the highest mold and seepage caps at the lowest available rate floors in Stuart.

FAQ

1. Does my standard home insurance cover the plumber’s bill to fix the broken pipe?

No. Even if your water damage claim is 100% approved because the leak was sudden, the insurance contract considers the actual physical piece of plumbing pipe to be basic home maintenance. The carrier will pay to tear out the drywall to reach the leak and pay to rebuild the wall afterward, but the plumber’s invoice to patch the pipe itself must be paid out of pocket.

2. What should I do immediately if I suspect a slow leak inside my wall?

Do not let a contractor immediately rip down your drywall before capturing evidence. Go to your main water meter box, ensure all faucets are off, and see if the low-flow dial is spinning. If it is, call a leak detection specialist to locate the drip using thermal imaging or sonic testing. Save the digital diagnostic report and video files; this documentation provides the primary proof your independent agent needs to successfully navigate a claim.

3. Does home insurance cover mold caused by high humidity or poor bathroom ventilation?

No. Standard policies completely exclude mold or mildew caused by ambient air humidity, condensation, or inadequate ventilation systems. Property owners are expected to control interior climate levels using air conditioning units and exhaust fans to keep moisture levels below 60%.

Insulate Your Savings from a Hidden Water Peril Today

A slow, hidden wall leak is quiet, entirely invisible, and mathematically weaponized to void your insurance protection if left unresolved for two weeks. Relying on an ordinary, unmodified property contract to cover a subterranean or behind-the-wall drip is a gamble that can destroy your household budget.

Verify your hidden water riders before a leak breaks your budget. Contact Walker Insurance Agency today for a comprehensive property coverage review. We provide the visibility you need to erase hidden seepage loopholes, deploy smart automated defenses, and protect your family's lifestyle safely in Stuart.

[GET A FREE QUOTE TODAY]

Call us at +1-407-977-7100 or visit our office in Stuart, FL. Let us secure your home boundary lines today.

Related Articles

Does Insurance Pay for Lost Resale Value After a Crash? (2026)

Learn whether insurance pays for your car's lost resale value after an accident in 2026, how diminished value claims work, and how to recover your money.

Read More →

Recover Thousands in Diminished Value After an Accident (2026)

Your car was repaired after a crash, but it lost thousands in resale value. Learn how to recover inherent diminished value from the at-fault driver's insurance.

Read More →

In the Shop for a Week? Why Auto Insurance Won't Cover Your Rental

Is your car in the shop for a week of mechanical repairs? Learn why standard auto insurance rental reimbursement won't pay for a rental car in 2026.

Read More →